What Ever Happened to Value Investing?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This article is about an exception to a rule – an exception that, I believe, has ceased to be. And so the rule has become stronger, and there is a little less joy in the investing world.

Over the last decade or so, the broad public has come to recognize what academic economists have been proclaiming for several decades: It is extremely difficult and unusual for even dedicated professional investors to “beat the market,” that is, to get better returns than the market as a whole over the long run. (Sure, in the short run, it happens all the time. There are always folk with good luck. And greenhorns and carnival barkers will still have their fun on Robinhood or the next brokerage that comes along to serve the masses.) And when I say “market,” I mean not just the stock market; it’s also very difficult to beat other large financial markets, like, for example, the market for government and corporate bonds. This is why index funds have become so popular. Index funds represent markets (or segments of markets) in their entirety, and the managers of these funds don’t try to pick the best in class. They simply buy stocks (or if they’re bond index funds, then bonds) that represent the market, thereby earning the same return, less the tiny percentage of the funds’ value they take as their fee. (An index or benchmark is the representation, by a list of specific financial securities weighted in proportion to their values, of an entire market, or of a carefully defined segment of a market, and an index fund holds all the securities on that list in the same proportions, or, if the list is enormous, then a large representative sample of those securities.) So, for stocks, you’ll do better if you own a representation of the entire stock market than you will if you own only the stocks that you or your advisor have persuaded yourself are better than the rest.

But academic economists have also known, for nearly as long as they have proclaimed that it’s very hard to beat the market, that market indexes, at least the ones that are commonly used and that feature in nightly business news (the Dow and the S&P 500), are imperfect representations of the market.

And so, within the broad asset class that is stocks, some of us professionals, including me, who agree that the stock market is hard to beat, nevertheless try to improve returns beyond what a simple S&P 500 index fund (a fund that replicates the familiar benchmark of U.S. stock market returns) would achieve. We do this by relying upon a continuation of long-term historical stock behaviors that have been validated by conventional statistical analyses. One of these stock behaviors is the subject of this essay: The tendency of so-called “value stocks” to produce superior returns in the long run.

The reason that I am writing this article is that I’ve concluded that the long history of superior performance by value stocks now has much less relevance to the future of stock investing, and I am decreasing, although not eliminating, my reliance upon value stocks. Our reliance on value investing has caused some amount of underperformance of Peabody River’s equity allocations for some time, and our clients are owed an explanation. Our clients are hardly alone in having been hurt by value investing in recent years. Value investing has caused major hedge funds to bleed assets (which is the melodramatic way we investment professionals talk about losing clients) and some to go out of business, and caused many of our peer investment advisors to sweat and to swear to their clients that if they just wait long enough, value investing will reward them in the end.

I will explain why so many of us who have studied the stock market believed that value investing was worthwhile, and why I, for one – I can’t speak for others – have given up on it, although not entirely.

The basic idea underlying value investing

The basic concept underlying value investing has intuitive appeal: The identification of stocks whose intrinsic worth, as determined in a number of ways, seems to be greater, much greater, than the current stock price. Eventually, so the argument goes, the market will recognize what the clever investors already recognized, and the clever investors who bought the stocks early will earn superior returns. That sounds straightforward and sensible, but of course, the full explanation of how this plays out in practice rapidly becomes complicated. I’m going to try to make the explanation as simple as possible, and I hope to avoid the mystification, not to mention conceptual error, that inheres in much investment writing for the public.

To begin: One has to calculate the intrinsic worth of a stock (or the company it represents). There are four main inputs to the calculation: First, the liquidation value of the company if its assets were to be sold off today; in simplest form, this is the “book value”, which can simply be read off a company’s financial statements. Second, there are the cashflows that a company is expected to produce in the future. These are, roughly speaking, earnings, although the public probably thinks of these cashflows as dividends, which are actually a bit different. Third, there is the rate at which the company’s profits, or earnings, are going to grow in the future. (Past earnings should be irrelevant to determining value today.) And fourth, there’s the discount rate, by which the analyst transforms future earnings into what they’d be worth today, because, under most circumstances, the promise of a dollar in the future is worth less than a dollar today. (This input is the most complicated to estimate, and it entails estimating the risks to those future earnings, because greater risks justify higher discount rates.)

Now, although we need all four of these inputs to calculate, or, I should say, to estimate the value of a company, the expression “value investing” refers to approaches or styles of investing that focus primarily on the first and second, that is, the book value and the cashflows, and use those inputs, usually to the exclusion of growth estimates, to determine if the stock is worth more than its current price. There are “value investors” and “value stocks,” and even those investors who are not susceptible to the charms of the latter, that is, are not value investors, would generally still recognize them as such by their character and might still, sometimes, if they deem the moment right, choose to invest in them.

(There is a niche approach to investing that focuses on dividends almost to the exclusion of all else, which is the consequence of misunderstanding the economics of dividends and earnings. Even so, there is some historical evidence that might suggest a bit of attention to stocks that pay high dividends. But I digress.)

“Growth investing” is a complement to value investing. It focusses instead on the third input, the expected growth rate of a company’s earnings. Growth investors choose stocks that they believe are undervalued with respect to their growth prospects. For decades, investment professionals – some, but certainly not all – have divided themselves into two camps: value investors and growth investors. You should not infer from what I say here about the problems with value investing that growth investing is preferable. Remember: You need all four inputs to estimate the value of a stock. (There are also technical investing and momentum investing and other schools or cultures of investment practice, which I pass over here.)

Some of the appeal of value investing is that the inputs represent knowledge that is about as solid as anything in the world of investing. The published financial statements tell you the book value, the most recent past earnings, and the dividends. You can look up today’s price of the stock. In contrast, no one tells you the future growth rate of a company; it’s not in the financial statements; you have to guess it from stories of demand for the companies’ products, from economic forecasts, from an understanding of the companies’ future competitive environment, and so forth.

