Add Federal Reserve Chairman Jerome Powell to the roster of deficit hawks. In a widely followed speech, he claimed that the country’s fiscal path is “unsustainable.” But Powell still believes the Fed’s monetary policy is working, and that low inflation and unemployment will continue.

Add Federal Reserve Chairman Jerome Powell to the roster of deficit hawks. In a widely followed speech, he claimed that the country’s fiscal path is “unsustainable.” But Powell still believes the Fed’s monetary policy is working, and that low inflation and unemployment will continue.

We remain in “extraordinary times,” and these favorable conditions are likely to persist, he said.

“The economy is strong, unemployment is near 50-year lows, and inflation is roughly at our 2% objective,” Powell said. The baseline outlook of forecasters inside and outside the Fed is for more of the same, he said.

Powell took office as chairman of the Federal Reserve in February 2018, following his tenure as chairman of the Federal Open Market Committee (FOMC). He spoke at the NABE 60th Annual Meeting in Boston on September 30, you can access a copy of his remarks here.

His talk focused on the Fed’s ongoing efforts to promote maximum employment and stable prices during this period of low inflation and low unemployment.

I will explain why Powell claims the country is on an unsustainable fiscal path, but first let’s look at his analysis of current economic conditions.

Powell: The economy looks very good

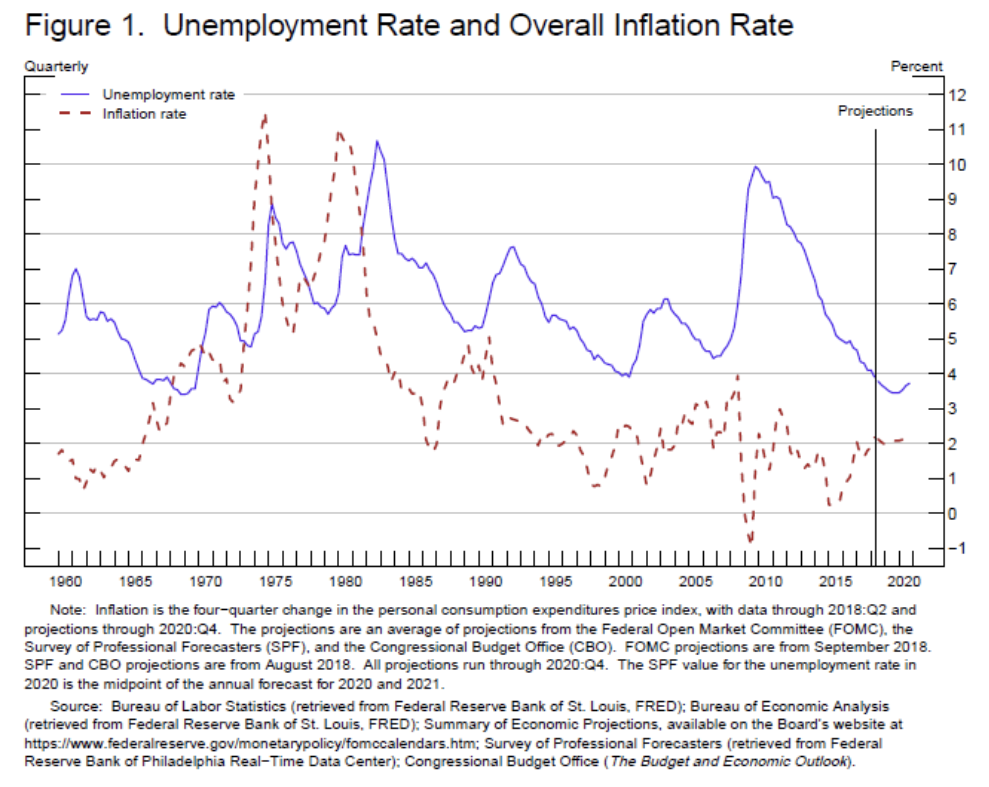

“The unemployment rate stands at 3.9%, near a 20-year low,” Powell said. “Inflation is currently running near the Federal Open Market Committee's (FOMC) objective of 2%.”

“I am pleased to say that, by these measures, the economy looks very good,” he said.

The graph below shows the unemployment (in blue) and inflation (in dotted-red) rates since 1960.

According to Powell, these two top-line statistics signal a positive view that is further supported by data on jobs and prices. “Many forecasters are predicting that these favorable conditions are likely to continue,” he said.

He said that he was asked whether these forecasts are too good to be true, which was “a reasonable question.”

Since 1950, the U.S. economy has never experienced both low inflation and low unemployment for such an extended time. This has some analysts asking “Is the Phillips curve dead?”

The Phillips curve is an economic model that holds that unemployment and inflation are inversely related. Low unemployment tends to push up wages, leading to rising labor costs, which feeds price inflation for consumers. The more that changes in labor market slack impacts inflation levels, the steeper the Phillips curve.

“I do not see it as likely that the Phillips curve is dead, or that it will soon exact revenge,” he said.

What is more likely, according to Powell, is that “better monetary policy has played a central role” over the last few decades. This has greatly reduced, but not eliminated, the effects that tight labor markets have on inflation.

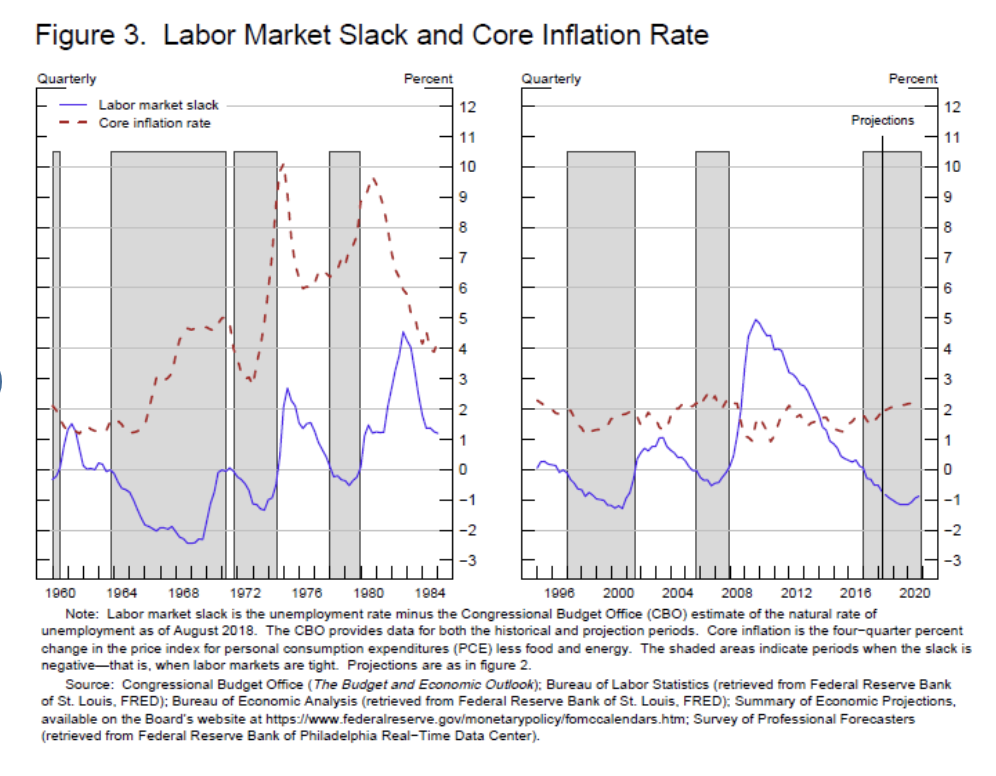

The graph below shows the relationship between labor market slack (in blue) and core inflation (in dotted-red) since 1960.

“The outlook is consistent with evidence of a very flat Phillips curve and inflation expectations anchored near 2%,” he said.

“These developments amount to a better world for households and businesses, which no longer experience or even fear the scourge of high and volatile inflation,” Powell said.

However, Powell emphasized, no one fully understands the nature of these relationships. Given this uncertainty about the unemployment-inflation relationship, he said, risk management and contingency planning plays an important role in setting monetary policy.

The Fed’s monetary policy

Powell made the case that forecasts are not too good to be true, and unemployment will remain below 4% and inflation will stay steady near 2% for an extended period.

This historically rare pairing of steady, low inflation and very low unemployment is testament to the fact that we remain in extraordinary times, he said.

“Our ongoing policy of gradual interest rate normalization reflects our efforts to balance the inevitable risks that come with extraordinary times,” he said.

If the Fed removes accommodation too quickly, he said, it could needlessly cut the expansion short.

But if the Fed moves too slowly, it could lead to rising inflation and a sudden spike in inflation expectations. Robert Gordon, who spoke at the same conference, predicted that this is what will lead us to the next recession.

“Our path of gradually removing accommodation, while closely monitoring the economy, is designed to balance these risks,” he said.

Powell suggested that managing expectations is indeed a priority when the Fed sets monetary policy.

“We attribute a great deal of the stability of inflation in recent years to the anchoring of longer-term inflation expectations,” he said. “And we are aware that it could be very costly if those expectations were to drift materially.”

We’re not on a sustainable path

“Obviously fiscal policy is providing real support to demand this year, and probably for the next couple of years,” he said.

“Longer term, we’re not on a sustainable fiscal path, we haven’t been for many years,” Powell said. With rising fiscal debt, some economists have cautioned that the market could be susceptible to a drop from future declines in demand. “There’s the possibility of some supply side effects that we’ll see emerge,” Powell acknowledged.

Powell also said that we’ll have to wait and see whether new tariffs drive inflation or simply increase price levels globally. It’s too early to see the effects of trade policy changes in the data, he said.

But Powell concluded by reiterating his positive analysis of the economy. “This is a good time to be working,” he said, “this is the top of the cycle.”

Marianne Brunet is a financial markets analyst at Advisor Perspectives.

Read more articles by Marianne Brunet

Add Federal Reserve Chairman Jerome Powell to the roster of deficit hawks. In a widely followed speech, he claimed that the country’s fiscal path is “unsustainable.” But Powell still believes the Fed’s monetary policy is working, and that low inflation and unemployment will continue.

Add Federal Reserve Chairman Jerome Powell to the roster of deficit hawks. In a widely followed speech, he claimed that the country’s fiscal path is “unsustainable.” But Powell still believes the Fed’s monetary policy is working, and that low inflation and unemployment will continue.