Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The turmoil in the banking system earlier this year caused private-debt issuers to make concessions, including floating rates and improved covenants, which make this an attractive asset class.

In March of this year, the financial banking system experienced a significant disruption with the collapse and bankruptcy of Silicon Valley Bank (SVB). At the time, SVB was the 16th largest financial institution in the United States, often the preferred bank for early-stage and venture capital-backed companies. Poor treasury management and dramatic outflows of deposits led the bank to declare insolvency. Other financial institutions with a similar customer base, including Signature Bank and First Republic Bank, saw a similar demise.

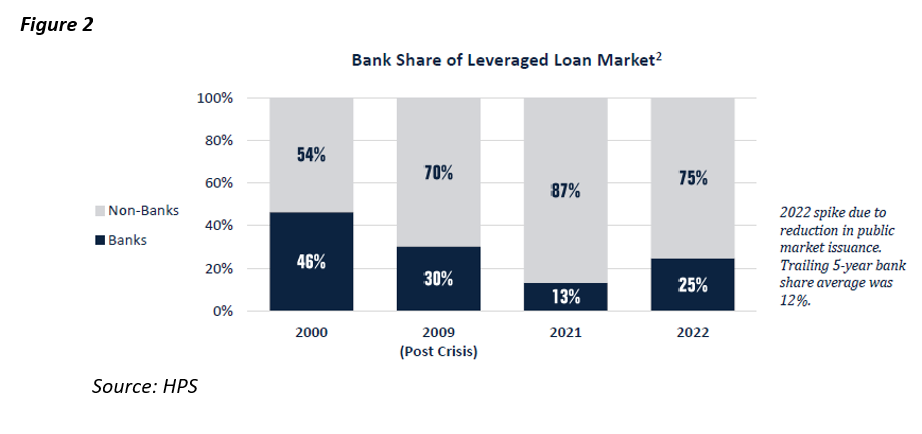

Fortunately, the Federal Deposit Insurance Corporation (FDIC) promised to make whole all customers of SVB, even those with assets above the insured deposits maximum of $250k. That step helped avoid a greater financial crisis, but there was a broader impact that changed the lending environment. The appetite for financial institutions to provide credit diminished due to concerns of policy tightening, higher interest rates, and recessionary fears. With companies in search of financing, the private-debt market has become an appealing option, as banks are reluctant to offer competitive quotes to borrowers. Private lenders are willing to provide the necessary capital but structure their loans so that they reside higher in the capital structure (they are first to be paid back in the event of a default) and are floating rate (a hedge against rising inflation). Overall, private debt has become an attractive opportunity, and investors can benefit from both higher yields and greater downside protection.

Advantages of private debt

The landscape for private debt has changed. Companies are utilizing the private markets more frequently for their borrowing. Investors in the asset class can benefit in the following ways:

- Attractive yields

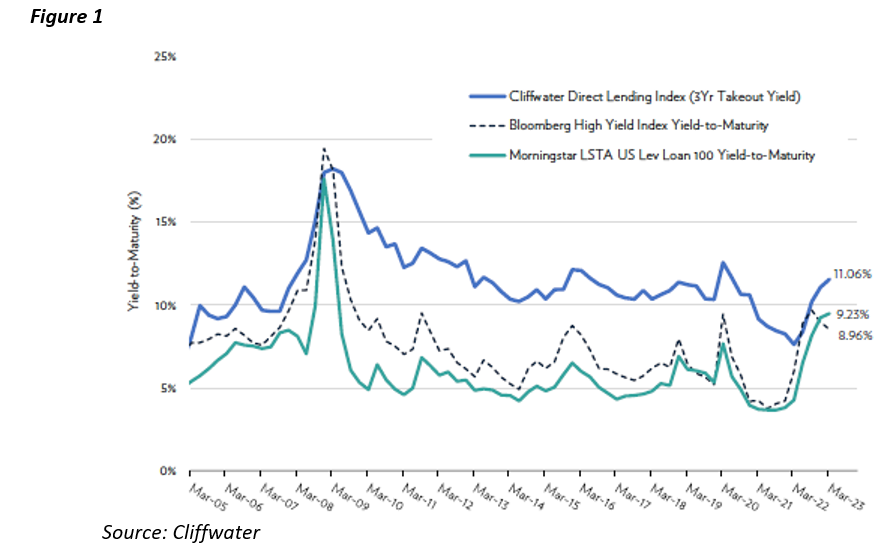

Private debt offers a return premium relative to leveraged loans and high yield bonds. Though the asset class is illiquid, at the time of this writing private debt compensated investors with an 11.06% current yield (as measured by the Cliffwater Direct Lending Index) relative to 9.23% and 8.96% current yield for leveraged loans and high-yield fixed income, respectively.

- A hedge against rising inflation

A majority of private debt is issued as floating- or variable-rate securities. If inflation were to persist and interest rates were to rise, then the yield on private debt would adjust. For example, at the end of 2021 the private-debt market was yielding close to 8%. By 2022, as the Federal Reserve aggressively raised interest rates to slow inflation, the yield on private debt only increased. Now, the current yield is hovering around 11%.

- Senior secured

Private-debt offerings have constructed loans that are mainly senior secured and first lien, where the actual loan is backed by collateral such as a building, inventory, or accounts receivable. These terms allow the lender to have first claim against these assets if the borrower were to default on the loans. This option is less risky than more subordinated or mezzanine debt, where the loans are unsecured, only senior to equity in the capital structure, and demand a much higher interest rate.

- Better covenants

Over the last 15 years, during a more accommodative and lower interest rate environment, terms of private loans were more favorable to borrowers. Structures such as delayed-draw term loans (DDTLs), which permit borrowers to draw additional funds during the term of the loan, became more prevalent. Maintenance covenants, which provide lenders with early warning signs of potential issues, became weaker. But, in the current environment, where access to financing has diminished, lenders are demanding higher rates and improved terms. This has allowed private-debt investors to better oversee their underlying portfolio companies and take necessary corrective action as needed.

- Diversification and active management

Private-debt investment managers have been thoughtful in lending to firms in numerous sectors, including information technology, healthcare, industrials, consumer discretionary, and business services. The objective is to diversify their exposure where they can generate a strong yield while minimizing default risk due to an economic downturn.

The biggest area of concern in private debt is defaults. While private debt offers an attractive investment opportunity, the risk of default remains as one of the greater headwinds in the asset class. Longer term and legacy private-debt issuers face the concern of higher interest rates, which makes servicing debt more difficult, coupled with a slower economy and potential margin erosion. If the United States were to experience a severe recession, private-debt portfolios would be negatively impacted.

The bankruptcy of SVB and other financial institutions created a disruption in the lending market. Banks are more cautious about who they lend to, going forward, which has minimized access to financing for many companies across various sectors. Private-debt markets identified this issue and have been willing to provide the necessary capital for these firms to assist in their growth, restructuring, or other long-term objectives. These loans offer high yields, stronger covenants, inflation protection, diversification, and the additional provision of being senior secured. The recessionary risks of default are still prevalent, but the asset class potentially provides a more favorable risk-adjusted return, especially relative to public equities and fixed income. In an uncertain time in the markets and economy, private debt may better a portfolio by enhancing return while minimizing risk.

Sloan Smith, CAIA, MBA, CWPA®, is principal and director, and Cos Braswell, M.S., is lead senior analyst at Innovest Portfolio Solutions, LLC, a Denver-based investment consulting firm. More information on Innovest can be found at www.innovestinc.com.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more articles by Sloan Smith, Cos Braswell

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.