I recently asked DeepSeek to model the impact of artificial intelligence on US labor productivity growth. Its calculations suggested that the positive impacts would be discernible in the medium term (5-10 years) and quite substantial further out (a decade and beyond). That’s broadly in line with estimates proffered by reputable economists. But ironically, DeepSeek failed to account for the lessons we’ve learned from DeepSeek itself over the past few weeks.

I’ll get back to the DeepSeek productivity model shortly. But first, consider how the AI timeline may have changed this month. On Jan. 20, the Chinese company wowed users by releasing its R1 model, which seemed to exhibit performance competitive with the best US models but at a fraction of the price. It’s true that some deep-in-the-weeds tech people probably saw this coming (my tech columnist colleagues Catherine Thorbecke and Parmy Olson first wrote about DeepSeek months ago). But to many of us, DeepSeek was a revelation that showed — to borrow the words of venture capitalist Marc Andreessen — that the world was experiencing a Sputnik moment. AI was coming hard and fast. It was going to be cheaper and more accessible than many of us imagined. And governments around the world — especially in the US and China — were going to race to ensure that their people and companies were beneficiaries.

Will that mean macroeconomically significant productivity benefits next year or the year after? It’s hard to say for sure, but we shouldn’t be shocked if they come sooner than previously expected. Here’s how Goldman Sachs Group Inc. economists including Joseph Briggs put it in a note Thursday (emphasis mine):

The potential for a faster buildout of AI platforms and applications—which we continue to see as the necessary step to facilitate adoption across a wide swath of companies—raises the prospect of a more optimistic adoption and productivity boost timeline. Our forecasts currently assume that US adoption reaches levels necessary to impact aggregate productivity statistics in 2027 with a peak impact in the early 2030s, with other DMs and major EMs lagging this timeline by a few years. The recent DeepSeek reports suggest adoption could happen sooner...

As Goldman notes, AI adoption rates are still strongest in the information sector (publishing, data processing, etc.). Those areas account for less than 2% of nonfarm jobs in the US, and other sectors will have to find productive uses of generative AI technology for the breakthroughs to have a major macroeconomic impact. But with recent developments, it’s quite possible that companies will be able to develop and deploy such applications faster than many previously imagined. It’s not that big employment sectors — health care and manufacturing, for instance — don’t want to use AI. Arguably, they’re just waiting for the right tools to arrive.

