The Federal Reserve’s tightening of monetary policy in March, raising interest rates .25% to a 16-year high of 5.0%-5.25%, combined with quantitative tightening (reducing its balance sheet) has led many economic forecasters to predict a recession. I have been receiving questions from advisors about what they should do.

The Federal Reserve’s tightening of monetary policy in March, raising interest rates .25% to a 16-year high of 5.0%-5.25%, combined with quantitative tightening (reducing its balance sheet) has led many economic forecasters to predict a recession. I have been receiving questions from advisors about what they should do.

When answering this question, I always point out the most important insights for investors to remember: Markets are forward-looking; they incorporate all available information into current prices; and recessions are only declared by the National Bureau of Economic Research (NBER) after the fact (we know they were recessions only in hindsight, and economic data is reported with lags).

With that in mind, we can examine the historical evidence. The following table, covering the six recessions since 1980, shows the number of months from the NBER declaring a recession until the market low. Because recessions are proclaimed with a delay, markets are often well on the way toward a recovery by the time of the announcement – the stock market had already bottomed prior to the announcement month in four of the six recessions since 1980. In 2020’s recession, the market’s low point was in March, three months before the announcement in June.

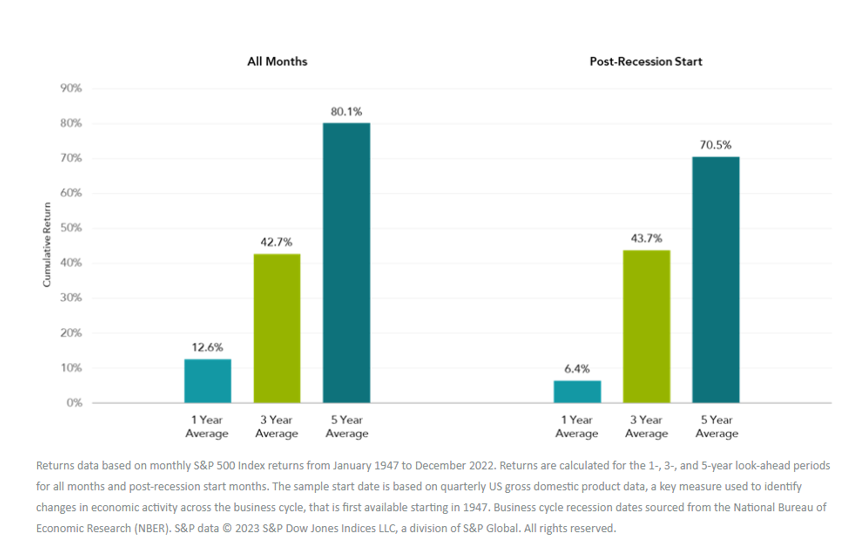

Though it is likely to surprise most investors, the table below shows that average U.S. equity returns have been positive after the onset of a recession:

That returns have been both positive and similar in both sets of data is consistent with the theory that markets are forward-looking. Even with the benefit of hindsight, and ignoring expenses and taxes, there isn’t much evidence to support a timing strategy based on a recession forecast.

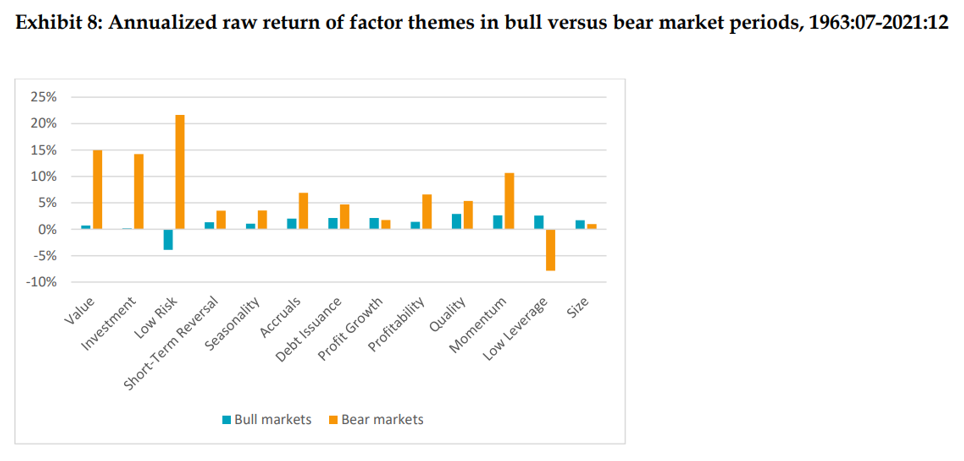

I’m also often asked about the performance of factors in different market regimes: If one is worried about a bear market, are there factors that are more defensive (tend to perform relatively better in bear markets)?

Factor performance in bear markets

David Blitz, author of the May 2023 paper “The Cross-Section of Factor Returns,” examined the performance of 13 major factor themes (value, investment, low risk, short-term reversal, seasonality, accruals, debt issuance, profit growth, profitability, quality, momentum, low leverage and size) during bull and bear markets over the period July 1963-December 2021. As seen in the following chart, Blitz found that all but the size and low-leverage themes earned most of their premiums during bear markets, demonstrating their ability to provide diversification benefits because of their defensive nature. Factors are long-short portfolios.

The value of market forecasts

If economic forecasts are nonproductive, what about the forecasts of the market? Songrun He, Jiaen Li and Guofu Zhou, authors of the March 2023 study, “How Accurate Are Survey Forecasts on the Market?,” sought to answer that question. They examined three sets of survey forecasts on the market return:

-

The Livingston Survey (LIV), a biannual survey (June and December every year) about the U.S. economy, and the S&P Index in particular, conducted by the Federal Reserve Bank of Philadelphia. The surveys are drawn from practitioners and economists (professional forecasters) from industry and academic institutions. About 90 participants are on the mailing list, of which 55 to 65 respond to the survey each time.

- The Nagel and Xu (NX) survey, which consolidates various data sources, including the UBS/Gallup survey, the Conference Board survey and the University of Michigan Surveys of Consumers, to form a representative survey of a typical U.S. household.

Here is the summary of their key findings:

- None of the survey forecasts beat a simple random walk forecast that predicted the future returns by using their past sample mean.

- For a mean-variance investor with typical risk aversion who allocated between the market and risk-free asset, the investor would have been substantially worse off (losing 1% to 18% per year) switching from a random walk belief to using one of the survey forecasts.

- While both professionals and individuals failed to outperform the naive prediction of the historical average, the professional-forecaster survey expectations produced even worse results (R-squared ranging from -51.69% to -12.47%) than individual investors (R-squared = -0.42%).

Investor takeaways

The most prudent strategy is to ignore the “noise” of the market and adhere to your well-thought-out asset-allocation strategy that acknowledges both the virtual certainty of recessions and bear markets while also recognizing that trying to time the market based on economic forecasts is likely to prove counterproductive. Risk-averse investors may want to consider diversifying their portfolios to include exposure to the more defensive factors. One of the most interesting, and perhaps surprising, results is that despite their greater financial literacy, the professional forecasters produced significantly worse forecasts than the average household. Market forecasts should be ignored, whomever they come from – professional economists or market gurus. That’s the warning Warren Buffett offered in his 2013 letter to Berkshire shareholders: “Forming macro opinions or listening to the macro or market predictions of others is a waste of time.”

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this article.LSR-23-511

Read more articles by Larry Swedroe

The Federal Reserve’s tightening of monetary policy in March, raising interest rates .25% to a 16-year high of 5.0%-5.25%, combined with quantitative tightening (reducing its balance sheet) has led many economic forecasters to predict a recession. I have been receiving questions from advisors about what they should do.

The Federal Reserve’s tightening of monetary policy in March, raising interest rates .25% to a 16-year high of 5.0%-5.25%, combined with quantitative tightening (reducing its balance sheet) has led many economic forecasters to predict a recession. I have been receiving questions from advisors about what they should do.