You can bet that value investors won’t put their money into internet startups that are losing money. Those are for growth investors, who care much less, if at all, about current earnings and book value and rely instead on narratives of what the future will bring.

There are, to speak very broadly, two ways to go about value investing. One might be termed (and often is termed) “fundamental,” and the other might be termed “quantitative.” These have much in common – after all, they’re both forms of value investing – but there are differences in methodology.

Bear in mind, when I write of “financial economists” or “academics” in what follows, that many or perhaps most academic economists who study finance are also consultants to or principals in investment management companies, and some professional investment managers also hold adjunct academic positions, so there’s never an opposition between economists and practitioners, but instead, disagreement among practitioners.

The fundamental approach to value investing

Value investing, though not under that name, has been around since before the middle of the last century. Its greatest advocate was Benjamin Graham, who was Warren Buffett’s mentor, and who wrote two classic texts, one for the general public, The Intelligent Investor, and the other for professionals, a textbook, in collaboration with David Dodd, Security Analysis, which has gone through six editions. (The first edition of the latter is a valuable collectors’ item.) Early on, Graham focused on book value, which I mentioned above, and which (after subtracting liabilities) he thought of as “liquidation value,” that is, what you could get today if you shut down a company and auctioned off its assets. That’s not exactly right, but it’s not a bad way to think about book value as a first approximation to the truth. Followers of Graham do not, of course, buy all stocks that look inexpensive when compared with their book values or future earnings. They thoroughly analyze companies to find those that, in their view, are truly priced too low by the market, at least as indicated by a comparison of their current stock prices with their book value, earnings, and robustness of their business model, and that also have a “margin of safety,” Graham’s term for the solidity of a fundamental value that offers some assurance that even an erroneous market cannot for long ignore. They also want to see that the stock represents a company that is in an understandable and viable line of business. Investors who proceed this way tend to hold very concentrated portfolios, that is, portfolios with not many more than a handful or two of stocks. This is the “fundamental” approach to value investing.

But another approach to value investing arose from modern financial theory and empirical economic analysis. This approach is related to Graham’s approach but relies much more on statistical analysis of stocks in aggregate and less on identifying a small number of individual companies that look like superior investments. This is the “quantitative” approach.

The quantitative approach to value investing: Basic concepts

Modern financial economic theory revolves around the relationship between measurable risks and expected returns. Furthermore, a concept that pervades modern financial theory, even though it is not a fundamental assumption, is the idea of “efficiency,” that is, that market prices immediately reflect all publicly available relevant information, in particular as this information might affect both returns and risks. (Note well: This definition theory does not posit that the prices reflect the information correctly, because there is no absolute standard reference for correct valuations. But there does follow a belief – and it’s no more than a belief – that the truth will out, and fast.) This idea of efficiency has been around for a very long time and in free-market ideology takes on the character of dogma, but it came to the fore in the 1960s in rigorous theoretical formulations and after testing against actual stock market data. It’s most closely associated with the academic career of Eugene Fama, of the University of Chicago, who shared the 2013 Nobel Prize in Economics for this work. (The Nobel Prize committee was nothing if not even-handed; they shared his prize with a financial economist whose work tended to contradict stock market efficiency.) If the market is perfectly efficient, no one, not even the most intelligent investor, can consistently beat the market, because the market, which is, by definition, the combination of all investors, immediately trades stocks (or bonds, or other investments for which there are public markets) on the arrival of any new information that might affect the outlook, and the consensus is generally better than the judgement of any individual. (Even the most fervent believers in market efficiency actually concede that there may be skilled investors, but it can take an impractically long time to distinguish them by their records from investors who just had a simple run of good luck, and by the time you’ve identified them, they may have lost their skill.)

And this is the intellectual foundation of and a justification for investing in broad stock market index funds. There is a lot of solid evidence, not just theory, to back it up.

If the stock market is efficient, then value investing is pointless. Well, not entirely pointless. Investors who use the methods of Graham would be contributing to the efficiency of the market in setting the right prices for stocks, but having made their contribution, they won’t reap any reward in the way of superior returns over time. (At least, hardly any of them will). All that matters, in this understanding, is a stock’s “exposure” to the market.

When I say “exposure,” I mean something like this: If a stock has an exposure of 2 to the stock market, then it will (on average) go up twice as much as the market when the market goes up, and it will go down twice as much as the market when the market goes down. Stocks have different exposures, and these don’t necessarily remain constant. (Those who know something of the mathematics of finance will recognize “exposure” as “beta.”) Exposure is thought of as “risk exposure,” in the sense that the stock market is risky, and a stock with an exposure of 2 has twice the market’s risk.

In this way of looking at the market (which everyone now acknowledges is a much too simplistic representation of the real world), the only factor that matters is the stock market as a whole. So financial models like this are called “single-factor” models. If you have even the most cursory acquaintance with the stock market, you know that a single factor alone doesn’t explain why any given stock goes up and down. There’s a lot else going on, but if you create a fully diversified portfolio of lots of stocks, the “all elses” of those stocks cancel each other out, leaving the single factor (and the average of the exposures of all the stocks in the portfolio to that factor) as the driver of the portfolio’s returns. Financial economists refer to the “all else” of a stock as “specific risk.”

Almost as soon, however, as the concept of market efficiency gained acceptance in the academic world, financial economists and investors trained in statistics were crunching stock market data and discovering a problem: In aggregate, stocks that had low price-to-earnings (P/E) ratios, or low price-to-book-value (P/B) ratios, the kind that we call “value stocks,” tended to have better returns than the market as a whole, even after adjusting those returns to reflect the stocks’ exposures to the single risk factor, that is to say, the market. If the stock market was efficient, this should not have been the case (because if anyone could see this phenomenon, all the investors taking advantage of it would buy the underpriced stocks, thereby bidding up their prices, and as a result, the extra return would disappear). This was termed – from the point of view that takes market efficiency as a given – an “anomaly.” As the years progressed, more and more anomalies were discovered, but these other anomalies are not the concern of this essay. (Note well: For all the anomalies, it remained the case that repeated studies found very, very, very few professional investors beating the market in the long run after allowing for the risks that they took – or even after not allowing for that.)

And the value anomaly was found to exist in foreign stock markets, too. (I’ve just read a paper that finds some specific forms of it in the Melbourne stock market up to 1987, after it was known in the U.S., but before it was widely exploited.) That means that this is not just a funny historical quirk of the American market, some sort of freak statistical artifact. Rather, it seems to have been a real universal stock market phenomenon.

Because a stock market anomaly is a source of extra return that isn’t (as far as anyone can tell) compensation for extra risk, it’s, well, not exactly a free lunch – lunch is the return from investing in the stock market in the first place – but a sort of free side order. Why not take it?

One conclusion you could draw from this was that those fundamental “Graham-style” investors had a point, although, quite likely – and they won’t like to hear this – that point was less that they had skill in their analyses of individual companies, than that they had a preference for the kind of stocks that anyway tended to have superior returns. And you didn’t have to do deep analyses to identify these stocks.

The quantitative approach to value investing: Diversifiable factors

But financial economists kept grinding away at the data, and beginning in the 1970s, some of them realized that, even if the stock market in general is efficient (and let’s forget about the anomalies for just a moment), returns – and risks – could be assigned to a multiplicity of shared economic causes that change over time. That is, every stock is exposed to a single set of multiple “risk factors” that explain the behavior of the stock market as a whole, and any given stock’s exposures to these factors, which are measurable at least with historical data, change over time. Another way of putting this is that these economists were breaking down most of the specific risks that I mentioned earlier, that is, the “all else” – and returns – into each stock’s exposure to common factors, leaving only a much smaller amount of return and risk that remained unexplained and unexplainable by financial models.

The largest common factor that explains stock returns over long time spans, by this reckoning, remains the return of the market as a whole, but – depending upon who is theorizing and identifying and measuring – the other factors included some of the sorts of information that value investors had been looking at all along. And if you could predict whether, over the next short period of time, a factor was going to produce better or worse returns, you could predict (with uncertainty, of course) the returns to portfolios of stocks that either emphasized or deemphasized those factors. If you could predict correctly, then you could get ahead of the efficient market. If you couldn’t predict, well, then the market was still efficient and you wouldn’t earn any extra return, but you could take quiet and unremunerative satisfaction in having a more sophisticated understanding of its behavior.

This way of analyzing the behavior of stocks accords well with casual observation. We all observe that in different periods, different kinds of stock are in favor, and others out of favor, often for good economic reasons that are apparent after the fact: sometimes the stocks of big companies, sometimes the stocks of small companies, sometimes medium-sized companies, sometimes tech companies, sometimes consumer products companies, sometimes health-care companies, sometimes mining companies, sometimes growth companies, and so on. Notice that these categories aren’t mutually exclusive. Most of these categories correspond to the risk factors that the financial economists were able to identify. So they would say, for example, that when health-care company stocks have done well, that has been because, in that period, the health-care industry factor produced a high return, and stocks with a large positive exposure to that factor therefore did well. Perhaps a consumer products company sells, among its many products, vitamins and blood pressure monitors; in this case, it would likely have a small but significant exposure to the health-care industry factor, even though it was not a primarily health-care company. This passing in and out of fashion of different kinds of stocks provides another reason to think that Graham-style value investors are only riding the wave of a value factor: When value stocks are in favor, the value investors do well, and when they are out of favor, the value investors do poorly.

To return to value: The value factors typically include one or more of: the ratio of earnings per share to the price of the stock; the ratio of accounting value (that is, “book value”) per share to the price; and something called “intrinsic value” per share to the price. Quantitative analysts (“quants”) prefer to work with earnings-to-price (E/P) over price-to-earnings (P/E), because earnings are sometimes zero, and division by zero perplexes computers.

When you see the “intrinsic value” of a stock mentioned, you can reasonably infer that it was calculated by something called a “dividend discount model,” of which the most basic is named the “Gordon growth model.” (The dictionary does not require that the expression “intrinsic value” imply the use of a dividend discount model, but in the parlance of quants that’s what it means.) Notice the word “growth.” Unlike the other two measures of value, dividend discount models explicitly take into account the growth component of the value of a stock. (There’s a sense in which the earnings-to-price ratio is an oversimplified dividend discount model, but I needn’t go into this here.) But the analysts who use dividend discount models tend to estimate growth rates that are much more conservative than the growth rates intuited by growth investors.

Although I’ve just cited three different value factors, they aren’t entirely distinct. That’s because stocks that have a large (or small) exposure to one tend to have a large (or small) exposure to the others. This makes it a little difficult to disentangle which factors are driving the returns to value stocks and by how much. (This is a technical problem called “multicollinearity,” and statisticians have methods for grappling with it.) So you won’t necessarily find all quantitative investors relying on the same value factors to the same extent.

The factor analysis approach to investing didn’t change the conclusion that value investing worked, but it allowed for easier automation of value investing. You could build the software equivalent of an investing machine. You’d pour into the hopper all the stocks in the market, set the dials for some of the factors to neutral, crank up the exposure to value factors, and rotate the knob the correct number of clicks for the number of stocks you wanted in the resulting portfolio. Then press the “Start” button. The machine would extrude (almost instantaneously) a diversified portfolio “tilted” (to whatever degree you preferred) toward value stocks. If all goes well, of course, value stocks go up in price and cease to be value stocks, and other stocks go down and become value stocks, so you have to rerun the machine periodically. Because you wouldn’t spend most of your waking hours analyzing each company, you’d likely turn the number knob way up, and create portfolios holding 20, 30, 40 stocks or more. This is, very roughly, what “quantitative” investment companies did for their clients.

Factor analysis was considered to be an explanation of short-run returns. Over the long run, only one factor, the return to the market as a whole, was the one that produced long-run returns – so it was thought. If you diversified away specific risk, represented by these various factors plus some residual amount that was unaccounted for by factors, you’d be left with the single market factor. That is to say, no component factor should produce a long-run return better than the stock market’s return after taking risk into account. (This is a subtle qualification, but an important one, and fundamental to how quantitative analysts construct portfolios and evaluate their subsequent performance.) To put this in practical terms: If you invested in an index fund, you were fully diversifying among these other factors, for the best possible balance of risk and return (if factor performance was unpredictable). But the breakdown of stock returns into factor returns did not, in itself, imply that the market was inefficient.

All the same, within this analytical framework, the success of value investing did not cease to be an anomaly. That it (and the other anomalies) produced superior returns in the long run, and to an extent not explained by their risk exposures, was not explained away by multi-factor models. Various causes of the anomalies were hypothesized, but none was ever caught in the act.

The quantitative approach to value investing: Non-diversifiable factors

For nearly as long as financial economists have thought in terms of multiple risk factors, some have had a slightly different idea: That basic to the nature of the stock market is that, at root, every stock is exposed to multiple factors that produce their own returns and risks, but these cannot be merged or diversified away. The market is efficient, that is, with respect to more than a single risk factor.

This is a subtle distinction: identifiable and diversifiable factors that explain specific behavior and that can be blended away by stirring together multiple stocks in a portfolio, leaving only the combination of each stock’s exposure (its sensitivity) to the entire market as the explanation of the portfolio’s long-run return, versus identifiable and undiversifiable factors, and you need to know a stock’s exposure, or sensitivity, to every one of these to explain its long-run return (again, plus its idiosyncratic behavior, its specific risk, which averages out in a portfolio in the long run). And this distinction matters for our understanding of how and why value investing works – if it does.

(I may mention incidentally that the economic theory behind this kind of at-root multiple-factor model is termed Arbitrage Pricing Theory, or APT for short. And no, I had nothing to do with it.)

Different financial economists have different statistical methods of constructing these factor models, and so come up with different factors, but often, they include what are recognizably “value” factors.

In only the last few years, the idea of “factor investing,” of either the diversifiable or undiversifiable sort, has reached the awareness of the professional investment community at large, most of whose members seem not to realize that it’s more than forty years old. And few, I believe, apart from those who spend their days in quantitative stock market analysis, understand that there are two kinds of factor investing (though all are aware that different quantitative analysts identify different factors).

Dramatically, in 1992, Eugene Fama, the doyen of efficient market theory, and his former graduate student, Kenneth French (now long of Dartmouth College), broke their silence on multi-factor models and published a famous academic paper in which they rigorously showed that there existed three factors that explained stock returns, one of which was the market, and that you could not diversify away the other two factors. That is, they redefined what it meant to be exposed to the market. Even assuming, as they did, market efficiency, you would have to construct portfolios that were not just exposed broadly to the market as a whole, but that had broad exposure to each of these factors (which is almost, but not quite, the same thing). And among the Fama-French factors was – yes – a familiar measure of “value,” namely, the ratio of book value per share to price. (In a later paper, 2015, they redid their analysis and found that there were four, not two extra factors that could not be diversified away. And since then, yet another factor has been added to their model. The Fama-French model is not, strictly speaking, a variant of Arbitrage Pricing Theory, because it retains the market as the single most important factor, which APT does not, but this difference need not concern us.)

There were two common reactions to the Fama-French paper in the professional investing community. One was to say, “Big deal; welcome to the club – we knew this all along.” The other was to call on their outsized academic reputations as validation of value investing (and the investment styles represented by their other factors).

From the perspective of this kind of investing theory, the “value” phenomenon was no longer an anomaly, because it wasn’t an exception to the way the stock market is supposed to work. Rather, the theory now said that this was how the stock market should and does work. And it implied that a portfolio with the ideal tradeoff between prospective return and risk should be more “tilted” toward value stocks than a simple index.

Straddling two investment worlds

Joel Greenblatt, a hedge fund manager, in his popular self-help book The Little Book that Beats the Market (second edition 2010), offered a methodology that was a bit of Graham, and a bit of quantitative analysis. He offered a formulaic approach that anyone with an inexpensive source of stock data and an MS Excel spreadsheet could implement at home to apply Graham’s basic principles in order to select large numbers of value stocks that would beat the market, though he recommended a portfolio of about 30 stocks. He even provided a Web site (still running), in place of MS Excel, for the public to implement his “magic formula.” This formula has just two components: a comparison of stock price with earnings, and the historical “return on capital” of the company, a measure of how good the business was. Greenblatt didn’t build an economically deep and subtle financial risk model, or mine enormous quantities of data for complex and repeating patterns, as quantitative investment managers do, but like them, he automated investment management with a database. Greenblatt’s hedge fund uses a refined version of his methodology, the refinements (presumably deeper analyses of the data, which he doesn’t describe in his book) being the justification for the fund’s fees.

(An actor playing Greenblatt, who is not identified by name, appears in the film The Big Short, threatening to pull his money from Dr. Michael Burry’s management as he grows impatient waiting for Dr. Burry’s forecast crash.)

I single out Greenblatt for being a distinctly modern, and at the same time, clear, and especially well-known writer from among the numberless popular writers on value investing.

The quantitative approach to value investing: The evidence

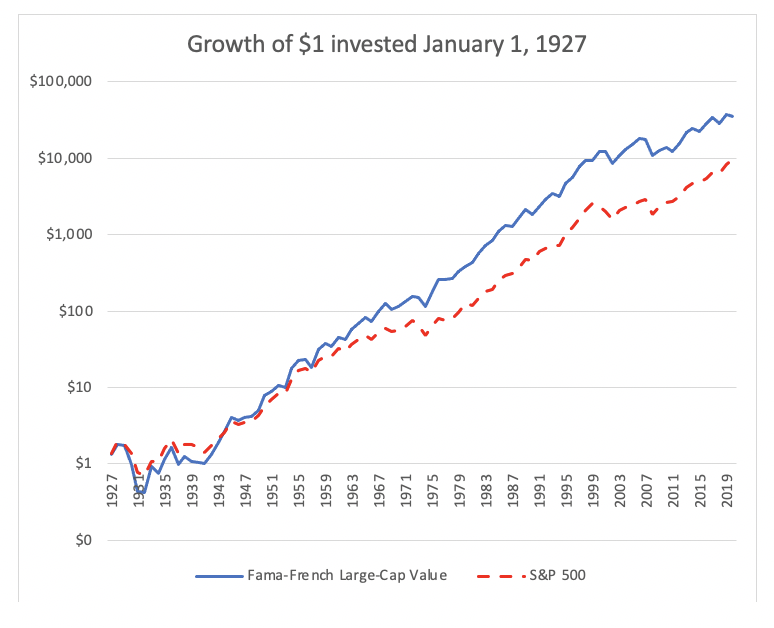

Let’s look at Fama and French’s data for returns to their factors. You’ll see why quantitative investors have been strongly biased toward value investing. (Technical details: The best data that we have for historical returns in the United States were assembled, in the 1980s, back to 1926, and the data series have been maintained since then, and that’s why these charts begin shortly after that year. That’s a fine long run of history. Fama and French are here looking at the stocks of larger companies, and of those, they are defining as “value” stocks the 30% with the lowest ratio of price to book value, which they recalculate every June 30. Keep in mind that theirs is only one of several definitions of value stocks. Note that the vertical axis of this graph shows a logarithmic scale, which is to say, the scale of dollars grows in powers of 10; hence the leaps in the labels on the vertical axis.)

In the graph, you can’t really see the comparative volatility of the series. Quantitative analysts use volatility as a rough-and-ready measure of risk. But trust me: Even after taking risk into account, the value series is very impressive.

One dollar invested in large-company value stocks at the beginning of 1927 would have grown to $35,761 at the end of 2020. One dollar invested in the S&P 500 (or its equivalent in the years before the index was created) would have grown to only $9806 over the same span of years.

Strategic and tactical value investing

No question about it: If you intend to put together a buy-and-hold portfolio of stocks, you want it to consist of value stocks, not growth stocks.

You could be a very sophisticated value investment manager, or a naïve value investment manager, a quantitative one, or a fundamental one, but whatever the case, you would now have evidence to back up your expectation of superior returns.

Note that I said “buy-and-hold.” The entire point of considering the long-term outperformance of value stocks is its implication for a long-term strategy: You’d want to emphasize value stocks to the extent that you have a long-term strategy of including stocks in your portfolio. Sure, you might sometimes increase or lessen the proportion of value stocks in your portfolio if, in the teeth of market efficiency, you believe you have just cause to adjust for changing expectations, but these would be tactics overlaid on a long-term strategy. If you have no long-term strategy, but instead trade in and out of investments that look to you attractive or unattractive, then you might sometimes hold value stocks, sometimes not. No one has ever thought – or had evidence to show--that value stocks always outperform, month after month. This non-strategic, purely tactical investing, though, is not our concern here.

Simple is good enough

Sophisticated quantitative value investment managers devote their efforts to “cleaning” the stock market data that they use, to refining their definitions of “value,” and perhaps to building better factor models. It’s proverbial in the profession that some stocks are “cheap for a reason.” Their growth prospects are poor. This is why Graham, and later Greenblatt, placed equal emphasis on the identification of companies that had solid business propositions. Furthermore, the basic financial statement data reported in (expensive) databases may be misleading. Perhaps a close reading of the notes in the financial reports can produce correctives to the prominent income statement and balance sheet data. So, the sophisticated quantitative value managers are automating some of the deeper analyses carried out by the more scrupulous of the fundamental Graham-style investors in trying to distinguish the genuine value stocks from the rest.

The naïve value investment managers – and I count myself among them – don’t worry about refining the data. I don’t employ PhDs in finance and accounting to get an edge on other value investors through more ingenious number crunching and subtle blending of different value factors, but then again, I also don’t charge hedge fund fees. But there’s a perfectly adequate way to be a value investor without much added effort: Buy a value stock index fund. These are index funds that start by taking the universe of stocks, next sort them on one or another “value” criterion, like the price-to-book value ratio, and then buy, say, the cheaper half, or the cheapest 200, or whatever. One very popular example, the Vanguard Value exchange-traded fund (VTV), is based on an index of 325 stocks selected through a methodology that “classifies value securities using the following factors: book to price, forward earnings to price, historical earnings to price, dividend-to-price ratio and sales-to-price ratio.”

Sure, this simple approach will accidentally scoop up stocks that are “cheap for a reason.” But then, the original quantitative research that discovered and validated the value anomaly similarly did so with vast unrefined quantities of value stocks, not with artisanal value portfolios carefully handcrafted by highly-compensated data scientists and accounting experts. Maybe the gilded lily really is worth more, but I’ll take just the plain lily, thank you very much.

