The latest economic data for the US are better than most dared hope a year ago. Inflation has fallen much faster than the Federal Reserve expected, and so far without the abrupt economic slowdown and higher unemployment that many economists thought likely. With prices coming back under control, investors are confident that the next move in interest rates will be down. The only questions are when and how much.

Caution would be wise. A hoped-for soft landing is increasingly plausible, but this won’t make the Fed’s job any easier. At their meeting this week, the central bank’s policymakers need to weigh risks and uncertainties that could still upend expectations.

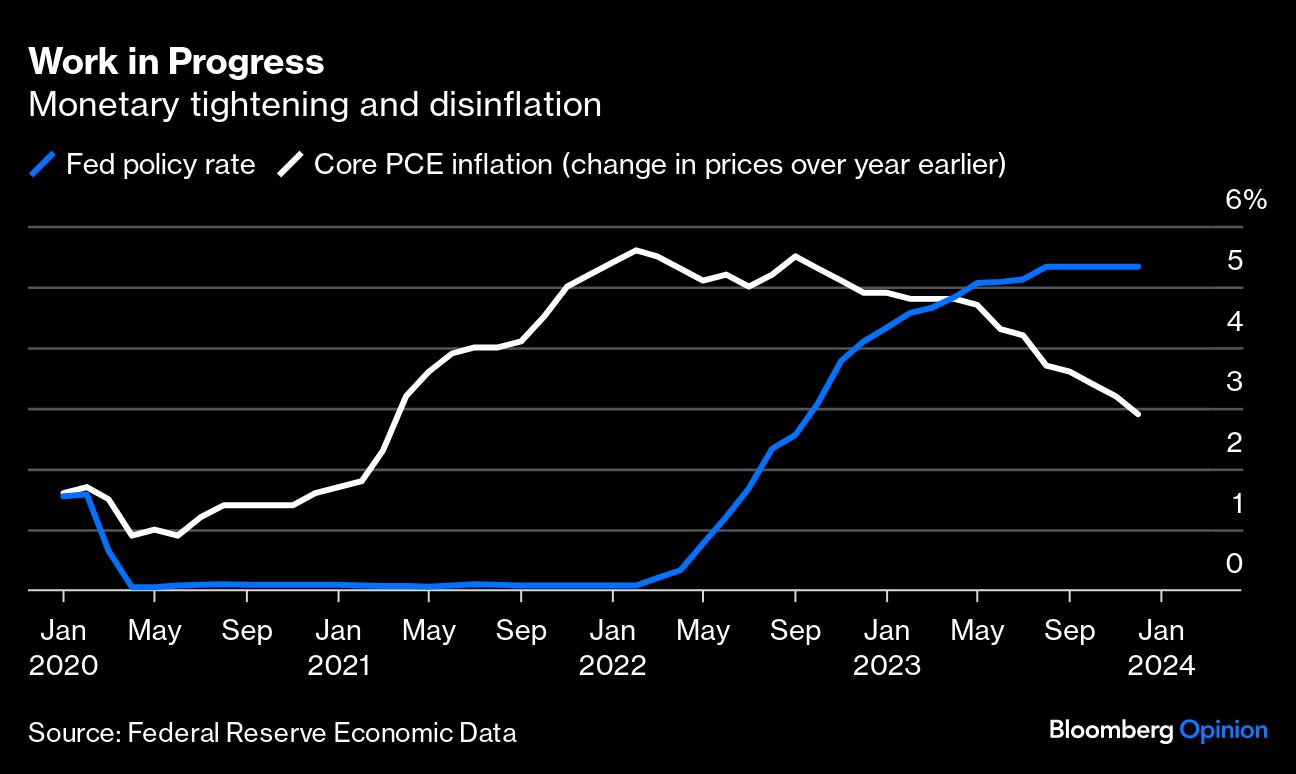

New inflation figures confirm the progress made so far on inflation. The Fed’s preferred measure — the price index for so-called core personal consumption expenditures — rose 2.9% in December from a year earlier, down from 3.2% in the year to November. If anything, this understates the recent pace of disinflation. For the second half of 2023, core PCE prices went up by just 1.9% at an annual rate, bringing that metric back to the Fed’s 2% target.

Even so, it’s too soon to declare victory. The combination of tight money and steady consumer demand, along with very low unemployment and falling inflation, is indeed welcome — yet at the same time puzzling. Last year’s forecasts stand refuted left and right, which argues for humility in predicting where things go from here.

On the face of it, an economy that’s growing, with a strong labor market and rising wages, doesn’t need extra demand and lower interest rates. Market sentiment rests partly on the assumption that the Fed’s firm monetary tightening starting in the spring of 2022 can and should be reversed as soon as lower inflation permits: In other words, with inflation suppressed, monetary policy should get back to normal. This reasoning is questionable. First, the Fed hasn’t quite yet delivered on-target inflation. Second, as the array of recent forecasting errors attests, what was normal before the pandemic may no longer work. The upheaval in the jobs market, for instance, has distorted the relationship between quits and vacancies, making it harder to judge how tight conditions are and hence where interest rates should be.