Would Charles Darwin Have Been a Good Investor?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Pulak Prasad is a successful investor in the Indian market, where he grew up. But he is also an amateur evolutionary biologist. His new book illustrates a powerful – and often money-making – link between the disciplines of investing and evolution.

Pulak Prasad is a successful investor in the Indian market, where he grew up. But he is also an amateur evolutionary biologist. His new book illustrates a powerful – and often money-making – link between the disciplines of investing and evolution.

I wanted to write Pulak Prasad’s What I Learned About Investing from Darwin, or something very much like it, 40 years ago. My first published article, written in 1982, began: “The economy of man was Charles Darwin’s inspiration for his theory of natural selection.”1 I then quoted Darwin:

I happened to read...Malthus on Population, and being well prepared to appreciate the struggle for existence which everywhere goes on from long continued observation of...animals and plants, it at once struck me that under these circumstances favorable variations would tend to be preserved and unfavorable ones to be destroyed. The result of this would be the formation of new species.2

My article then outlined the ways in which evolution and economics are similar, explaining changes as the result of variation and natural selection. Clearly, there’s a book in there somewhere. It is just as well that I did not write it, because Prasad has done so with knowledge of both markets and evolution vastly superior to what I had at age 28.

Prasad’s book is excellent but has some faults. It’s oriented to the art of stock picking, his bottom-up way of trying to achieve alpha. But many of his readers are not stock pickers – they’re asset and manager allocators or wealth managers, disciplines he could have addressed but did not. Another downside of Prasad’s book is that the connections between evolutionary theory and investment management sometimes feel forced. But Prasad writes about biology and evolution with the brio of a gifted science teacher, a most welcome change from the prosaic tone that characterizes so many investment books.

Prasad has a deep understanding of the ways in which ideas from evolution apply to businesses and the economy, and thus to investment management. I wish he had spent more effort on the ways in which they don’t apply, but I recommend this book with considerable enthusiasm.

Three rules for winning

Prasad makes two Warren Buffett-like recommendations for managing an active equity portfolio successfully...

- Don’t lose money – which he translates into “don’t take big risks,” because it’s impossible to entirely avoid losing money if you’re buying equities.

- Buy high-quality companies at a fair price.

...and one that I associate with Jack Bogle:

- Don’t be lazy – be very lazy

The book is organized around these three themes, in each case relying on links between Darwin’s evolutionary theories and the economics behind active equity management. But, for brevity, I won’t cover these topics in the order in which Prasad presents them. Instead, I devote this review to two of the basic evolutionary concepts – convergence and signaling – that Prasad uses to inform his investment strategy. At the end I’ll say a few words in favor of laziness.

What is evolution and what does it have to do with economics and investing?

As background for convergence, signaling, and the other evolutionary ideas in Prasad’s book, let’s look at the many parallels between biological evolution and the operation of the economy – acknowledging that there are areas where the metaphor doesn’t apply.

I start with a precise definition of “evolution,” because the word is often used loosely just to mean change or improvement. That’s not its scientific meaning. In biology, evolution is a change in the genetic makeup of a population over time. More precisely, it’s a change in the relative frequency of alleles (gene variants) in that population, due to the joint effects of (1) random variation and (2) natural selection – the latter sometimes called “survival of the fittest,” a vivid but imprecise phrase I expand on below.3 (An allele is “one of two or more alternative forms of a gene that arise by mutation and are found at the same place on a chromosome” – that is, it is not just any variation in a gene, but a specific kind.4)

If two subsets of a population change enough in their genetic makeup that they can no longer reproduce with each other, you get new species, as Darwin said in the quote above. Further evolution can cause, over very long periods of time, divergence so profound that the species look like they come from different planets. Eagles and crocodiles, both descended from archosaurs, are an example.5

The operating instructions of evolution

To see how evolutionary concepts can be repurposed as business management ideas, let’s review the basic “operating instructions” of evolution:

- Competition (Darwin’s “struggle for existence” – not everyone survives long enough to reproduce);

- Mistakes (most variations are useless or harmful);

- Speciation (some new variants of organisms succeed and, over time, become new species);

- Convergence (very different species, faced with similar problems, come to resemble each other);

- Differential reproduction rates, consisting of (1) the probability of surviving to reproductive age, and (2) the number of offspring you produce if you do reach that age; and

- Natural selection, or “survival of the fittest.”

