It is unlikely housing prices are set to crash unless there is an unexpected shock (a “black swan” event).

It is unlikely housing prices are set to crash unless there is an unexpected shock (a “black swan” event).

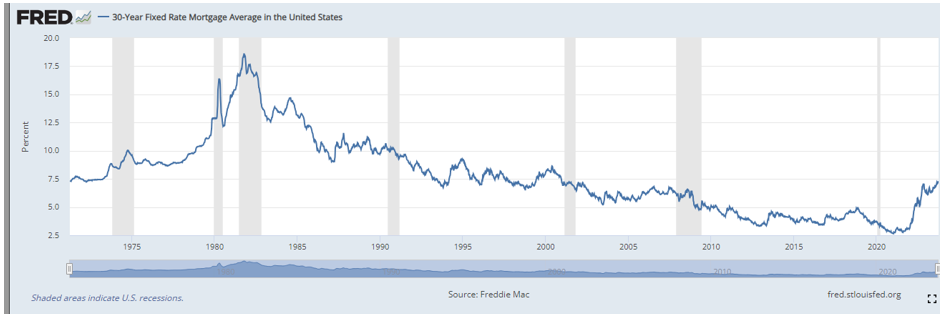

As the head of economic and financial research at Buckingham Wealth Partners, I’ve been getting lots of questions about the outlook for housing prices. The questions are driven by the sharp rise in mortgage rates, from a low of about 2.7% in late 2020 to about 7.3% at the end of September 2023.

The rise in rates has led to concerns that the housing market could be set to repeat the crash in prices experienced during the great financial crisis (GFC). According to the S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, housing prices fell by 27.4% from their peak in 2006 to their low point in 2012.

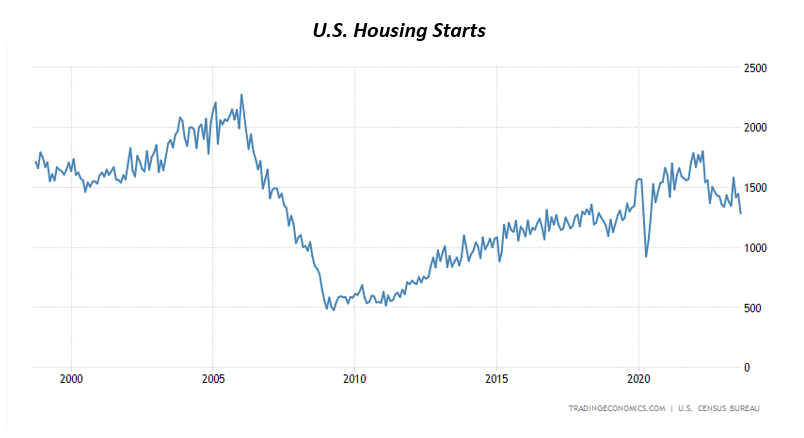

What causes prices to collapse is an excess of supply relative to demand. While that was the case for housing in the pre-GFC period, when there was lots of speculative building fueled by easy credit, that is certainly not the case today. In the post-GFC era, several factors have led to a sharp drop in new home construction: dramatically tightened lending standards, restrictive zoning regulations, shortages of labor and material and rising land costs. As seen in the chart below, housing starts have remained well below the levels reached in 2005 (far more than two million) since then; the August 2023 figure was under 1.3 million.

Andrew Haughwout, Richard W. Peach, John Sporn and Joseph Tracy, authors of the 2013 National Bureau of Economic Research study, “Housing and the Financial Crisis,” estimated that 3 to 3.5 million excess housing units were produced during the boom. In contrast, the reverse is true today, as we have been faced with a continuous shortage of new housing construction since the GFC. The estimates of how large the shortage is varies widely. For example, a June 2023 report by Zillow put the estimated shortage at 4.3 million homes: “This lack of housing – especially affordable options – has left millions of households ‘missing.’ These missing households consist mainly of individuals and families living in another family's owned or rented home. Across the country in 2021, there were nearly 8 million missing households, compared to just 3.7 million housing units available for rent or sale, a deficit of 4.3 million homes.”

On the other end of the spectrum, Kevin Corinth and Hugo Dante, authors of the July 2022 study, “The Understated ‘Housing Shortage’ in the United States,” used a supply-and-demand framework and county-level data on land shares of home prices. They defined a housing shortage in a particular market as the gap between the current number of homes and the number of homes that would exist absent supply-constraining regulations. They estimated that the U.S. housing shortage was 20.1 million homes in 2021, 14.1% of the national housing stock: “Our housing shortage estimate is 4 to 5 times as large as previous estimates.” They added: “Consistent with predictions of economic theory, our estimated housing shortage is uniformly low in areas with low regulation but varies in areas with high regulation, since a housing shortage requires both stringent regulations and strong housing demand.”

Restricted supply

Economists have long recognized that regulatory barriers to housing development restrict supply, increase home prices, and have negative economic consequences. Local land-use regulations – referred to as “not in my backyard” (NIMBY) regulations – such as minimum lot sizes, height restrictions, occupancy limits, parking-space requirements and permitting delays impose costs on the development of housing. When too few homes are built each year and demand grows, prices rise.

Supply is also being restricted because today about 61% of all outstanding mortgages have an interest rate below 4%, including 23% that are below 3%. With current mortgage rates above 7%, very few homeowners will give up their current homes because their mortgages are not transferable. The lack of supply leads to bidding wars, pushing prices higher. The following chart shows the monthly supply of new houses in the U.S.

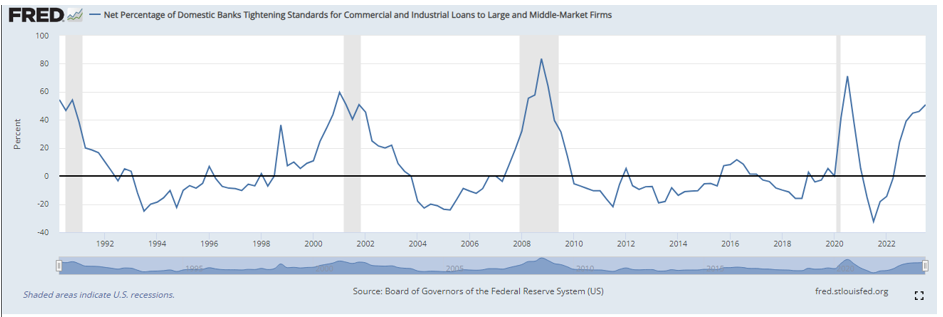

In addition to the high level of interest rates, yet another reason that the housing supply is restricted is that bank lending standards have tightened dramatically since the collapse of Silicon Valley Bank. That makes it both harder and more expensive for builders to acquire funding and for borrowers to obtain loans.

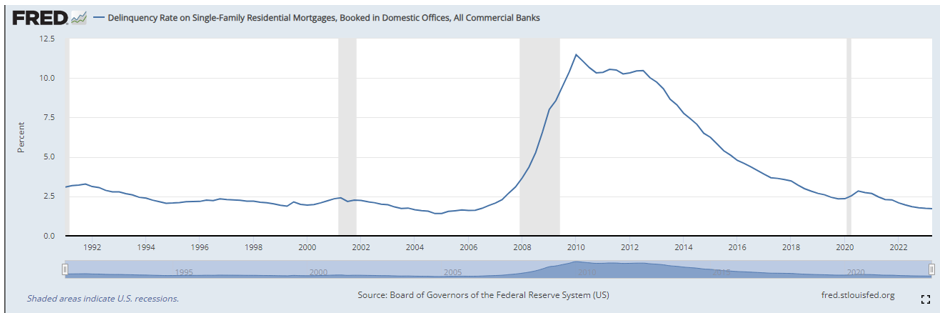

Reflecting the tightening of credit standards in the post-GFC era as well as the strong employment market (the unemployment rate is 3.8%), mortgage delinquencies are at historic lows, ending the first half of the year at just 1.7%. Low delinquencies mean it’s unlikely that banks will be forced to foreclose and put homes up for sale (which was the case in the GFC period), increasing supply.

Summary

While the long and variable lags in the Fed’s tightening monetary policy are starting to show signs of slowing economic growth, a combination of factors makes it unlikely that housing prices will come under strong downward pressure barring an unexpected shock to the economy:

- The huge shortage of housing should prevent prices from falling sharply.

- Housing supply remains at near historic lows – especially entry-level supply – consequently propping up demand and sustaining higher home prices.

- NIMBY policies continue to restrict supply.

- Tight credit conditions are limiting new home construction.

- Tight labor markets, and inflation in general, are driving building costs higher.

- More than 60% of existing home mortgages are below 4%, restricting supply.

- Mortgage delinquency rates are at historic lows.

But unlikely doesn’t mean impossible. In fact, two of the biggest and most common mistakes investors make are treating the unlikely as impossible and the likely as certain, leading them to take too much risk and concentrate risks. There are mounting headwinds to the economy in the form of the resumption of student loan repayments, increased energy prices, higher interest rates, tightening credit standards, slowing employment growth, the potential for a prolonged auto strike, and the potential for a shutdown of the government in November. Individually, they might not be sufficient to push the economy into a recession (which could drive unemployment up sharply and home prices down), but collectively they could. And there is the risk that the Fed, with its emphasis on driving inflation down to its 2% target, could make a policy mistake, raise rates too high, and push the economy into recession. Finally, there are always unknown risks that could negatively impact the economy and thus housing.

For those who are contemplating buying a home and are delaying doing so because of the risk that a recession could lead to falling home prices, that might not be a good strategy. Should we enter a recession, the historical evidence suggests that the Fed would act quickly and drive rates down sharply (the Fed has tended to raise rates slowly and lower them quickly), which would in turn lower mortgage rates and unleash considerable pent-up housing demand. The result could be higher, not lower, home prices.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners, collectively Buckingham Strategic Wealth, LLC and Buckingham Strategic Partners, LLC.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed adequacy of this article. Mentions of specific funds should not be construed as a recommendation. Certain information may be based on third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. Buckingham is not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. LSR-23-568

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

More Real Estate Topics >

It is unlikely housing prices are set to crash unless there is an unexpected shock (a “black swan” event).

It is unlikely housing prices are set to crash unless there is an unexpected shock (a “black swan” event).