Furthermore, because a majority of stocks (more internationally than in the U.S., but in the U.S., too) over the last thirty years and very probably longer have not even produced a return exceeding that of U.S. Treasury bills (think: the return you get from money market funds) and in many instances did much worse, the chances of creating a dud portfolio of, say, only 30 stocks chosen not randomly but by systematic mistake are unacceptably high, and this is likely as true of value stocks as of the stock market as a whole. This fact is one argument for total stock market index funds that applies with equal force to value stock index funds.

Taking stock

Let’s look back over the arc of development of value investing: Beginning as an approach to identifying stocks that are superior investments, value investing was simplified and generalized and proven to be an empirical exception, over long spans of time and in many stock markets, to the theoretical rule that you cannot beat the market after taking risk into account; from there, investment theory was changed to incorporate this discovery so that it was no longer an exception, but part of the mathematical models that explained how stock markets work.

Today, all these ways of thinking about value investing are concurrently held by different investment professionals. It’s like evolution without selection: The ancestral forms coexist with their descendants.

Price goeth before destruction

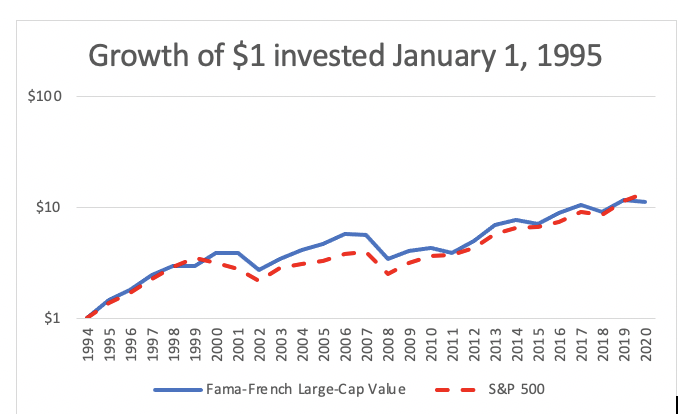

The last quarter-century has seen the value stock anomaly evaporate. Here is the same graph I showed earlier, but with one change: It shows the growth of a dollar invested at the beginning of 1995, rather than 1927.

One dollar invested in large company value stocks at the beginning of 1995 would have grown to $11.26 at the end of 2020. One dollar invested in the S&P 500 (or its equivalent in the years before that index was created) would have grown to $13.48 over the same span of years. The last decade was even worse, with value stocks underperforming in seven of the ten years (though they had a very good 2016).

Not only have value stocks underperformed, but at the worst moment in recent stock market history, the market bungee jump at the moment that the COVID-19 pandemic hit the United States with force, when you might have expected that value stocks, having been tied to the rigid frame of true value by the shortest cord, would fall the least, they plummeted much further than the market as a whole. There’s a plausible explanation: The big “tech” stocks – no value stocks they – were those of companies with the best business models for taking advantage of consumers’ needs during lockdowns and restricted economic activity. All the same…mightn’t the value stocks have been less dangerous than they turned out to be?

Early last year, before the pandemic, I took a fresh look at Fama and French’s own historical data for returns to the value stocks of large companies and the value stocks of small companies, and after a detailed analysis that I am sparing you here, I concluded that, for large companies, the value effect disappeared at least 25 years ago. There was evidence that for smaller companies, it has still persisted, but in a more attenuated form (by which I mean that there were fewer years than previously of outperformance by value stocks of small companies, and the extra return was, on average, smaller). Unknown to me at the time, Fama and French had themselves just been taking a fresh look at their data, and as I was completing my analysis, they published their results. They, too, concluded that the value effect had disappeared, meaning that they had to revise their model. (Unlike me, they concluded that the value anomaly for all stocks, not just those of large companies, had vanished; this was because they adjusted, as I did not, for yet another anomaly: that the stocks of small companies tend to outperform those of large ones.)

What happened?

So, what happened?

Well, if your first reaction is that this is a passing episode, and value stocks will eventually return to their long-term behavior, then you have an exceptionally sunny disposition. Greenblatt cautioned that one reason that his “magic formula” probably worked was that it “works in the long run (meaning it sometimes takes three, four, or even five years to show its stuff),” and impatient investors would give up on it, thereby keeping the market inefficient. But 25 years is a much longer run than “even five years.” You may be patient, but how much longer will you wait while other investors figure out that their valuations were wrong and value stock prices make up for the last quarter century?

Let’s remember that value investing is a castle in the air; the only reason that some theories incorporate it is that they are they are designed to fit the evidence. The reasons behind value investing remain mysterious.

There have always been attempts to explain the value phenomenon or anomaly. The quantitative analysts kept framing hypotheses that there were risks that justified the higher returns, until they gave up and hypothesized that value was its own risk factor. The fundamental analysts, not believing in market efficiency, just assumed that they were finding mis-priced stocks. They probably were, but not noticing that hundreds of other stocks that they hadn’t identified were also mis-priced at the same time.