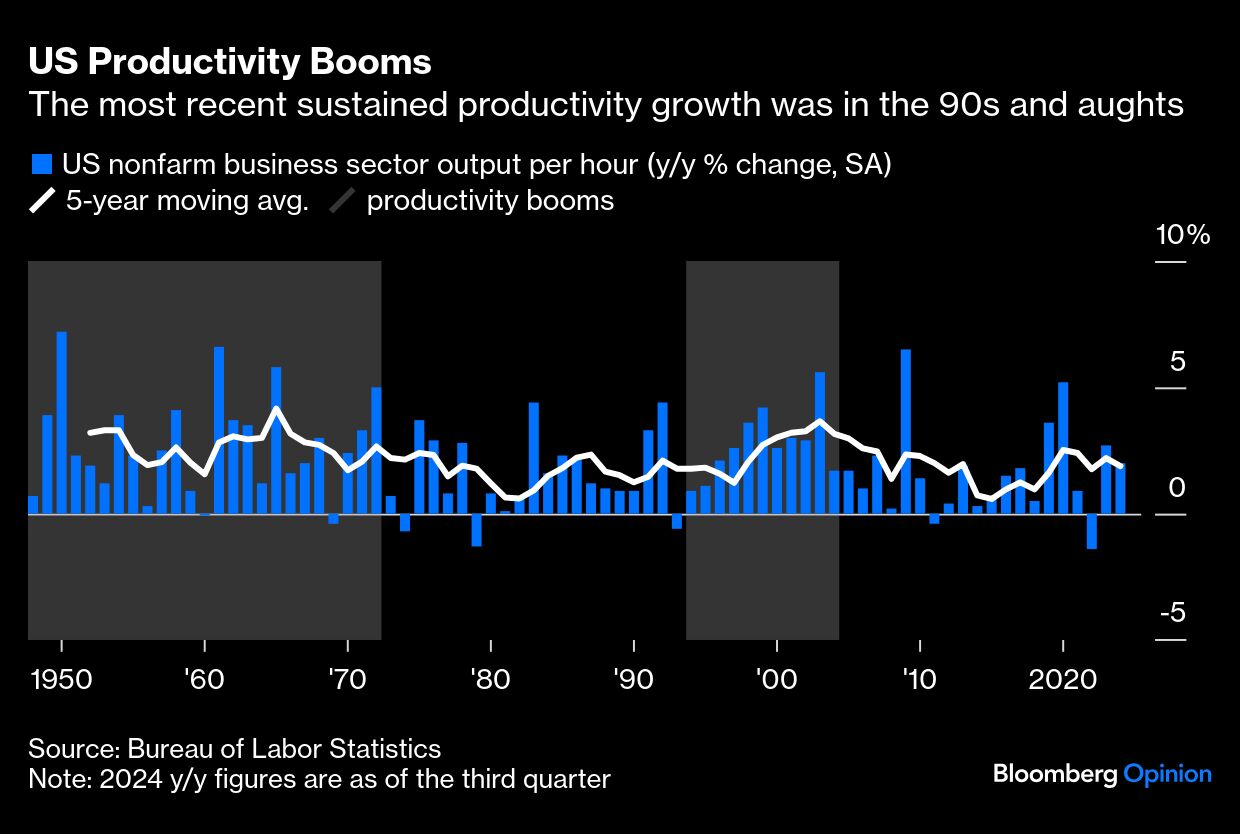

Productivity — defined here as production per hour worked — is a bit like magic fairy dust for an economy. As the US experienced after World War II and then again in the 1990s, productivity has the potential to deliver strong and sustainable economic and wage growth without the accompanying inflation. I get why it sounds too good to be true, and why blind faith in productivity’s magic might even be a bit dangerous: It could make policymakers complacent about the many other pressing economic problems facing the US, including the unsustainable path of the national debt. (Example: “The debt will probably be fine, since productivity-driven growth will boost the denominator in debt-to-GDP ratios.”) Americans should start thinking about how AI will affect their work lives, but act as if it may be a very long time coming.

In fairness, conservative estimates are consistent with the historical experience. The adoption of personal computers and the advent of the internet provide some highly imperfect guidance on the timeline. In 1968, Hewlett Packard released a desktop computer available for a cost of $4,900 (around $44,059 today). But it wasn’t until the late 1980s and 1990s that falling costs enabled widespread adoption among workers and individuals. With that and booming internet use, productivity finally took off from the late 1990s until the early 2000s. More recent technological advances have exhibited different patterns. Smartphones became a part of the work landscape very quickly in the late aughts. But as research by the Federal Reserve Bank of St. Louis has shown, other recent technologies (cloud computing, 3D printing) appear to have spread throughout the economy much more slowly.

There’s still a lot we don’t know about DeepSeek, and I don’t mean to suggest that the Chinese firm itself has supercharged the AI story — it’s just a wakeup call, and an invitation to other companies to follow suit. Similarly, it’s mind-bogglingly difficult to know how all of this will shake out in the US stock market. Just one example of this is the utilities sector in the S&P 500 Index, which posted one of its strongest performances of the millennium last year on the idea that AI would require extraordinary amounts of power. In early trading on Monday, the news that DeepSeek had trained a generative AI chatbot on the cheap prompted utilities to tumble. Later that afternoon, they were rebounding on the idea that we would still need a lot of energy to run AI models, especially as they spread to more people and industries.

It’s hard to ignore how impressive this tech already is. In a post on Substack on Monday, Stony Brook University Professor of Economics and Public Policy Stephanie Kelton shared what happened when she asked DeepSeek to create “a model and run a simulation to show the impact on Canadian GDP if the US imposes 25% tariffs on all exports from Canada to the US.” She showed how DeepSeek reasoned, calculated and spat out its findings, which Kelton said were roughly consistent with results from experts at the Bank of Canada. “I wonder how long it took the staff at the BoC to come up with their figures,” she wrote. “It took Deepseek about 12 seconds.”

Taking my cues from Kelton, I asked DeepSeek to “please create a model to estimate how soon we may see economically significant gains to US labor productivity from artificial intelligence.” DeepSeek first defined “economically significant” as a “sustained increase” in labor productivity of 0.5 to 1 percentage point annually. That would come on top of the roughly 2% gain we’ve seen in recent quarters, or the long-term trend of 1.5%. It correctly identified that the drivers of such productivity would come from AI adoption rates, technological advancements, industry-specific impacts, labor market adjustments (workforce “reskilling”) and infrastructure and investment (“availability of data, computing power, and investment in AI technologies.”) In all, the 785 word answer included some assumptions that I disagreed with, but it was transparent about how it got to its answer. It was also slightly dated, since — as DeepSeek will tell you — its training data doesn’t go beyond 2023. But the conclusion (below) seemed like a reasonable starting point:

Economically significant gains in U.S. labor productivity from AI are likely to emerge in the medium term (5-10 years), with transformative impacts in the long term (10+ years). By 2030, AI could contribute 0.5-1.0% annually to productivity growth, reaching the threshold for economically significant gains. However, the exact timeline depends on adoption rates, technological advancements, and policy support.

That answer is so impressive that it could very well be wrong — or at least a bit too conservative.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin