Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In her July 21 Think Advisor article, What’s Wrong With Advisors’ Retirement Planning Models, and How to Fix It, Bernice Napach highlighted some of the problems with planning models used by most financial advisors. Those problems were discussed by three distinguished financial planning experts in a panel discussion at the recent Engage 2020 virtual conference: Michael Kitces, David Blanchett and Michael Finke. And while Napach’s article detailed the problems raised by those gentlemen, it falls short at discussing the fixes.

This article discusses an obvious fix to those problems: Financial advisors should incorporate actuarial financial planning process (or components of it) into their planning toolkits.

Problems with current modeling tools and processes

Some of the problems noted by the panel experts included:

|

Kitces:

|

Current industry tools for retirement planning “are not very good.”

|

|

Kitces:

|

Tools don’t provide an adequate framework to adjust from two people in a couple to one (after first death within a couple).

|

|

Blanchett:

|

Retirement plans need to quantify the value of non-financial assets. Advisors view assets as income but not income (like Social Security or pensions) as assets.

|

|

Finke:

|

Plans should reflect flexibility to adjust spending.

|

|

Finke:

|

Retirees also need to understand how much of their budget is fixed and how much is variable.

|

The fix: Incorporate actuarial financial planning process

In my September 2, 2019 article, An Actuarial Process for Better Decisions in Retirement, I set forth a recommended retirement planning process for retirees and near retirees and included an example of how this process would work. The process involved the following seven steps:

1. Based on a review of current expenses, estimate the client’s future recurring expenses in retirement

2. Estimate the client’s future non-recurring expenses

3. Work with the client to categorize each expense in steps 1 and 2 as “essential” or “discretionary.”

4. Using one of my actuarial budget calculator workbooks for retirees, determine the actuarial reserves (budget buckets) theoretically needed to separately fund future essential expenses and future discretionary expenses. Note that more aggressive assumptions may be used to determine the actuarial reserves needed to fund future discretionary expenses than the reserves needed to fund future essential expenses.

5. Compare the total present value of the client’s assets with total actuarial reserves needed as calculated in step 4.

If the total present value of the client’s assets is less than total actuarial reserves needed, suggest:

- increasing client assets (for example through part-time employment),

- decreasing client current and future spending budgets,

- applying a reasonable smoothing algorithm to the client’s current spending budget, or

- some combination of these alternatives.

If the total present value of client assets is greater than the total actuarial reserves needed, suggest increasing the client’s:

- current and future spending budgets,

- rainy-day fund, or

- some combination of the two.

6. Develop a liability-driven investment (LDI) strategy consistent with floor and upside portfolio calculations in Step 4, where investments in low-risk assets (the floor investments) are anticipated to be sufficient to fund spending on future essential expenses and investments in risky assets (the upside portfolio) are used to fund spending on future discretionary expenses.

7. Repeat above steps at least once a year and periodically model deviations from assumed experience by stress testing significant assumptions for the purpose of modifying the client’s plan to mitigate risks.

Benefits of the actuarial financial planning process

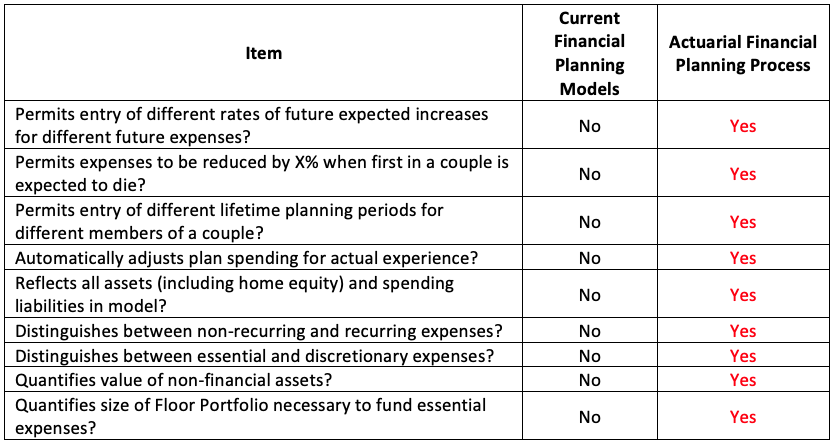

The chart below compares the functionality of my recommended actuarial process with that of models employed by many financial advisors. The chart focuses on the problems discussed by the panelists, as well as several problems not discussed.

Functionality comparison

The above chart shows that certain aspects of retirement planning can be improved by incorporating the basic actuarial principles and processes built into my recommended approach into the tools currently used by financial advisors. And while I wouldn’t say that the industry tools used for financial planning “are not very good,” as noted by Kitces, I agree with the three panelists that they certainly can be improved.

Summary

I thank Napach and the three gentlemen who participated in the recent Engage 2020 conference for teeing up my recommended actuarial financial planning process for retirees and near-retires. Adding this process and tools (or components of it) to financial advisor toolkits will help advisors better meet the needs of their clients.

Ken Steiner, FSA, is a retired actuary with a website entitled, "How Much Can I Afford to Spend in Retirement."

Read more articles by Ken Steiner

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.