Bankers are warning that tougher capital rules being proposed by the Federal Reserve and other US regulators will push more risks out of well-regulated lenders and into markets. “This is great news for hedge funds, private equity, private credit … they’re dancing in the streets,” Jamie Dimon said on JPMorgan Chase & Co.’s earnings call last month even before the entire proposal was unveiled.

The chief executive officer of the biggest US bank has since called the plans “hugely disappointing,” saying they will likely increase costs and restrict supplies of some mortgages and small business lending — from banks at least.

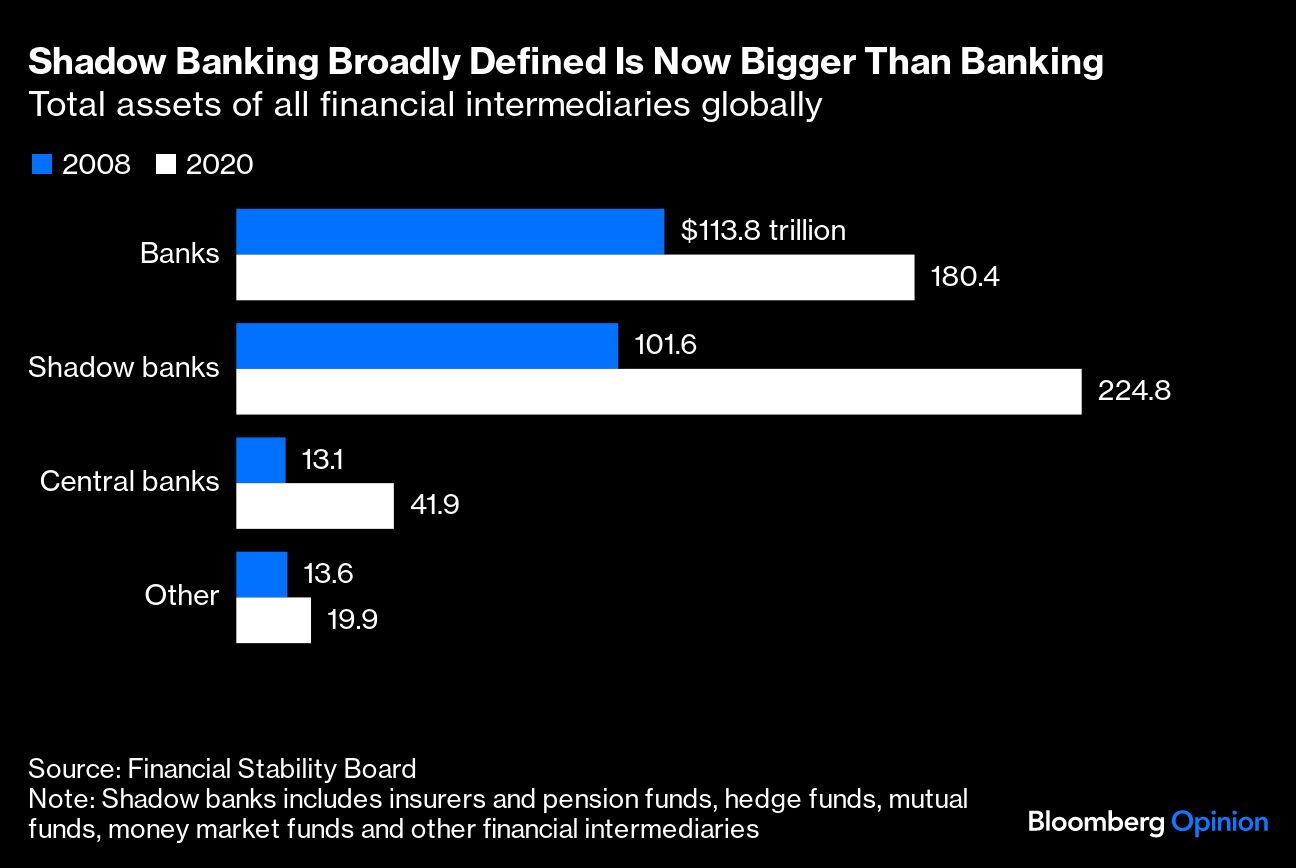

The evolution of capital rules since the 2008 financial crisis has been focused on making the banking system stronger, safer and less likely to need bailouts. The supply of credit from financial markets instead has ballooned partly as a consequence of this. But pushing risk from banks into what’s often called shadow banks hasn’t necessarily made the system as a whole safer, nor has it reduced the Fed’s role in lending support when times get tough.

In fact, the Fed formalized its job as the lender of last resort to the shadow banking system – or what could be called dealer of last resort – after seeing the problems that emerged during the dash for cash at the start of the Covid-19 pandemic and when money markets seized up in September 2019.

This is, I think, an underappreciated shift in the Fed’s relationship to market finance. It’s easy to underestimate because the changes were mostly couched in terms of ensuring monetary-policy effectiveness and were related to collateralized lending and borrowing windows known as Standing Repo and Reverse Repo Facilities. But these changes have given primary dealers, which handle government debt trading, and money-market funds access — either directly or through dealers — to the sort of central bank deposit and borrowing facilities that traditional banks have always had in modern finance.

The monetary policy part of this is twofold. When there is too much cash sloshing around the system, money funds can hand it to the central bank through the reverse repo facility rather than chasing short-term bills and pushing yields down too far below the Fed’s target rate. Right now, they have nearly $2 trillion parked at the central bank this way.

On the flip side, when dealers or money funds suddenly need cash, instead of rushing to sell Treasuries or bills and thereby pushing market interest rates too high, dealers can borrow directly from the Fed through the permanent standing repo facility, which was opened in the summer 2021.

But this isn’t just about monetary policy, especially the standing repo part. It’s also about preventing a rapid contraction of credit in the economy. What central bankers and regulators realized in 2008 and reinforced for them even more in 2020 is that the shadow banking system can suffer chaotic and destructive runs just like traditional banks. When that happens it has nasty ripple effects.

In both these crises, the Fed had to step in and offer repo financing to dealers and others as a temporary measure – alongside its many other support programs. But after 2020, it decided this repo facility was so crucial to the healthy functioning of finance that it should be made permanent. Lorie Logan, now president of the Dallas Fed but previously in charge of liquidity operations at the New York Fed, laid out the mechanics of a shadow banking run that the standing facility should help to mitigate in an August 2021 speech. A sudden heightened demand for dollars revealed vulnerabilities in short-term funding and money-market funds, which in turn threatened the flow of credit.

When this happens with traditional lenders, it all unfolds within a bank’s balance sheet. The balance sheets of shadow banks are spread over different kinds of institutions. The core of shadow banking has very short-term deposit-like liabilities, often held by money funds, at one end; and through a chain of transactions in repo markets with dealer banks and risk-hungry investors like hedge funds at the other end, these liabilities are transformed into riskier, longer-term capital markets lending.

When the money-market funds and other big companies and fund managers with vast pots of cash suddenly want that money back, it leads to exactly the same kind of unraveling as a bank run.

Part of the reason shadow banking grew so large, according to the money-market specialist and former Credit Suisse Group AG analyst Zoltan Pozsar, is that companies and foreign central banks with large amounts of dollars couldn’t safely keep their cash in banks: Deposit insurance only stretches to $250,000, and there aren’t enough big, safe banks to spread it around. Some economists go as far as saying that repo liabilities and even money-market fund shares are essentially money in the same way that bank deposits are money. There is a big difference in that you can’t use a repo liability to buy your groceries, but many other characteristics support this idea.

The bottom line is that shadow banking has grown increasingly important and similar to traditional banking. And while banks have been made sturdier through tougher regulation, the biggest is still deeply entangled with shadow banks through their own dealer arms. The Fed is now the permanent backstop to both.

Credit risk might keep moving from banks to markets, but when the next crunch comes, the Fed will likely be just as involved as ever in keeping it flowing.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies