A large body of literature demonstrates that there are predictable patterns in security returns that conflict with market efficiency. If there are behavioral explanations, these are called anomalies. A new study looks at whether “insiders” (those with access to nonpublic, material insider information) exploit those anomalies – and whether investors can benefit from observing insider trading patterns.

Following is a list of 11 such anomalies that have been studied.

- Net stock issues: Net stock issuance and stock returns are negatively correlated. It’s been shown that smart managers issue shares when sentiment-driven traders push prices to overvalued levels.

- Composite equity issues: Issuers underperform non-issuers, with “composite equity issuance” defined as the growth in the firm’s total market value of equity minus the stock’s rate of return. It’s computed by subtracting the 12-month cumulative stock return from the 12-month growth in equity market capitalization.

- Accruals: Firms with high accruals earn abnormally lower average returns than firms with low accruals. Investors overestimate the persistence of the accrual component of earnings when forming earnings expectations.

- Net operating assets: The difference on a firm’s balance sheet between all operating assets and all operating liabilities, scaled by total assets, is a strong negative predictor of long-run stock returns. Investors tend to focus on accounting profitability, neglecting information about cash profitability, in which case net operating assets (equivalently measured as the cumulative difference between operating income and free cash flow) captures such a bias.

- Asset growth: Companies with high growth rates in their total assets earn lower subsequent returns. Investors overreact to changes in future business prospects implied by asset expansions.

- Post-earnings announcement drift: If earnings surprises are positive (negative), future stock prices drift upward (downward) – stock prices drift in the same direction as the earnings surprise.

- Investment-to-assets: Higher past investment predicts abnormally lower future returns.

- O-score: This is an accounting measure of the likelihood of bankruptcy. Firms with higher O-scores have lower returns.

- Momentum: High (low) recent (in the past year) past returns forecast high (low) future returns over the next several months.

- Gross profitability premium: More-profitable firms have higher returns than less-profitable firms.

- Return on assets: More-profitable firms have higher expected returns than less-profitable firms.

There are also other predictable patterns that are anomalies for the capital asset pricing model (CAPM): Small stocks have outperformed large stocks and value/cheap stocks have outperformed growth/expensive stocks. While the size premium is generally considered compensation for risk, there is a great debate on the source of the value premium. Is it risk- or behavioral-based?

Whether the explanation is risk- or behavioral-based, an interesting question is whether inside investors exploit these anomalies. And if they do, does that provide us with any insights into the sources of the anomalies?

Deniz Anginer, Gerard Hoberg and Nejat Seyhun contribute to the literature and our understanding with their November 2018 paper “Do Insiders Exploit Anomalies?” They began by noting that the research has demonstrated that “insiders can also accurately identify times when their own firm’s common stock becomes over- or underpriced and they trade to exploit such mispricing. Insiders buy before an abnormal stock price increase and sell before an abnormal stock price decline. Such trading can improve price efficiency and create large positive externalities in the form of price efficiency and resource allocation if the required disclosure of insider trades can be used by sophisticated anomaly traders to speed price corrections.”

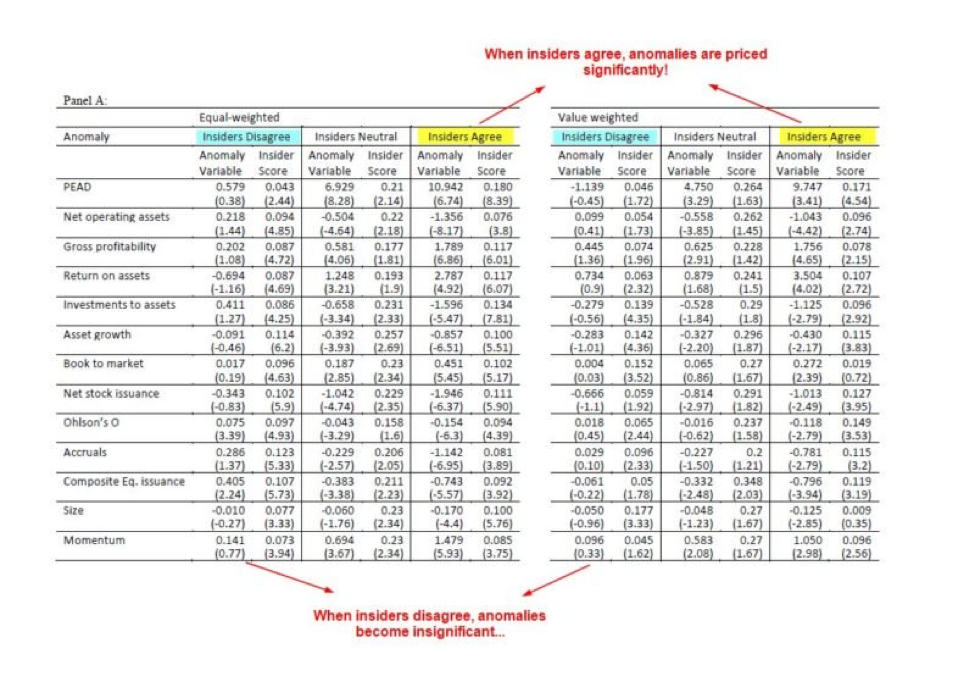

Anginer, Hoberg and Seyhun investigated whether insiders are able to exploit the 11 behavioral anomalies as well as the value and size factors. They also analyzed the consequences of mandatory public disclosure. They used a large insider trading database covering the period 1975 through 2014. Their hypothesis was that if insider trades systematically predict the direction of returns due to anomalies, it is likely that anomalies are due to mispricing/informational inefficiency. Specifically, they examined the predictability of anomalies when insiders agree or disagree with the direction of returns implied by a given anomaly (the “agree-disagree portfolio”). There was agreement if insiders are buyers of the stock and the anomaly signal predicts high returns, or if insiders are sellers of the stock and the anomaly signal predicts low returns. There is disagreement if insiders are sellers of the stock and the anomaly signal predicts high returns, or if insiders are buyers of the stock and the anomaly signal predicts low returns. The signal is neutral if insiders are neither buyers nor sellers.

Following is a summary of their findings:

- A significant portion of the informational content of anomalies, both in magnitude and timing, can be explained by insider signals. When insiders agree, anomaly returns are significantly higher in the three months after insider trades are made public. After the three months, mispricing is corrected, and subsequent abnormal returns are significantly lower.

- With all 13 anomalies, mispricing is corrected shortly after insider trading becomes public, but only when the direction of insider trading agrees with the anomaly.

- Anomaly returns vanish when insider trading disagrees with the anomaly. For some anomalies, the direction of their returns is reversed.

- When insiders do not trade, anomaly returns are modest and persist beyond three months.

- The “agree-disagree portfolio” is significantly positive for all anomalies. Using equal weighting, the average monthly CAPM alpha across all anomalies is -0.27 percent for the disagree portfolio. It is 0.54 percent for the agree portfolio. Three-factor alphas are weaker but are still economically and statistically significant.

- For most anomalies, insiders are contrarians. For example, insiders tend to sell when the stock price has gone up and momentum is high, and buy when the stock price has gone down and momentum is low.

They found that insider trading is generally less informative for large firms— the results are somewhat weaker when value weighting versus equal weighting.

Since insiders tend to sell more shares than they buy and may trade routinely based on motives not related to information (such as diversification and rebalancing), as a test of robustness, they computed abnormal shares traded for each firm each month by standardizing net insider trades using the previous 36-month average and standard deviation. They found similar results using abnormal shares traded.

The authors concluded: “These findings support the conclusion that exploitable mispricing plays a role in explaining a large number of anomalies, and that insiders trade on these anomalies and thereby improve market efficiency.” They added: “Hence our results suggest that risk averse insiders are able to identify short-horizon episodes where investment opportunities have both high alpha and low risk.” They also stated: “While we cannot rule out risk-based hypotheses, our evidence indicates that market mispricing likely plays an important role in all 13 anomalies we test.”

The following table from the paper provides evidence suggesting that funds/investors should jointly consider insider trading signals along with anomaly signals.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.

More Mutual Funds Topics >