If, on the one hand, you believe that the stock market is not efficient, in the way that Benjamin Graham believed it was not, then, that the value phenomenon ever existed at all should still perplex you. That’s because Graham wasn’t arguing that, say, 30% of the stock market in aggregate could be inexpensive while the rest was at fair value or overvalued; he was giving guidance on identifying truly undervalued stocks. There was no need to write an entire textbook on stock analysis if all you have to do is skim off the bottom 30% of the market with below-average price-to-book-value ratios. Actually, he did argue that the entire stock market could be undervalued or overvalued, but when he was writing, although there were stock indexes, there were no index funds, and investors therefore had no alternative to choosing individual stocks or paying someone to choose individual stocks for them; now, of course, you can either buy (and sell) the entire market with a single transaction, or pick individual stocks. Much earlier, I wrote that followers of Graham “of course” do not buy all stocks that look cheap, but why not? As a modern follower of Graham, why are you picking individual stocks when you know that you can buy a value index fund when you think that stocks are undervalued? Don’t you think it looks just a tad smug to argue that most people who trade stocks enough to move their prices aren’t as wise, individually and collectively, as you are? That is possible, but to an onlooker, it smacks of self-deception.

If, on the other hand, you believe that the market prices stocks efficiently, then including some sort of value factor or factors in your model is still unsatisfying when you think deeply about it. Why is there a value factor? Even if you disagree that market efficiency holds in the real world, you can see how, if forced to assume the premises that, first, when vast numbers of intelligent and highly motivated participants instantly react to economic news, prices will immediately adjust to any new tidbit of news, and second, the consensus of all forecasters is almost always more accurate than the judgments of the overwhelming majority of individual forecasters (something that has been demonstrated in many contexts, not just investing), then there is, indeed, a “why” for market efficiency. There is, however, no “why” that one or more value factors systematically drive an enormous fraction of the stock market, over a long span of time, to outperform the average.

Even a mathematical investing model that takes stock behavior to be fundamentally irreducible to a single factor, and includes a value factor as basic to stock behavior, begs the question. It looks like a theoretical construct, but actually it’s an empirical fit to the data without a good reason behind it. That makes it unlike the single-factor model of stock behavior, which may be – and actually is – wrong, but can be justified in economic theory from first principles. Sure, reasons may be hypothesized, but as I said before, these reasons haven’t been nabbed in the act by economic detectives seeking evidence.

This by itself does not shame financial economics as a social science, making it inferior to, say, the hard science of physics. Physics has had similar explanatory deficits. One reason for Isaac Newton’s great success was that he refused to be stymied by a lack of explanation for why gravity worked. As he famously declared, “Hypotheses non fingo” (I don’t frame hypotheses), and he proceeded to model, mathematically, how it worked. For some of his contemporaries, this was wrong: One physical body can’t act on another at a distance, across space, without an actual mechanism for conveying that action from the one to the other, which is what Newton appeared to assume. (For an entirely different conundrum in fundamental physics almost 250 years later, Einstein, who had explained gravity, coined the memorable expression “spooky action at a distance” – “Spukhafte Fernwirkung.”) And even today, physicists model behavior that they can’t explain, like that of dark matter (though they do frame hypothetical explanations that remain unproven). There remains a difference between financial economics and physics, though: We assume that how the physical universe works remains unchanging, even as our understanding of it changes, whereas the universe of markets, the creation of human beings, is not unchanging.

All the same, if it now turns out that value investing is not a universal phenomenon, and so doesn’t require explanation, I, for one, would still like to know why it once existed, and in so many different stock markets. But, as Buddy Holly sang, I guess it doesn’t matter anymore.

And so, depending upon how skeptically you regard the evidence for market efficiency, you may or may not have been surprised when the wheels came off value investing over the last couple of decades. Not to be overly delicate about it, value investors have been creamed, and that goes for both the fundamental investors who pore over financial statements in the manner of Graham, and the hedge fund managers with their PhDs in finance, constantly refining their computer models.

An alternative hypothesis

Today, the dominant and pressing question for many professional investors and financial economists is not, why was there a value anomaly or factor in the first place, but, instead, why has it ceased to exist? So many have lived with the value phenomenon for so long that, so they believe, it is a truth universally acknowledged that an investor in want of a good fortune must be a value investor.

One possible explanation for the dissipation of the value phenomenon is that, precisely because it became universally familiar, its advantage was traded away. (In our profession, the current vogue jargon for saying that the market has latched on to something is “crowded trade.”) One flaw in this argument is the very fact that the anomaly undeniably persisted, puzzling as it may be, for years after it was not just suspected, but rigorously proven to exist; this makes it difficult to believe that investors traded away its advantages only in or around 1995. Proponents of value investing were always aware that its persistence needed explanation. Joel Greenberg offered what I suspect was a common explanation: That most investors lack the patience to hold onto value stocks through the long periods (“three, four, or even five years”) during which they may underperform the market indices. The ants will always come out ahead of the grasshoppers, because the grasshoppers will never learn.

Many proponents of value investing find it difficult to stomach this explanation – that the market has now latched on to value investing – not because if it were correct, it should have happened sooner, but for different reason, one that confirms their beliefs: That today’s value stocks, by any of the usual valuation measures, appear to be very, very inexpensive, and so it seems more obvious than ever that the market is pricing them incorrectly. But one rejoinder to this argument is that the value anomaly was indeed traded away, and therefore most of today’s “value” stocks are now “cheap for a reason,” that is, their growth prospects are comparatively poor. I’m not saying that I think they are, only that it’s a possible alternative explanation to the market’s being perverse, flippant, foolish, or ignorant.

The defenders of value investing have proffered a number of hypotheses that explain why the value anomaly only appears to have gone away, and why we should expect it to return. A pair of academic papers, by different authors, in the two most recent issues of the Financial Analysts Journal (which is really a journal for practitioners, but follows academic standards for publication and whose articles are often written by academics) are the latest in a swelling academic literature to set out these hypotheses thoroughly and go beyond common handwaving excuses.[1] One of these papers states and critiques the several hypotheses that explain what happened to the value anomaly, and the other presents a more thorough analysis of the one that seems best to hold water.

