Are Fixed Indexed Annuities More Efficient Than Bonds?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits A recent paper by retirement researcher, Wade Pfau, had two fascinating conclusions.

A recent paper by retirement researcher, Wade Pfau, had two fascinating conclusions.

- In accumulation mode, a portfolio comprised of stocks, fixed-indexed annuities (FIAs), and (sometimes) bonds offered a more efficient risk-return tradeoff than stocks and bonds alone.

- In withdrawal mode, stocks and FIAs offered a far greater withdrawal rate than a portfolio constrained by stocks and bonds alone. Bonds had no role.

The paper entitled “Protection as an Asset Class” was published by the Alliance For Lifetime Income, a non-profit 501©(6) educational organization based in Washington, D.C. I’ve known Pfau for many years and have the utmost respect for him. I’m always looking for safer strategies for accumulation and, especially, decumulation. I investigated this research and interviewed Pfau. My concentration was on the use of FIAs in portfolios rather than whether they were a separate asset class from stocks or bonds.

FIAs in accumulation

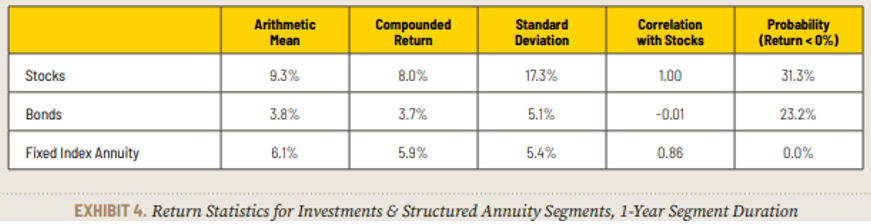

An FIA is a contract between the annuitant and an insurance company where the return is based on the performance of a chosen stock market index or indexes. With FIAs, the principal is guaranteed. In the paper, Pfau uses an FIA linked to the S&P 500 price index (excluding dividends, which he discloses) with a cap rate of 12%. With these terms, the FIA will earn between 0% and 12% each year. It will not have a loss which, as Pfau points out, both stocks and bonds had in 2022. He told me these terms were similar to many FIAs but not based on any specific product.

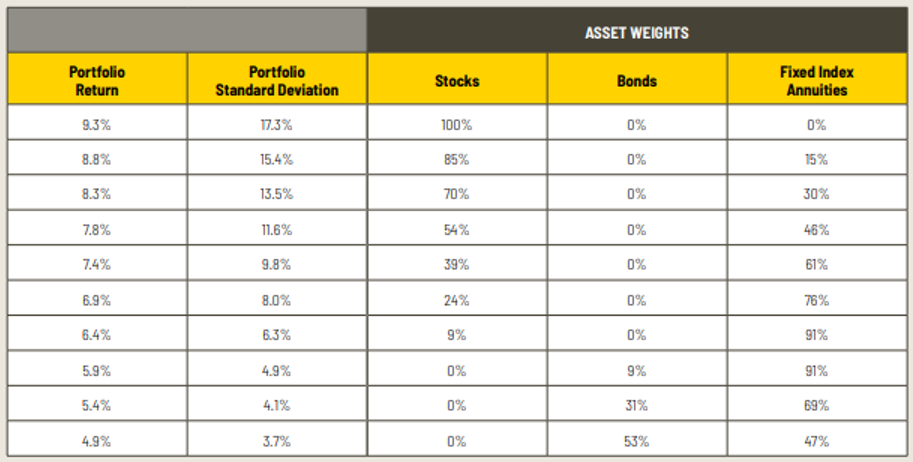

Using the efficient-frontier framework, Pfau calculated the optimum portfolios from a risk-return perspective. Bonds had a place only in portfolios with no stocks. Had bonds ben included, a lower risk-adjusted return would result, which would not be on the efficient frontier.

Pfau’s assumptions were as follows:

For stocks and bonds, the return assumptions came from BlackRock’s long-term (30-year) capital market expectations. The compounded return is the geometric mean; the larger the standard deviation, the more the geometric mean will lag the arithmetic mean. For stocks, Pfau used U.S. large-cap and, for bonds, the Bloomberg US Aggregate bond index.

The FIA has a significantly higher return than bonds for both the arithmetic and geometric returns. That’s driving the use of FIAs rather than bonds. I take no issue with assumptions on either stocks or FIAs (with the existing terms) but do on bonds.

The 3.8% arithmetic mean is 0.6% below the 10-year Treasury yield of 4.4%. Economists have a horrible track record of predicting intermediate-term rates and the best predictor of forward intermediate-term rates turns out to be the current rate. Second, the Bloomberg AGG is about 67% backed by the U.S. government or government agencies. While an FIA has some backing by individual states, those states would have to fund the losses from other insurance companies; that guarantee might be worthless in a systemic insurance crisis. FIAs are riskier than U.S. government bonds.

I told Pfau that a diversified investment-grade corporate bond fund might have a closer risk profile to one (or even three) FIAs with insurance companies. Pfau responded that this was a reasonable argument. As of the time of this writing, the Vanguard Intermediate-Term Investment-Grade Fund Admiral Shares VFIDX had a 5.3% yield with a standard deviation slightly higher than the AGG. That wiped out the vast majority of the FIAs advantage over comparable bonds.

Every FIA contract I’ve reviewed has the unilateral right of the insurance company to change the terms of the contract, such as lowering that 12% cap. Pfau agreed that insurance companies have that right. I asked Pfau how low those caps could go, and he responded, “As low as 1-2%.” I’ve seen 0.25%, meaning the contract owner would get between 0% and 0.25% annually. This right of the insurance company to slash returns was not mentioned in Pfau’s paper.

FIAs in withdrawal mode

In the second part of the paper, Pfau used a framework he called the efficient frontier for retirement income. He defined the efficient frontier in retirement as:

Meeting a lifestyle spending goal for as long as one lives, providing a legacy for the family or community, and maintaining liquidity to cover unexpected expenses and contingencies.

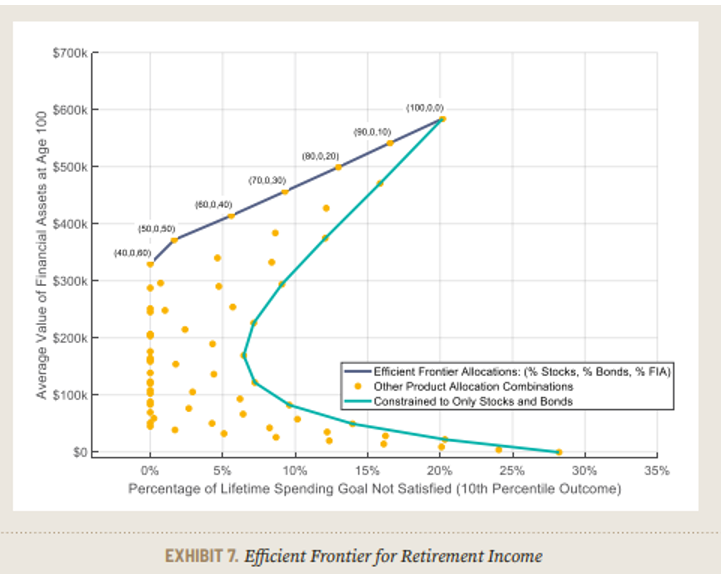

Pfau used the example of a 65-year-old woman wishing to spend 4% of her portfolio annually, increasing by 2% annually, for 35 years (age 100). Pfau looked at stocks, bonds, and FIAs with a guaranteed lifetime withdrawal benefit (GLWB). A GLWB is an optional lifetime income protection that does not require annuitizing the contract. Using $100,000 as the starting amount of investible assets and a 4% spend rate (increasing 2% annually), Pfau produced the following efficient frontier.

Pfau concluded, “Bonds are not on the efficient frontier. They do not serve a useful role for meeting spending goals in the optimal retirement income portfolio.”

I spoke to Pfau at length about this chart. A portfolio of 60% FIA and 40% stocks survived the 4% spending goal in at least 90% of the Monte Carlo simulations. A portfolio constrained to stock and bonds with, say, a 15% pending goal not satisfied means that, at the same bottom 10% of scenarios runs out on average 5.25 years (15% x 35 years) before turning age 100.

For this scenario, the risk that the insurance company could unilaterally cap the return is essentially eliminated. That’s because the GLWB payments combined with the 1.1% annual fee for the rider means that the underlying annuity value will likely eventually reach zero over long periods of time, according to Pfau. But the GWLB will keep paying 5.5% for life. In this example, where there is no shortfall in the lifetime spending goal, the retiree with $100,000 puts $60,000 in the FIA to get $3,300 a year for life. Thus only $700 needs to be taken out from the $40,000 in stocks the first year, which is only 1.75% of that stock portfolio.