I earlier described this last principle as imprecise. Sure, only the fittest survive – but fittest for what? If it only means the fittest for survival, the phrase is tautological and meaningless. Herbert Spencer, and then Darwin who loved and adopted the phrase, meant survival of those variations that were “fittest” for (that is, best adapted to) the immediate, local environment. But, at least initially, Spencer and Darwin did not quite finish the thought. All organisms are well enough adapted to their immediate environment that they thrive there, so “survival of the fittest” is better understood as fitness for surviving possible future change.6 Are you beginning to see the business analogy?

By recasting natural selection as survival of the fittest, Spencer should be credited, even more than Darwin, with pulling economics and evolution together. He described one aspect of evolution as “opportunistic expansion into empty ecological niches [along with] ...extinction... [that] happened due to large shifts in the...environment.”7 This description fits the story of business expansion, competition, and demise perfectly.

To round out the list of operating instructions, note that all organisms – not just intelligent ones – try, as hard as they can, to influence their environment to their own advantage. The outcome of these many processes is profound change over long periods of time.

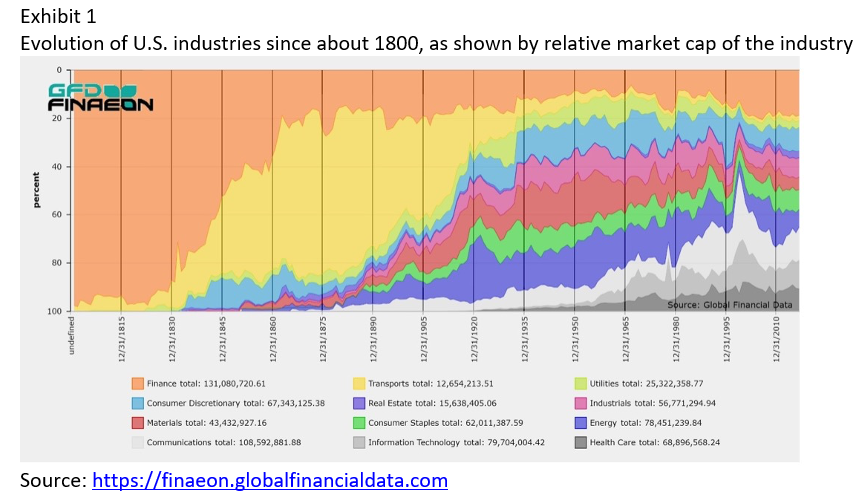

This is what happens in the economy and markets too. See the self-explanatory Exhibit 1.

Of the two concepts I cover, signaling applies more directly to business and investing, but convergence is a more profound and universal idea. So, I begin with convergence.

Convergence: On fish, dolphins, and ichthyosaurs

Why do fish, dolphins, and ichthyosaurs (an aquatic dinosaur) look so similar, despite having radically different ancestry? Why do birds, bats, and pterosaurs (a flying dinosaur) all sprout wings where their forearms “belong”? The reason is called convergence, the tendency of disparate organisms facing the same problem to come up with similar solutions.8 If you want to swim fast, the streamlined, finned design of fish and dolphins is just about the only design that will work. (That is why submarines also look like fish and dolphins.) Darwin understood this. He wrote,

Animals, belonging to two most distinct lines of descent, may readily become adapted to similar conditions, and thus assume a close external resemblance.9

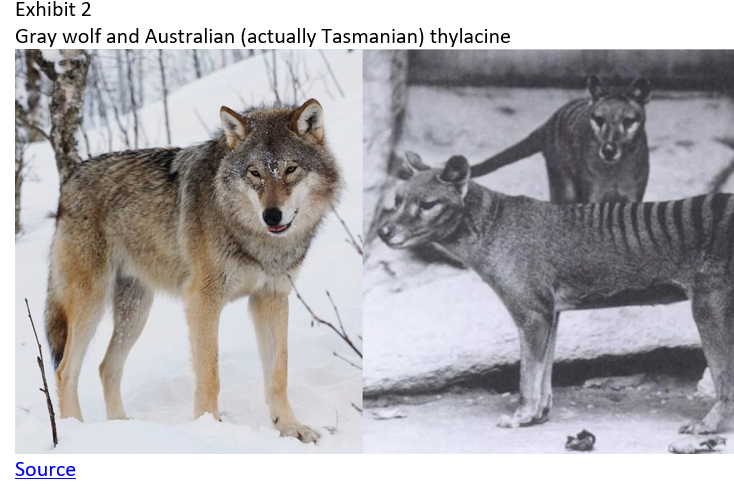

A particularly vivid illustration of convergent evolution is the similarity between Australian marsupials and non-Australian placental mammals. Each marsupial seems to have a placental counterpart that looks and functions similarly but comes from a different bloodline. Exhibit 2 shows an example.

Australia and Asia separated, due to continental drift, about 100 million years ago when no mammal of modern design existed. The thylacine, sadly now extinct, and the wolf have no common ancestor that looks anything like them. The two carnivores came to look alike over millions of years because they faced similar challenges in adapting to their respective niches – the need to catch fast-moving prey, to chew and digest it, to stay warm in a cold climate, and so forth. In fact, the “dog design” and the “cat design” are the only surviving carnivore designs because they seem to be the only ones that work, all of nature’s other experiments in carnivory having gone extinct.10

This apparent pairing of an Australian marsupial and a Eurasian/North American placental mammal, physically similar but genetically almost unrelated, is repeated many times across different creature designs. This shows that convergence is not just an oddity applying to wolves and thylacines, but a recurring theme in evolution. The reason is that there are typically only a few ways – sometimes only one way – to solve a problem, as we saw with fish, dolphins, and submarines.

Convergence investing

Now, what does all this evolutionary biology have to do with stock picking?

Although Prasad buys companies like any other stock picker, he thinks of himself as buying industries because all the companies in the industry compete in the same ecosystem and face similar problems. As a result, their profits tend to cluster around the industry median. That’s the business analogue of convergence in biology. (I’m oversimplifying for brevity’s sake.) Some industries, often the most boring ones, offer large profit margins almost as a matter of course: “sanitaryware” (toilets) and job bulletin boards are his examples. Others, typically glamour industries, offer low ones: airlines, the quintessential glamour stocks of the last century, have earned a cumulative loss over their entire existence!

But Prasad identifies exceptions to the boring (value) versus glamour (growth) rule, for example information-technology outsourcing companies, which typically earn huge returns on investment. Competition among these semi-glamorous companies doesn’t seem to drive down profits as one might expect. You have to look at industry data and macroeconomic conditions (the ecosystem beyond the industry), not just judge an industry based on its superficial appearance.

Prasad sums up his convergence philosophy by noting that, like animals or plants trying to solve a problem and converging on similar solutions, “there are only a few ways for a business to succeed.” His advice is to “identify...a convergent pattern of success or failure” in businesses and, of course, buying the likely-to-be-successful ones.

This is easier said than done. And Prasad admits that the rule works except when it doesn’t.

Assessing convergence-based investment strategies

If these homilies are what Prasad got out of Darwin’s writings on convergence, they’re not wrong – they’re just a bit anticlimactic. It’s true that the industry factor explains a large proportion of a given stock’s return. But company strategies and decisions matter. Investors in Ford Motor Company and Packard Motor Company had profoundly different experiences. A priori it was not obvious that they would; they were in the same highly profitable industry, made high-quality products, and differed mostly in size and strategy. Ford’s large size and diversification were advantages, but so is specialization (Packard made luxury touring cars, a strategy that worked well for Daimler-Benz!). Packard went out of business because it made a major strategic mistake. It tried to compete with Ford and GM by expanding into markets for which it had no talent.11 Prasad’s method might have missed this difference.

