Three Strategies to Strengthen Household Balance Sheets

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This article is a follow-up to excellent Advisor Perspectives articles by Joe Tomlinson, The Bright Side to 2022’s Annus Horribilis for Investments, and William Bernstein, Playing Inflation Russian Roulette in Retirement. Tomlinson’s article reminded financial advisors to “be cognizant of both sides of the financial planning balance sheet” when advising clients. Bernstein’s article compared the financial benefits and risks of implementing a TIPS ladder versus purchasing a single premium life annuity (SPIA) in today’s economic environment.

In this article, I will use an example and an actuarial model to compare the efficiency of the following three strategies for strengthening a retired or near-retired client’s balance sheet under both a lower and a higher assumed future inflation scenario:

- Delaying commencement of Social Security benefits until age 70;

- Purchasing a SPIA; and

- Implementing a TIPS ladder.

I will make the comparisons on an “apples to apples to apples” basis by assuming the same 30-year lifetime planning period and client costs for each strategy.

Delaying Social Security is more efficient than the other two strategies under both assumed inflation scenarios, assuming no changes in Social Security law. But a client’s investment in this strategy (or cost) is effectively limited to the present value of the estimated extra withdrawals from the client’s accumulated savings during the commencement delay (or bridge) period. As noted by Bernstein, the TIPS ladder strategy can be more efficient than the SPIA strategy during periods of relatively higher inflation and vice versa during periods of relatively lower inflation.

Example

Ralph is a 65-year-old single male retiree. As of January 1, 2023, his retirement assets consisted of the following:

- An immediate Social Security benefit of $18,000 per annum;

- An immediate lifetime pension benefit of $12,000 per annum; and

- $750,000 in accumulated savings invested 70% in non-risky investments and 30% in risky investments.

His desired spending plan includes the following annual recurring expenses, each of which increases with inflation:

- $41,000 per annum in essential expenses assumed to increase each year with inflation;

- $3,000 per annum in discretionary expenses assumed to increase each year with inflation; and

- $5,000 per annum in discretionary expenses expected to remain constant in nominal dollars 0 year.

His spending plan includes the following non-recurring expenses:

- $0 in long-term care expenses (assumed to be funded by his home equity);

- Present value of $25,000 for unexpected expenses;

- Annual home mortgage fixed dollar repayments of $20,000 per year for five years (considered an essential expense);

- A new car assumed to be purchased when Ralph is age 70 for $30,000 increased with inflation (considered 50% essential and 50% discretionary);

- Annual travel expenses of $10,000 per year assumed to increase with inflation for the next 15 years (considered to be 100% discretionary); and

- Desired estate at the end of lifetime planning period of $20,000 in today’s dollars (considered to be 50% essential and 50% discretionary).

His 2023 assumptions about the future (lower inflation scenario) include:

- 4.5% per annum investment return on non-risky assets/investments;

- 7.5% annual investment return on risky assets/investments;

- 3.5% per annum annual inflation increases; and

- Lifetime planning period of 30 years.

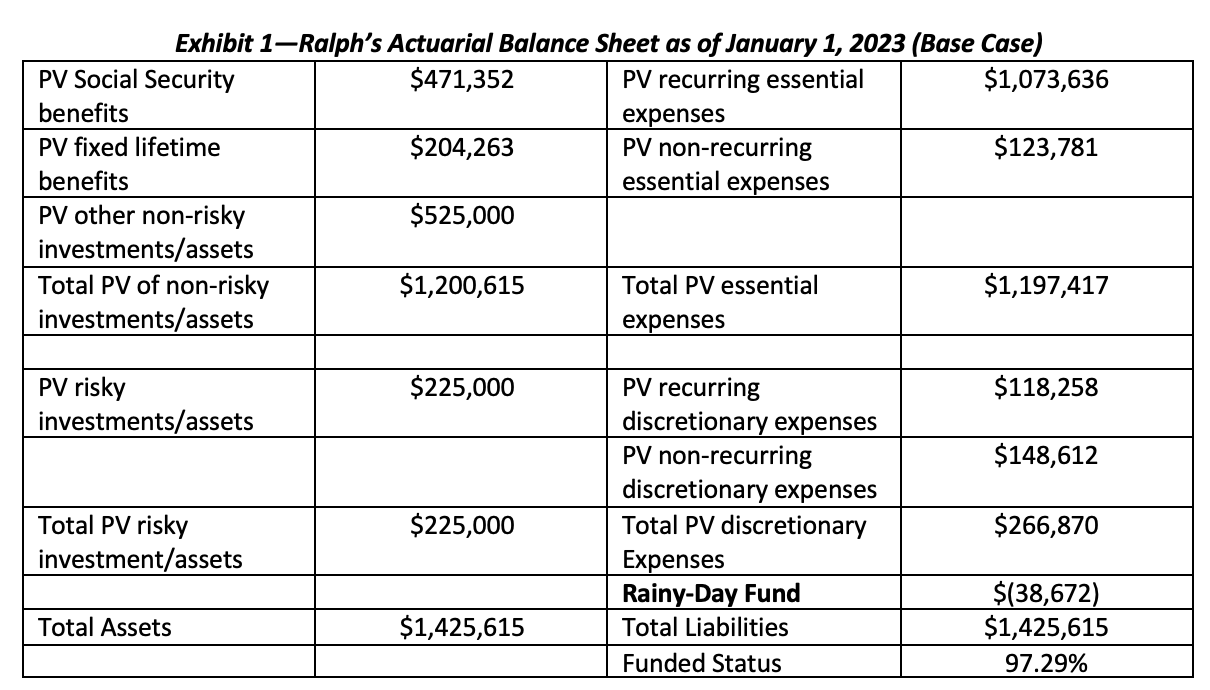

Entering the above data and assumptions in an actuarial model1 produced the following balance sheet for Ralph as of January 1, 2023:

Ralph prefers the safety-first investment approach. He and his financial advisor have structured his accumulated savings to approximately match the present values of his non-risky assets/investments and essential spending liabilities. He considers his investments in bonds to be non-risky for this purpose.

Exhibit 1 shows that Ralph has a negative rainy-day fund as of January 1, 2023, and as a result, the model shows his personal retirement plan funded status (total assets / (total liabilities – rainy day fund) to be 97.29% under the assumptions and data entered in the model.

While he is not overly concerned about having a small negative rainy-day fund (or funded status of 97.29%), he wonders if there may be relatively simple financial strategies he can implement to increase his personal retirement plan funded status that do not involve actions such as:

- Going back to work;

- Reducing planned discretionary spending; or

- Renting out a room of his house for extra income.

His financial advisor suggests the following three possible strategies:

- Delaying commencement of Social Security until age 70;

- Selling some of his bonds and purchasing a SPIA; or

- Selling some of his bonds and implementing a TIPS ladder.

Ralph’s financial advisor calculates that under the model assumptions for investment return and inflation noted above, his Social Security benefit would increase from $18,000 to $30,587 per annum at age 70 (in nominal dollars) if he delays commencement until age 70. She also calculates the present value of extra withdrawals from Ralph’s accumulated savings to pay for the stream of real dollar amounts that would “bridge” to $30,587 at age 70 to be $126,325. To facilitate the comparison of the three strategies, she suggests that this amount be used as the value of bonds to be sold to purchase the SPIA and TIPS ladder.

Ralph’s financial advisor uses the ImmediateAnnuities.com December 10, 2022, rate of $655 per month for a $100,000 premium for a 65-year-old male to SPIA with an annual payout of $9,929, and uses Bernstein’s TIPS real draw of $3,494.73 per month for a $1,000,000 investment to develop a cost-equivalent TIPS inflation-adjusted annual 30-year payout starting at $5,298. In both these scenarios, the amount remaining in Ralph’s accumulated savings after purchase would be $623,675 ($750,000 - $126,325)

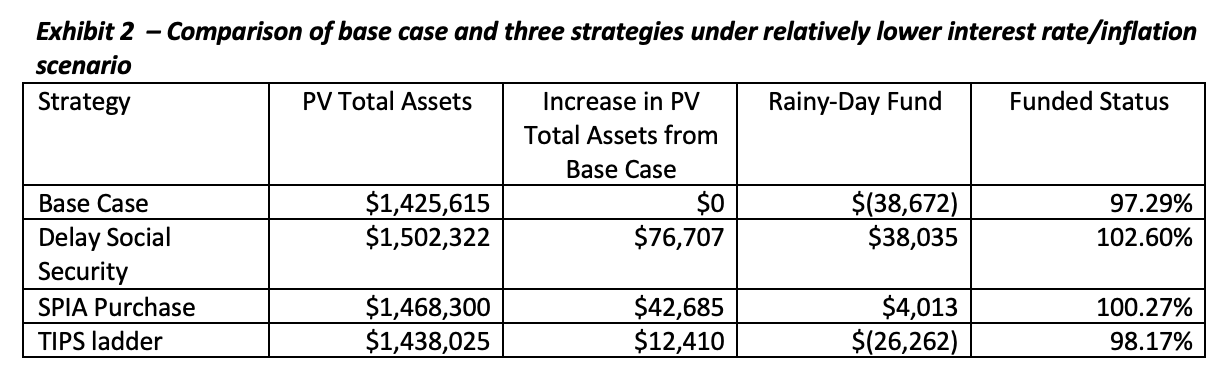

The results of the comparison are shown in Exhibit 2 below:

Exhibit 2 shows that, under the assumptions used for this comparison, for each $1.00 of strategy cost:

- the delay Social Security strategy generates a $0.61 increase in Ralph’s assets;

- the SPIA purchase strategy generates a $0.34 increase in Ralph’s assets; and

- the TIPS ladder strategy generates a $0.10 increase in Ralph’s assets.

Ralph understands that while the delay Social Security strategy is much more efficient at increasing the value of his retirement assets than the other two strategies, his investment in this strategy is limited to the present value of his Social Security bridge payments. This strategy is also subject to the risk that future Social Security benefits may be reduced in some manner, such as through means-testing, higher taxes or lower cost-of-living increases.

As noted by Bernstein, the SPIA strategy is subject to insurance company failure risk and can lose purchasing power in the event of higher inflation, while the TIPS ladder strategy does not benefit from insurance company pooling and is subject to longevity risk. Neither of these two strategies is limited like the Social Security strategy, so if Ralph wanted to use more than $126,325 of the non-risky assets in his accumulated savings to purchase an annuity or set up a TIPS ladder, he could.

Ralph’s financial advisor suggests that they look at a higher interest rate/inflation scenario to see how the base case and three strategies fair.

Ralph’s financial advisor suggests the following assumptions for the higher interest rate/inflation scenario:

- 6.5% per annum investment return on non-risky assets/investments;

- 9.5% annual investment return on risky assets/investments;

- 5.5% per annum annual inflation increases; and

- Lifetime planning period of 30 years.

Ralph’s financial advisor also assumes that the current value of Ralph’s non-risky assets ($750,000 before annuity purchase and $623,675 after) would not change as a result of these higher assumed interest rates.

Under these assumptions, Ralph’s financial advisor recalculates his expected annual age 70 Social Security benefit if he defers commencement to that age to be $33,659 and calculates that the present value of Social Security bridge payments would be about the same as under the lower-inflation scenario ($126,325).

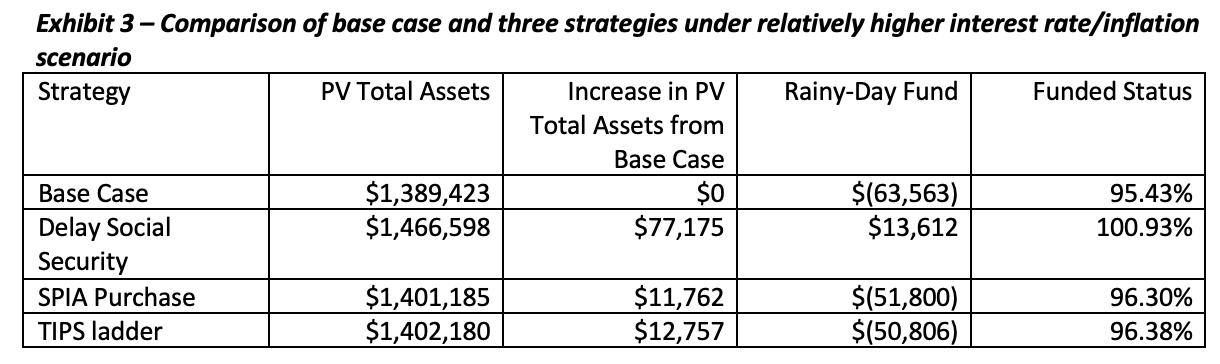

The results of the comparison of the base case and the three alternative strategies under these higher interest rate/inflation assumptions is shown in Exhibit 3 below:

The delayed Social Security strategy is still the most efficient. The TIPS ladder strategy, while about as efficient as in the earlier scenario when compared with the base case, is now more efficient than the SPIA purchase strategy, since as noted by Bernstein, higher assumed rates of future inflation/interest rates will decrease the value of the fixed dollar life annuity.

Summary

My results differed slightly from those produced by Bernstein because I employed different methodologies and assumptions, and I used more current annuity purchase rates. Bernstein made his comparisons using less favorable joint and survivor annuity purchase rates available last month. My results do, however, support his contention that a TIPS ladder can be more efficient than a SPIA as a relatively low-risk approach for providing inflation-indexed income to retirees if inflation is expected to be relatively high over the household lifetime planning period (greater than or equal to 5.5% per annum) and real rates of return on less-risky assets/investments are expected to be relatively low (1% or less). Assuming current Social Security law, however, neither strategy beats deferring commencement of Social Security benefits under reasonable assumptions.

The Federal Reserve Board appears to be tackling the problem of higher-than-desired levels of inflation by aggressively raising Federal funds interest rate, but it is unclear how successful its efforts will be. The 2022 OASDI (Social Security) Trustees Report provides some guidance with respect to assumptions about future rates of inflation and expected real rates of return on non-risky investments. While the Trustees underestimated the rate of inflation in 2022, they assumed (under the intermediate assumptions) that inflation will be back to 2.4% for 2023 and later, and the real rate of return on the special-issue government bonds held in the OASDI trust will increase to over 1% after five years, over 2% after eight years and ultimately reach a rate of 2.3% after 10 years. Even if these assumptions are wildly optimistic, the default assumptions in my actuarial model of 4.5% nominal investment returns on non-risky investments (1% real) and 3.5% inflation are conservative, and under those assumptions, today’s SPIAs are more efficient than establishing a TIPS ladder as illustrated in Exhibit 2. To strengthen a client’s balance sheet, assuming the client is already deferring commencement of benefits until age 70, consider the benefits of purchasing an SPIA.

Ken Steiner, FSA, is a retired actuary with a website entitled "How Much Can I Afford to Spend in Retirement."

1The actuarial model used for this example is the Actuarial Financial Planner for Single Retirees and is available in the spreadsheets section at How Much Can I Afford to Spend in Retirement? Amounts in this exhibit may not add to the total due to rounding.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All