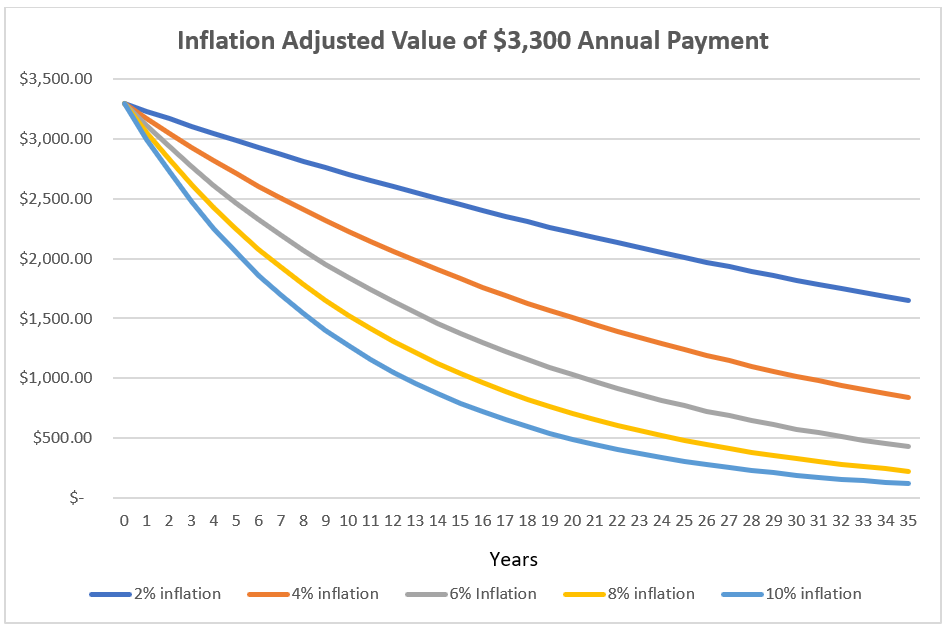

While using the assumptions for an investment-grade bond portfolio would mostly close the gap between the bond and stock constrained portfolio, I suspect the FIA would only prevail under the assumptions of low inflation. Pfau stated he increased her spend rate by 2% annually to “help cover inflation for retirement expenses.” But inflation has averaged nearly 3.8% since 1960. At 4% annual inflation, in year 35, this $3,300 annual payment buys only $836 of goods and services and, at 10%, only $117. In other words, this strategy would lead to more than a shortfall; it would be a catastrophic failure.

I ran this by William Bernstein, an author, financial historian, and co-founder of Efficient Frontier Advisors. He discussed inflation in his revised edition of The Four Pillar’s of Investing . Bernstein called this strategy “Russian roulette with inflation.” Bernstein noted that the odds of catastrophe with Russian roulette, one in six, are in the same ballpark as the odds of catastrophe with inflation. Bernstein said, “From economic history, inflation is pervasive and common, and our country is slowly approaching the point of debt spiral. Counter to that is the Fed's reputation for inflation fighting.” Bernstein said the retiree should be worried about inflation in excess of 3% annually.

Pfau’s response to my concern with inflation was that a bond portfolio would also take a hit from rising rates. I pointed out that the duration of the annuity was much longer than the bond portfolio and thus more exposed to inflation. He correctly noted that some of the bond portfolio would have already been spent before the underlying bonds matured but did admit the annuity was far more exposed. He also agreed that using TIPS as part of the bond portfolio would mitigate inflation risk. As of the time of this writing, TIPS were yielding over 1.8% plus inflation and any portion of a portfolio in a TIPS ladder can provide a real (inflation-adjusted) and virtually 100% safe spend rate of over 4% for 30 years.

Conclusion

I applaud Pfau for his professionalism in answering some very difficult questions. Pfau said that he was paid a monthly stipend from The Alliance For Lifetime Income, which published the paper. Further, he directed me to the list of member organizations, comprised in large part of insurance companies or companies which would profit from the sales of annuities.

I do, however, disagree with some of his key assumptions and omission of critical risks such as the insurance company lowering the annual return cap, the risk that insurance companies could fail, or that inflation is a predictable factor. Average historic inflation would produce a very different result, while high inflation would lead to the GLWB being close to worthless in real terms. While the FIA with the GLWB provides longevity protection, it takes on an extreme amount of inflation risk.

When adjusting for more realistic assumptions and considering the fact that the insurance company can change return caps and that inflation is both an unknown and deep risk, an FIA, along with most annuities, is not on the efficient frontier in either accumulation or decumulation phases.

In fact, the high fees of annuities are, by definition, inefficient.

Fees must be low and diversification high to be on the efficient frontier. A combination of diversified stock and bond portfolios is on the efficient frontier. A TIPS ladder as part of the bond portfolio mitigates some of the deep risk of inflation. Delaying Social Security is generally on the efficient frontier for retirement income, since it provides both inflation and longevity protection with no fees. Both Pfau and I agree on that point. He told me, “The implied payout rate on delaying Social Security is much higher than any commercial annuity.”

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All