Offices in many of the world’s major cities are struggling to find workers to occupy them. The trend of remote working, triggered by the pandemic, is costing Manhattan “$12 billion a year,” “devastating America’s cities” and “killing London.”

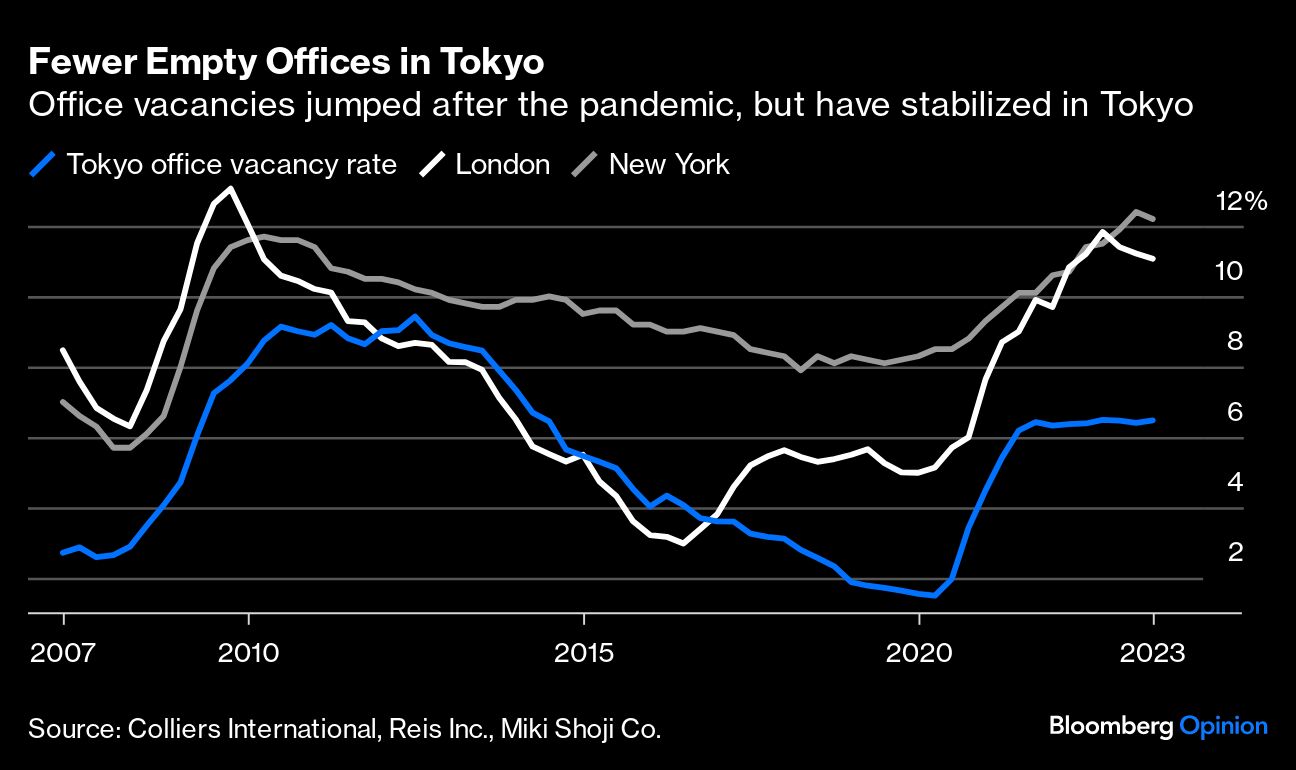

In the world’s biggest metropolis, however, not only are employees back, developers are doubling down on the office. In 2023, Tokyo will add some 1.26 million square meters (13 million square feet) of new office space, with little trouble occupying it. Vacancy rates hover around 6%, primarily in older stock. Foreign investors, some of whom are dumping properties overseas, are snapping up buildings.

It’s quite a contrast from a year ago. As the borders reopened last October, some wondered if a still-masked Tokyo might never return to pre-Covid normality. Almost 12 months on, though the city’s recovery from the pandemic has been more circuitous, it may be more complete than global peers.

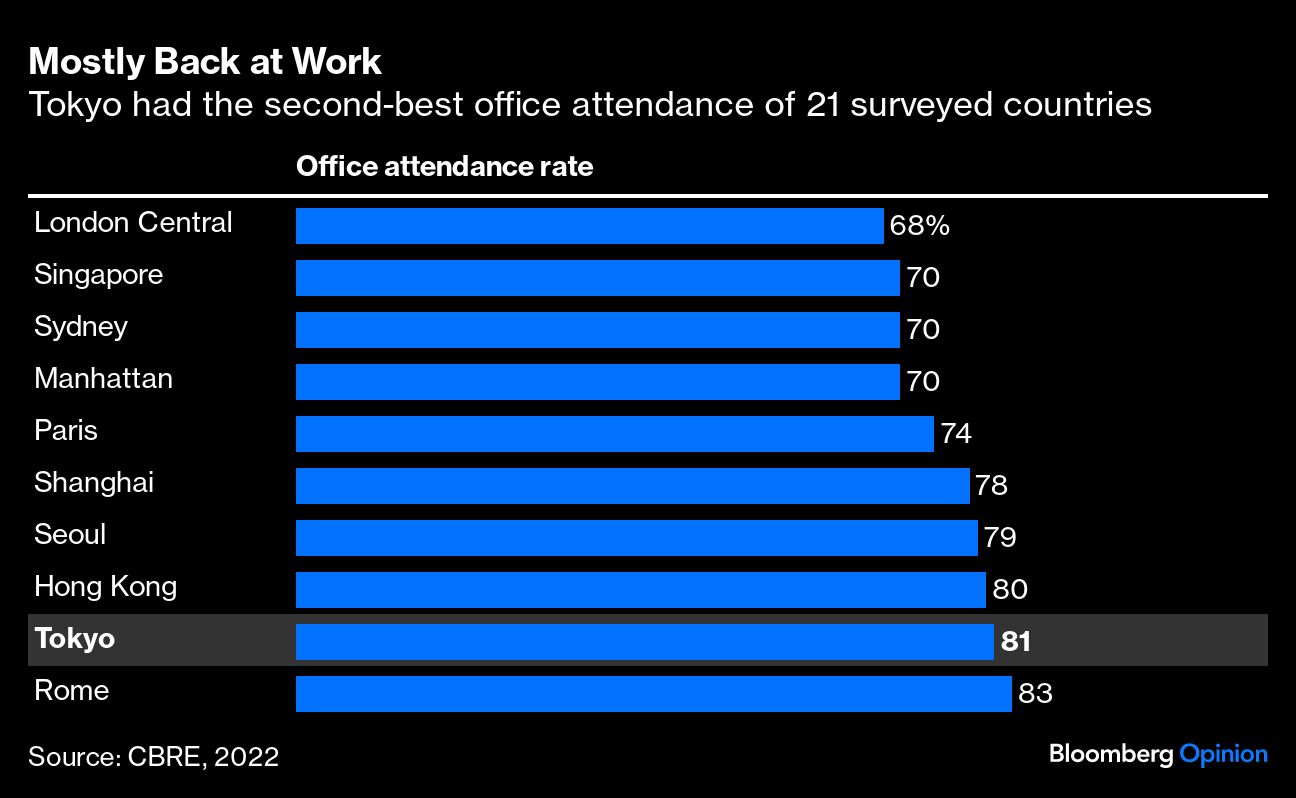

Workers are populating offices: Tokyoites have the second-highest attendance rate of 21 countries surveyed by CBRE Group Inc. The average number of people in the Otemachi business district, for example, is back to more than 90% of 2019 levels during office hours, Nikkei reports. This week, the Partnership for New York City, a business interest group, said just 58% of office workers in Manhattan have returned to the workplace, with that figure only expected to grow to 59% “on a long-term basis.”

Tokyo, of course, is far from the only Asian city that has bounced back from Covid’s onslaught. But a unique combination of factors are working in its favor. The Bank of Japan’s outlier status in keeping cash cheap is one; many foreign investors speak of the higher rental yields available thanks to the reduced cost of capital. Even if the central bank does get rid of yield-curve control or negative rates before the next global recession, it’s practically impossible to imagine a scenario where money becomes expensive in any meaningful way. Meanwhile, for international financiers — as well as digital nomads, who are headed to Japanese cities like never before — the weak yen has made everything 50% off.

Shopping is another reason. Adding to locals’ preference for in-person experiences rather than online, a growing wave of tourists who flock to the city to shop personally makes Tokyo the “city of choice for retailers,” CBRE says. The number of tourists staying in Tokyo was up 30% from 2019 levels in June. That’s good for the mixed-use retail and office facilities Tokyo specializes in.

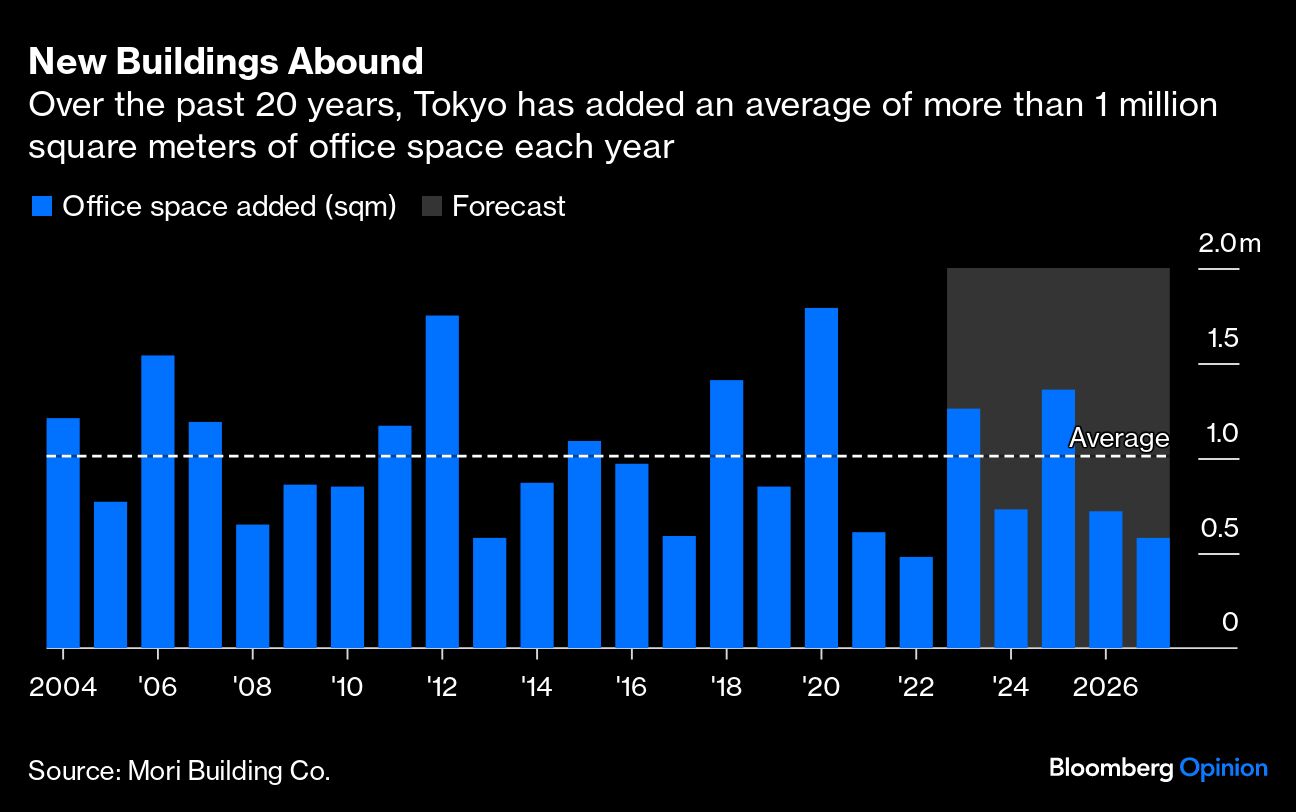

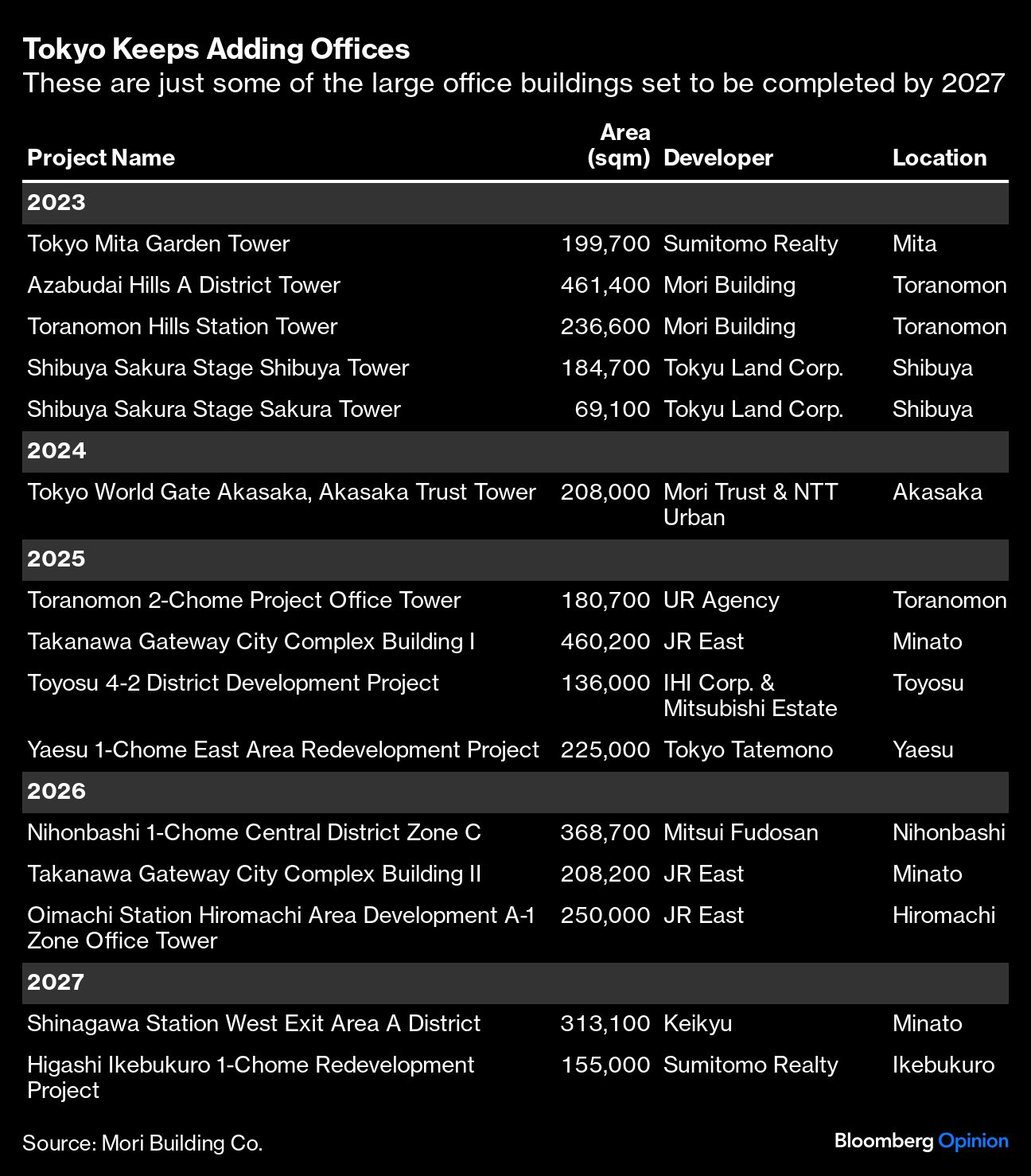

Meanwhile, the city has been building during the pandemic. Some 660,000 square meters will be added in Tokyo’s five central wards this year alone, according to Colliers International Group Inc. Much of that construction is in the Toranomon area, a once-humdrum business district that stretches from the bureaucracy’s seat of power in Kasumigaseki to Tokyo Tower, now in the middle of a remarkable transformation at the hands of Mori Building Co.

The latest in Mori’s multipurpose developments that fuse shopping, office space, apartments and hotels is the $4 billion Azabudai Hills project, set to fully open in November. On top of a hotel by Aman Group and a new campus for the British School, it will feature Japan’s tallest building, the 65-floor Azabudai Hills Mori JP Tower, which is Tokyo’s first supertall skyscraper1, adding about 214,500 square meters of office space and boutiques that include Hermes and Cartier.

It will join the nearby Toranomon Hills Station Tower, opening next month, while across town Tokyu Land Corp.’s Shibuya Sakura Stage will host the headquarters of firms such as Square Enix Holdings Co., as well as serviced apartments operated by Hyatt Hotels Corp., after the complex opens in November.

Total occupied floor space is actually up by 3% compared with pre-Covid days, CBRE says. Is this something employers in the West can replicate? Partly, though, the factors are unique: Scars from the pandemic run far less deep here. No government-imposed lockdowns throughout the period meant remote work didn’t become as entrenched. Worker presenteeism undoubtedly still exists, even if its intensity has dropped significantly than a few decades ago, while Japan’s relatively cramped apartments haven’t made working from home a more attractive option. And the services sector simply comprises a smaller segment of the economy than in the US or UK.

But the recovery is also unquestionably buoyed by the city’s enviable public transport network: Developers wouldn’t dream of opening those new buildings in Toranomon were it not for how they link with both newly built and existing train stations to ferry workers. One other simple policy is the standard commuter’s allowance: Most companies pay workers for their mass transit commutes. That might make it a little more difficult to stay at home.

The decline in the city’s nightlife persists, however: Although employees might be back to 90% normal in Otemachi during office hours, after work they drop off to just 70% of pre-Covid numbers by 10 p.m. Tellingly, that’s the same rate as 2022 despite a 10 percentage-point jump during the day. The situation is just as severe in most-famed nightlife districts such as Ginza.

All this contributes to an increasing sense of winners and losers. Savills Research is among those who seea widening “bifurcation between strong and weak offices,” as those who can afford to move to premium sites are able to attract talent in a tightening labor market. Even well-known areas such as Roppongi aren’t safe: Goldman Sachs Group Inc. is leaving for Toranomon, while Alphabet Inc. already abandoned the location for Shibuya before the pandemic. Thus, even as Tokyo’s working habits normalize, the landscape is quickly becoming unrecognizable.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.