Prasad admits that his formula does not always work and gives Amazon, which he didn’t buy, as an example. He avoided it because it started out in a glamour industry (e-commerce) – and he expects to miss the next Amazon too. But he says that the opportunity cost of missing an Amazon is offset by the consistent profits from buying “high-quality companies at a fair price” and being “very lazy.” I’ll return to laziness later (because I’m lazy).

More recently, the computer industry has provided huge returns to investors. Yet, while Apple and Microsoft have grown to be trillion-dollar corporations – there are only five in the world12 – many computer companies have failed or deeply disappointed, including former greats such as Digital Equipment, Compaq, and the technologically superb Cray Research.13 Although the business ecosystem has rewarded innovation in computers beyond imagining, it was possible to lose money by choosing stocks poorly. The evolutionary approach to investing, or more properly this evolutionary approach, has its limits.

But one can imagine many other investment disciplines grounded in biology and evolution, because the basic principle is sound and provides a pathway for thinking differently about investments, surely the key to beating the market or a benchmark.

Signaling

Even closer to the essence of business strategy than convergence is signaling, an element of game theory.14 Game theory, in economics, asks how one should behave when the results depend on how others behave. This idea applies in business because companies maximize their profits in the face of competition from other companies that are trying just as hard and employ people who are just as smart. Most businesspeople know they are playing this game, so applying formal game theory to business is not a stretch.

Evolutionary game theory asks the same question about species that thrive if the individuals maximize the number of their descendants.15 The evolutionary version was developed by scientists who were familiar with economic game theory and intuited – correctly, it turned out – that it would apply even more directly to biology than to economics.

Central to evolutionary game theory, and to security analysis, is signaling. Prasad writes,

Signals have evolved specifically to alter the behavior of the receiver in ways that benefit the signaler and are [intended to] influence the behavior of prey, predators, mates, competitors, friends, and family. While we call ourselves investors, an evolutionary biologist would not be remiss in branding us as “signal decoders.” As outsiders to a company, the only thing we rely on is signals being emitted by companies – some direct and others indirect; some comprehensible and others bizarre; and most important, some honest and others dishonest.16

According to evolutionary theory, signals are likely to be honest only when they involve some sort of sacrifice or cost borne by the signaler. According to Prasad,

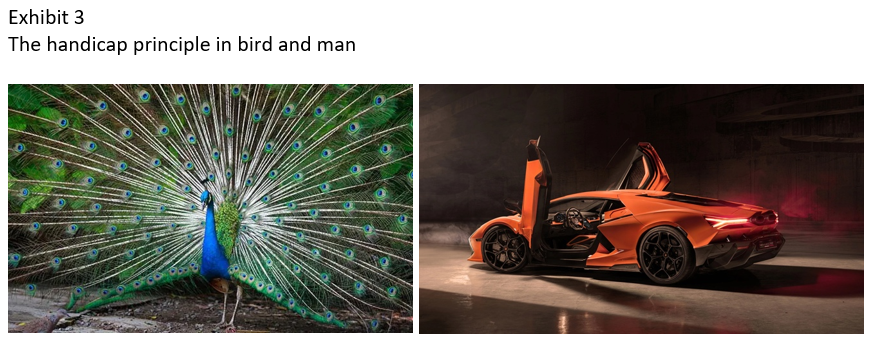

In 1975, Amotz Zahavi, an Israeli evolutionary biologist, proposed his famous handicap principle which asserts that only those signals that are costly to produce (and hence are handicaps) can be considered reliable. For example, male elks with larger antlers attract more mates presumably because their message to female elks is: look how healthy and virile I am because I carry these massive unwieldy antlers.

It’s possible that big antlers help their bearers fight or scare off rivals, but the peacock’s magnificent tail has no known function other than to show females that the male has so much vigor he can afford to waste it on a very expensive (in metabolic terms) decoration.

The behavior of rich human males is similar. Rather than or in addition to advertising one’s athletic ability – a more direct way of demonstrating fitness – they may buy fast cars, big boats, and lavish homes, again demonstrating the ability to expend resources frivolously. The Lambo is the human “peacock’s tail.”