This hypothesis (which has been adduced by other writers in the last few years), is that intangible assets, as distinct from tangible ones, that is, physical ones or readily observable ones (like investments in R&D), have in the last twenty years or so come to represent more of the total assets of a firm. The book value reported in corporate financial statements does not capture all of the intangible assets. Seen this way, many companies that appear, from traditional calculations, to have low book value may actually hold assets of much greater value than is reported, and so these should not necessarily be considered “value” stocks, and many other stocks are less undervalued than they were seen to be.

Both of these papers examine the data and find that the nature of corporations has indeed changed in the last couple of decades, so that intangible assets do account for a larger proportion of the total assets held by companies. The second paper, which applies a somewhat different methodology, finds that the degree of this effect varies across different industries, and is actually more pronounced abroad than at home, in the U.S. It also argues that the invisibility of intangible assets in traditional calculations also affects earnings estimates, with the result that yet another value measure, the earnings-to-price ratio, has been putting into the “value” category stocks that don’t belong there. The first paper furthermore shows that, after recalculating book value to take into account intangibles (again, by these authors’ methodology, which is not something universally agreed), both the duration and the depth of the poor performance of value stocks is less than it appears to have been. But – and this is important – the paper shows that the failure to capture intangible assets in value calculations still does not explain all of the recent underperformance of value stocks.

What next?

As I write this conclusion, value stocks in the U.S. have been on a tear, beating the S&P 500 for most of the last six months. (At press time, this has very recently reversed.)

Something like this was bound to happen sooner or later. Some analysts have been forecasting it for years. The first of the two articles I cited a moment ago – probably written around the middle of 2020, because it takes a while for a properly vetted article to wend its way from the writing desk past reviewers and into print – made the case that valuations, based on the book-to-price measure, could hardly get much lower without implying that value stocks should have negative returns, not a logical impossibility but an economically indefensible one, and that even a modest reversion to the average (actually, in their analysis, median) valuation should produce a very healthy return. The authors conclude, however, with the inevitable caution: “Although value strategies seem as attractive as they have ever been…an elevated expected return is not a guarantee that value must outperform growth in the years ahead.” (Emphases theirs.)

The questions are, will this superior performance that we’ve been seeing persist, and even if for now it is short lived, by how much will the return on value stocks have exceeded that on the broad stock market when this surge ends?

Value stocks will always be an option for tactical investing. And by tactical investing, I don’t mean that value stocks will become the latest fad, “meme stocks.” Value stocks as meme stocks is an oxymoron. Meme stocks are the most flippant of growth stocks, maybe so much so that they aren’t even growth stocks, either. Our investing conversations have lately been drowned out by noisy babble about the meme stocks and their promoters, but the whole point of value stocks is that they’re tied to actual valuations, which meme stocks are not. As for tactics: There ought to be economic reasons for value stocks to outperform the rest, based on numbers and not so much on narratives unrelated to measurable assets and sources of corporate revenue. John Authers, one of the more perspicacious and most prolific of investment commentators, recently wrote of the present moment, “We can see that profit growth is much less scarce than it appeared to be a year ago. That means an epic correction for growth stocks, and a rally for value stocks.” More than a year ago, however, he was forecasting that the time for value stocks had come, when this reason didn’t hold. Maybe he was right then and a little early, but who can say? Choosing to invest in value stocks at the right moment will forever be an investor’s option, but this will be bootless unless she can correctly time (even with imprecision) the moves into and out of value stocks.

In light of what I wrote earlier about factor investing, it follows that I believe that the right way to go about tactically investing in value stocks is not to trade in and out of them, but rather to increase or decrease a portfolio’s exposure to them in proportion to one’s confidence that they will outperform the market and by how much; that is, in the simplest form, increase or decrease portfolios’ holdings of a fund like Vanguard’s VTV.

I am reasonably confident – but still not entirely certain – that the value anomaly, as an anomaly, is no more, at least for large companies. It could, indeed, continue roaring back, but in doing so, it would have to best the broad stock market indexes either by an enormous amount in a short span of time, or a still very large amount over a long period of time for it to wipe out, statistically, its long record of underperformance and to persuade us that we can once again put our faith in it. I’ll continue to place some confidence, but less than I did before, in a strategic position in small company value stocks – and think very hard about whether I trust my judgement in timing moves into large company value stocks.

Granted, I tend to think like a quant, and in this, I am unlike the majority of investment professionals, who were not trained as quants and don’t break bread or drink with quants and economists. These others are not thinking in terms of factor exposures. For that matter, they may not even be thinking of strategies. Those with a “value” bent are likely upholding the article of faith that, in the long run, the skillful selection of stocks that are underpriced will always produce returns superior to those of a boring and average index fund. But this faith has blinded them to the possibility – I would say likelihood – that most of those who were once successful (and not many of them were) were coasting along on the value anomaly. If the anomaly is truly gone, then the long-run future results of most of these formerly successful value managers will be mediocre. (To be sure, and as I’ve already said, I don’t know of anyone, not even Eugene Fama, who would deny that there are a very few talented stock-pickers.)

But let’s not begrudge the value managers the happiness of the last six months. And I, who am not a value manager, now hold a modest tactical position in value stocks.

Adam Jared Apt, CFA, is a financial advisor and the owner of Peabody River Asset Management, based in Cambridge, MA.

[1] Robert D. Arnott, Campbell R. Harvey, Vitali Kalesnik, and Juhani T. Linnainmaa, “Reports of Value’s Death May Be Greatly Exaggerated,” Financial Analysts Journal, Vol. 77 No. 1, First Quarter 2021, pp. 44-67.

Amitabh Dhugar and Jacob Pozharny, “Equity Investing in the Age of Intangibles,” Financial Analysts Journal, Vol. 77 No. 2, Second Quarter 2021, pp. 21-42.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits