To better serve and retain retired or soon-to-be retired clients, advisors should use the actuarial budget benchmark (ABB), an annual spending plan developed using actuarial and financial economic principles.

Regardless of how you currently assist your client with their financial planning, adding the ABB to your client discussions will reduce your fiduciary risk or, at a minimum, reduce the risk of having a dissatisfied client and help your client make better financial decisions before and during retirement.

This article will:

- Describe the ABB,

- Explain how you can calculate it, and

- Demonstrate why you will want to make the calculation and your communication of the ABB an integral part of your approach.

I will also illustrate the calculation and the use of the ABB with an example.

The actuarial budget benchmark (ABB)

The ABB is an annual calculation based on your client’s specific information and basic actuarial and financial economics principles. It balances the market value of your client’s assets with those of your client’s spending liabilities using the following actuarial equation:

|

Accumulated Savings

|

+

|

PV Income from Other Sources

|

=

|

PV Future Non-Recurring Expenses

|

+

|

PV Future Recurring Annual Spending Budgets

|

The items on the left-hand side of the equation are the client’s assets and the items on the right are the client’s spending liabilities in retirement. To obtain the ABB, the present value of (or reserve for) future non-recurring expenses, such as unexpected expenses, bequest motives and long-term care expenses, is first subtracted from the client’s assets and the remaining amount is spread over the client’s expected remaining lifetime.

ABB calculation assumptions

To make the ABB a “mark-to-market” calculation, the market value of the client’s spending liability is determined using financial economics principles using the price of a portfolio of financial assets whose expected distributions match the anticipated client spending in amount, timing and probability of payment. I recommend using life annuities as the financial assets for this purpose.

My recommended discount rate and lifetime planning period assumptions for ABB calculation purposes are more conservative (higher) than the current cost to settle spending liabilities through annuity purchases, as I recommend assuming a 25% probability of survival lifetime planning period for individuals in excellent health rather than the 50% probability generally used in annuity pricing. I make this recommendation because individuals who self-insure a portion of their retirement spending will not be eligible for mortality credits with respect to that portion of their assets as they would with an annuity, and will therefore generally need to plan more conservatively, all things being equal.

For ABB calculation purposes, I also assume that future recurring annual spending budgets remain constant in real dollars over the client’s remaining lifetime planning period.

My assumptions for ABB calculation purposes are a little more conservative (because of the longer assumed lifetime planning period), but similar to the cost of retirement promoted by BlackRock in their CORI indextm. If you like BlackRock’s CORI concept for determining the cost of providing real dollar retirement income for life, you will love it for calculating the ABB for your clients.

Using the ABB

The ABB considers your client’s total retirement assets and liabilities, not just withdrawals from their investment portfolio. I recommend comparing the client’s pre-tax spending budget for annual recurring expenses with your client’s ABB on an annual basis and monitoring the trend in this ratio over time. The ABB is a conservative measurement of the amount of constant real dollar spending that can be supported by the client’s assets (reduced by reserves for expected non-recurring expenses) based on the assumption that the client’s assets are invested in relatively low-risk investments. Annually benchmarking your client’s spending budget against their ABB provides the client with a measure of how aggressive their current investment and spending strategy is relative to a relatively low-risk strategy.

Based on your client’s financial goals and investment strategy, they may be comfortable with a spending budget that is more aggressive (higher) or even more conservative (lower) than the ABB. Your client’s level of comfort may, however, change over time, depending on the trend of this ratio over time.

How to calculate a client’s ABB

The client’s ABB may be calculated by applying the actuarial equation shown above using a discount rate (and other assumptions) developed from financial economics principles. I provide an Excel workbook and recommended assumptions (including assumptions for determining reserves for non-recurring expenses) for this purpose on my website to make this easier. However, financial advisors may wish to develop their own software for this purpose and/or use their own reasonable approach to estimate the “market value” of their client’s spending liabilities.

Benefits of incorporating the ABB into your consulting approach

Improve client understanding

As Derek Tharp noted in his February 8, 2017 guest post in the Kitces.com blog, “Monte Carlo analysis has become a common standard amongst financial advisors for evaluating the health of a prospective retiree’s spending plan in retirement” and pointed out, “there’s one big problem [with Monte Carlo analysis]: it’s difficult to know how to interpret the results.” Tharp suggests that to address this problem, advisors should emphasize the importance of ongoing planning and should present information in more than one way. Annual benchmarking against the ABB will be more effective than simply updating the client’s Monte Carlo analysis to develop a revised probability of success that the client may still have difficulty interpreting. In addition to reflecting changes in the client’s assets from year to year, the ABB will also reflect changes in interest rates.

The ABB is a conservative measurement of the client’s total recurring spending budget that does not depend on historical investment returns generally assumed for forecasting purposes in Monte Carlo modeling. It is a benchmark for comparison with the recurring spending budget that the advisor recommends, which is typically based on the client’s specific investment strategy and a number of other factors. Explaining why the advisor’s recommended spending budget differs from the ABB will help the client (and the advisor) better understand the financial implications of assuming historical rates of investment return and other factors as well as the limitations of the advisor’s Monte Carlo analysis.

Keeping spending budgets on track to meet client goals

The difference and trend over time between the client’s spending budget and the ABB quantifies how far off the actuarially balanced “mark to market” track the client’s investment and spending strategies have led the client, and provides useful information to move spending back into the client’s “comfort zone” relative to the ABB over time.

Suppose the spending budget developed by the advisor is significantly higher than the client’s ABB this year. There could be several reasons for this, including:

- More optimistic expectations about future investment returns, longevity or inflation than used in the ABB;

- A conscious desire by the client to have declining real dollar spending in future years;

- Over-smoothing of unfavorable prior investment experience;

- Under-estimation of non-recurring expenses or over-estimation of other income sources relative to those used in the ABB (which can be rectified if the advisor believes her estimates are better than the estimates used in the ABB); or

- The mechanics of the advisor’s spending budget calculation may overstate short-term spending budgets relative to expected long-term spending budgets.

Your client may be just fine with the difference this year between your calculated spending budget and the ABB. However, if your client’s outcome significantly deviates from your assumptions during the year, the difference between the two spending budgets at the end of the year may creep outside of the client’s comfort zone. The ABB provides your client with an important data point that can be used to help them reach the decision that it may be time to decrease spending.

While the ABB is based on fairly conservative assumptions, the spending budget developed by the advisor might be significantly lower than the ABB. There could be several reasons for this, including:

- More pessimistic assumptions about future investment returns, longevity or inflation than assumed for the ABB;

- A conscious desire by the client to underspend (or save) during retirement or have increasing real dollar spending in future years of retirement;

- Over-smoothing of favorable prior investment experience;

- Over-estimating non-recurring expenses or under-estimating other income sources relative to those used for the ABB; or

- The mechanics of the advisor’s spending budget calculation may under-state the client’s short term spending budget relative to the long-term spending budget.

This result may be just fine with the client, provided it is consistent with their financial objectives and tolerance for risk. If it isn’t, the ABB can give the client important information to possibly increase spending over time and get spending back into the client’s comfort zone relative to the ABB.

Balancing need for spending stability with need to mitigate sequence of return risk

Comparing the client’s ABB to the more static spending approaches typically recommended by advisors (that generally stress spending stability) can also help clients balance their need to avoid unnecessary fluctuations in spending with their need to mitigate sequence of return risk.

Reducing advisor fiduciary risk

Finally, annually benchmarking the client’s spending budget against the client’s ABB and monitoring the trend over time reduces the risk of breaching of fiduciary liability by educating the client about the potential risk of future spending adjustments inherent in their investment and spending strategy. Compare this with the fiduciary risk (or loss-of-client risk) with a client whose advisor does not benchmark against the ABB and who is forced to significantly reduce spending after being initially told by his advisor that his spending and investment strategy had a 99% probability of success.

Example

Mike is a 65-year old single male who earned $100,000 last year and believes he needs a pre-tax recurring spending budget of about $70,000 per annum to replace his pre-retirement standard of living. For calculation simplicity, we are going to assume that Mike’s home equity exactly covers the reserves he needs to set aside to cover all his expected non-recurring expenses. He has $1,000,000 in accumulated savings and is eligible to immediately start his Social Security benefit of $2,042 per month, or $24,504 annually. He has no other assets and no other spending liabilities.

The recommended assumptions to develop Mike’s ABB are:

- A discount rate of 4% per annum

- Inflation of 2% per annum

- Lifetime planning period of 29 years (25% probability of survival from the Actuaries Longevity Illustrator assuming excellent health and non-smoker)

Mike’s ABB assumes that his future spending budgets will increase with assumed inflation of 2% per annum.

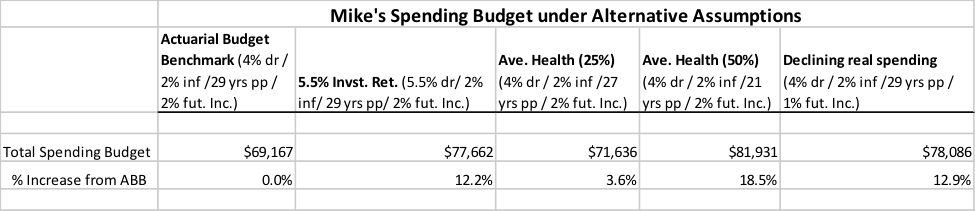

Based on these assumptions and using my Excel workbook (available in my website), Mike’s ABB for this year is $69,167. By comparison, the 4% rule would give Mike a spending budget of $64,504 (.04 X $1,000,000 + $24,504), or about 93% of Mike’s benchmark budget.

If you are an advisor, you may wish to compare the budget you would have provided to Mike with his ABB. Of course, the budget you provide would depend on several factors such as Mike’s risk tolerance, his investment strategy, his general health, his desire to front-load spending, etc., so it would not be unusual for it to be higher or lower than his ABB.

The chart below shows the effect on Mike’s spending budget (developed using my workbook) of using different assumptions for average future investment return, his lifetime planning period (based on his health and probability of survival from the Actuaries Longevity Estimator) and his desired rate of future budget increases. The items in parenthesis describing each set of alternative assumptions are: discount rate, inflation rate, lifetime planning period based on health and assumed probability of survival and desired increase in future spending budgets.

For example, if Mike were comfortable with 1% per year less than inflation annual increases in his spending budgets but felt more comfortable with the other ABB assumptions, he may target a spending budget more than $70,000 but less than the $78,086 spending budget shown in the last column of the graph, and he and his advisor may decide that his “ABB comfort zone” is 95%% to 130% of the ABB (a corridor around the 112.9% level). They also agree that Mike would consider changes to his spending strategy in the future if his spending budget should fall outside this ABB comfort zone.

Conclusion

Using Monte Carlo modeling to develop client spending budgets is an effective approach but not a perfect solution. In addition to using historical data to forecast future investment performance, many clients don’t fully understand the probability-of-success output. Some advisors use even less effective approaches to develop spending budgets for their clients, such as adding “safe” withdrawals from an investment portfolio to income from other sources.

Rather than requiring clients to have faith that these approaches will produce results consistent with their financial objectives, advisors should supplement their current approach by calculating and communicating an ABB to enable their clients to make better budgeting and investment decisions. Adding this additional data point to advisor-client discussions will reduce your fiduciary risk and will result in better informed and more satisfied clients.

Ken Steiner is a retired actuary with a website entitled, "How Much Can I Afford to Spend in Retirement."

Read more articles by Ken Steiner