Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

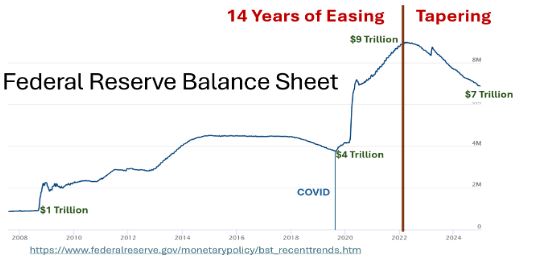

In response to the 2008 stock market and real estate crash, the Federal Reserve stimulated the economy by reducing interest rates to (almost) zero under its zero interest-rate policy (ZIRP). It “printed money” that amazingly did not bring serious inflation, yet.

Quantitative easing (QE) worked. The economy chugged ahead without a recession and the stock market skyrocketed with its longest bull market ever. Mission accomplished, despite the acceleration of QE in the face of COVID.

The Fed took its foot off the ZIRP brake in 2022. Here’s the Fed’s balance sheet journey so far. The balance sheet is decreasing as bonds mature without being replaced.

Note that there’s still $6 trillion sloshing around in the economy that threatens to bring inflation. The Fed’s balance sheet at $7 trillion is $6 trillion more than the $1 trillion historical average.

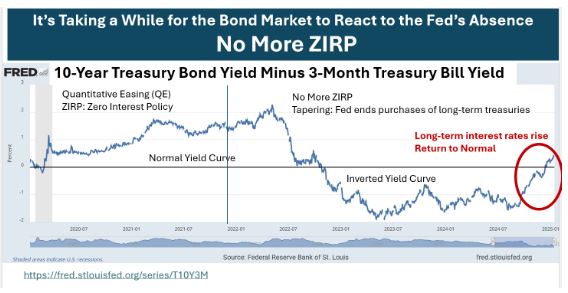

Interest rates react

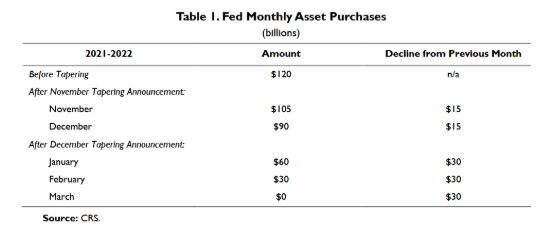

Since ZIRP required the Fed to buy long-term Treasuries at low interest rates, you’d think that tapering would result in interest rate increases, but what actually happened is shown in the graphic below:

At first, short-term Treasury bill interest rates increased faster than long-term bond yields, so the yield curve inverted, with Treasury bills paying higher interest than Treasury bonds. The implication of an inverted yield curve is that investors expect interest rates to decline in the future, typically because they expect lower inflation ahead.

That’s changed in the last several months, as long-term interest rates have been increasing. With the Fed no longer in the long-term bond market, market forces are establishing fair prices. Rising long term interest rates reflect buyers’ expectations of rising inflation.

Trouble ahead

Rising interest rates are not good for stock prices because future earnings are discounted at higher rates and bonds compete with stocks as a safe alternative. Will rising interest rates burst the bubble? Stay tuned.

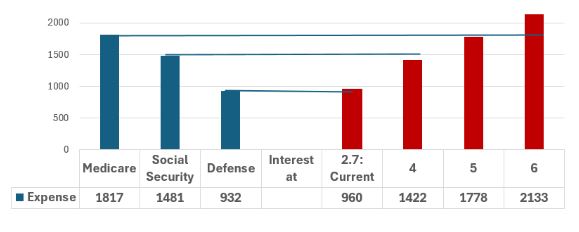

And rising interest rates can lead to a “debt spiral” where service on our $36 trillion – and rising – debt is financed by “monetizing”: borrowing even more to pay the interest. Interest payments on our debt are now the third-largest expense, even higher than defense, and will become our largest expense if interest rises above 5%.

Conclusion

There are many explanations to choose from for why long-term interest rates are increasing. In my opinion, it’s caused by inflation concerns coupled with the absence of the Fed. Inflation concerns are being reflected in bond prices because the Fed is not intervening to keep interest rates low. In order for new Treasury bonds to clear the market, the Treasury’s ask must find the buyer’s bid. This was not required when the Fed was buying whatever did not clear the market at the Treasury’s ask.

Why do you think long term interest rates are increasing?

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.