Nature, I guess, has a sense of humor – it selects for individuals who conspicuously waste resources over those who more subtly demonstrate that they have plenty of them.

Signaling in business

Applying the handicap principle to stock picking, investors should avoid companies that waste resources on dishonest signaling and buy those that send honest signals. Analysts should therefore ignore signals that are costless (or nearly so) to the signaler. Prasad’s examples of worthless signals include press releases, interviews, investor conferences, road shows, and earnings projections. There are no consequences for being wrong, no “skin in the game.”17

In contrast, worthwhile signals, which are costly to the company, include past financial performance and the company’s achieved competitive position in the industry. These demonstrate a history of having produced a high return on capital. Not only can such a company do something right, it has done so, repeatedly so as to produce the observed results.

Prasad thus invests in companies that display these characteristics. His investment management firm has done well, partly because it operates in the emerging Indian market where price is often quite distant from value. Signal-based investing is not, however, a fail-safe formula for success (nothing is). IBM Corporation did a great many things right, dominating its industry for decades, before it faltered in the 1990s.18 The same can be said of many other once-great companies, so beware of taking Prasad’s signaling advice too literally.

“Don’t be lazy – be very lazy”

If there’s one lesson in Prasad’s book that is hard to argue with, it’s that lazy investors tend to be winners. Buy – hold – forget is a good general strategy, as long as your memory returns when it’s time to rebalance. Buying only index funds is even lazier (and usually more financially rewarding).

But Prasad means something else by “lazy.” He notes that a company’s long-term fortunes vary less than its short-term ones. Earnings surprises are mostly noise. So are stock price fluctuations, he argues. “News” is noisier than either.

He cites as an example L’Oréal, which meets his “buy” criteria by doing one thing well for a long time and making large profits. He then lists 65 (count ‘em!) news stories about L’Oréal that surfaced between 2009 and 2021, ranging in tone from slightly bad to very bad. He then pointedly asks, “Would you have stayed invested?” Most readers would say “no.”

L’Oréal’s stock price, quoted in dollars, rose from $18.15 on January 2, 2009 to $95.42 on December 31, 2021. It also paid a total of $7.63 in dividends over the period, plus some extra from reinvesting the dividends in the rapidly appreciating stock.19

Be lazy – but not crazy. Buy-and-hold almost always beats frequent trading, and always beats noise trading (trading not based on information). But, as I noted earlier, some companies do everything right until they don’t, or until a competitor wipes the floor with them.

Conclusion and advice to investors

I had fun reading What I Learned About Investing from Darwin. But I learned more about biology, a field in which I’m already somewhat well-read, than about investing. Many investors who are avid readers will come to the same conclusion. The classics of investment literature – Burton Malkiel’s A Random Walk Down Wall Street, Charles Kindleberger’s Manias, Panics, and Crashes, Peter Bernstein’s Against the Gods, and Nassim Taleb’s Fooled by Randomness, to name my favorites – are the finance liberal-arts education every serious investor needs.20 Prasad’s Darwin book is an elective course, likely to enrich readers’ understanding of the investment thought process but not revolutionize it.

Prasad makes a valiant effort at applying evolutionary theory at the granular level needed to inform investment decisions. Mostly he succeeds – and the book is a pleasant, lively read. But investors should not overapply the lessons of evolution any more than they should ignore them. Read this book; then, think for yourself and apply many disciplines, not just that of evolutionary biology, to the selection of securities.

Laurence B. Siegel is the Gary P. Brinson Director of Research at the CFA Institute Research Foundation, economist and futurist at Vintage Quants LLC, a speaker and independent consultant, and the author of Fewer, Richer, Greener: Prospects for Humanity in an Age of Abundance and Unknown Knowns: On Economics, Investing, Progress, and Folly. His website is http://www.larrysiegel.org. He may be reached at [email protected].

1 Siegel, Laurence B. 1982. Foreword to Roger Ibbotson and Rex Sinquefield, Stocks, Bonds, Bills, and Inflation: The Past and the Future. Charlottesville, VA: CFA Institute Research Foundation.

2 The Origin of Species, p. 7 (1859 [1909, Harvard Classics edition, in the introduction]).

3 A third mechanism, called genetic drift, has recently been discovered but it is not relevant to investing. A good explanation is at https://en.wikipedia.org/wiki/Genetic_drift as it was accessed on June 14, 2023.

4 The quote is from Oxford Languages.

5 Over even longer periods, plants and animals have a common ancestor, as do all living things on earth (including single-celled organisms). We know this from analysis of the DNA in their cell nuclei. This is one of the most astonishing findings of evolutionary theory.

6 And it is not clear in advance what the change will be. So, a genetic variation in an organism can be well adapted to one possible future outcome (say, warming of the climate) but poorly adapted to another (say, an increase in the population of predators). Depending on what actually happens, the organism will either thrive or go extinct. Evolution is powerfully influenced by randomness.

7 Principles of Biology (1864) – this is astonishingly modern talk for 1864! Spencer is blamed, fairly or not, for the dog-eat-dog philosophy called Social Darwinism, which basically says that you get what you deserve. Yet one of today’s most popular scientific themes, evolutionary psychology as popularized by E. O. Wilson and Steven Pinker, owes much to Spencer, who has been partly rehabilitated. A worthwhile discussion is at https://www.smithsonianmag.com/science-nature/herbert-spencer-survival-of-the-fittest-180974756/.

8 Some of my writing, like much evolutionary writing, makes it sound as though evolution has a mind of its own. It does not. Neither do species that “do” thus-and-such to adapt to their environment, or to become better adapted to possible future environments. It’s just a figure of speech. So is “design,” which implies that there is a designer when there isn’t.

9 Darwin, Charles. 1859. The Origin of Species. John Murray, London, UK, p. 427.

10 Except for the thylacine! And, remarkably, the thylacine looks like a cross between a dog and a cat – so much so that it is sometimes called the Tasmanian wolf and at other times the Tasmanian tiger. The evolutionary pressures faced by its ancestors pushed it toward both the (unrelated) dog design and the (unrelated) cat design, winding up somewhere in the middle. A richly detailed discussion of the evolution of carnivores is at https://en.wikipedia.org/wiki/Carnivora.

11 https://www.hagerty.com/media/car-profiles/10-reasons-why-packard-died/.

12 The others, as of this writing, are Amazon, Alphabet (Google), and Nvidia.

13 Larry Smarr, a distinguished computer scientist, called Seymour Cray “the Thomas Edison of the supercomputing industry.” https://www.washingtonpost.com/archive/politics/1996/09/24/computer-pioneer-injured/d173707b-7dc2-4fec-84c6-dfb13a86c7b7/.

14 Game theory in economics was developed by John von Neumann and Oskar Morgenstern (The Theory of Games and Economic Behavior, 1944) and John Nash (the subject of Sylvia Nasar’s 1998 biography A Beautiful Mind, made into an Academy Award-winning movie in 2001). Nash’s concept of game-theoretic equilibrium is described at https://en.wikipedia.org/wiki/Nash_equilibrium (caution, this article is quite detailed and advanced).

15 See https://plato.stanford.edu/entries/game-evolutionary/ for a description, again quite advanced. The seminal work in the field is Maynard Smith, John. 1982. Evolution and the Theory of Games. Cambridge, UK: Cambridge University Press.

16 In CEO World, at https://ceoworld.biz/2023/04/07/what-i-learned-about-investing-from-darwin/.

17 Earnings projections are Prasad’s bugaboo, not mine. Companies that miss their earnings estimates are often punished harshly in the market, indicating that they do have skin in the game. (Maybe this isn’t true in India – I have no idea.)

18 A thoughtful analysis is at https://manavsplace.medium.com/marketing-why-ibm-faltered-2b328b2a66e2.

19 These are actually quotes for the L’Oréal ADR (American Depositary Receipt), traded on the NASDAQ as LRLCY.

20 I leave out Benjamin Graham and David Dodd’s Security Analysis at my peril – it is the foundation of the modern practice of active management – but most advisors and their clients are not about to become security analysts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All