President Donald Trump may have found a way to force the Federal Reserve to lower interest rates after all.

It’s no secret that Trump wants lower rates. He also wants more say in monetary policy, even though he already has the power to name the Fed chair and two vice chairs, subject to Senate confirmation. It would be a mistake for the central bank to cede any more of its independence to this president or any future one, and I doubt it will.

But Trump may have a backdoor to the Fed. The central bank’s monetary policy garners a lot of attention and often criticism. Less noticed is the impact of fiscal policy, which has been at least as consequential as the Fed’s historic moves in recent years.

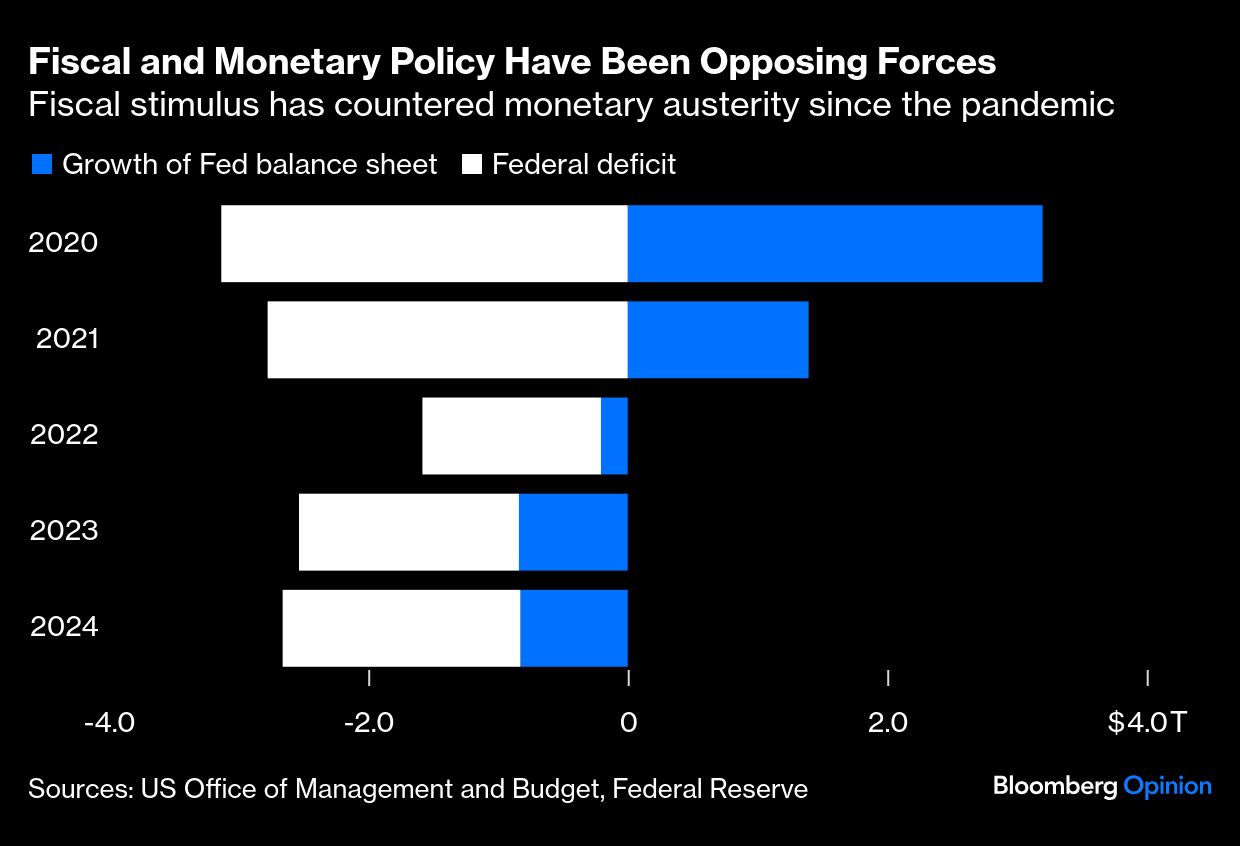

Fiscal and monetary policy have diverged widely since the Fed began its fight to bring down inflation. The Fed has tried to slow the economy by raising short-term interest rates more than 5 percentage points in just over a year beginning in 2022, the biggest rate increase in five decades, before pulling back modestly last fall. It has also trimmed its balance sheet by more than $2 trillion since the rate-increase campaign began, or about a quarter of its original size.

Fiscal policy has taken the opposite path. Congress has injected huge amounts of fiscal stimulus into the economy in the form of $4.2 trillion in cumulative deficits since spring of 2022, or about 6% of gross domestic product over the same time. For perspective, annual deficits as a percentage of GDP have averaged 2.6% since World War II. That includes the outsized deficits Congress ran during the 2008 financial crisis and again during the pandemic — rightly, I have repeatedly argued — to support a collapsing economy. No wonder the US has dodged a recession in recent years.

Fiscal and monetary policy may now be set to trade places. Treasury Secretary Scott Bessent has said the administration wants to trim the deficit to 3% of GDP. That would require Trump’s Department of Government Efficiency to find $1 trillion in spending cuts. It’s not yet clear to what extent it will succeed, but the mere threat of cuts may already be dampening sentiment and impeding the economy.

Signs to that effect are accumulating. Consumer sentiment declined in January for the first time in six months. The Bloomberg US Financial Conditions Index has tumbled 37% in the past two weeks, implying that economic activity is slowing. The Atlanta Fed’s estimate of annualized real GDP growth in the first quarter has been cut nearly in half, to 2.3% from closer to 4% a month ago. The yield on 10-year Treasuries has dropped 50 basis points to 4.3% over that time and is fast approaching the one on two-year Treasuries, a trend many economic observers view as an omen of looming recession.

A slowdown, particularly one accompanied by a weaker labor market, would most likely prompt the Fed to lower rates. It’s hard to see the central bank easing otherwise. The latest read of core personal consumption expenditures — the Fed’s favored inflation gauge — came in at 2.8% year over year in December, which is still uncomfortably higher than its 2% target. As long as the economy is growing and keeping a lid on historically low unemployment, the Fed can delay rate cuts until inflation is tamed.

By cutting spending, however, Trump may force monetary easing to support fiscal austerity rather than the other way around. It doesn’t even matter if Trump’s spending cuts cause the economy to slow. As long as those cuts — or threat of them — coincide with a slowdown, the Fed will likely act.

That scenario could be derailed in several ways. Trump’s tariffs could stoke inflation even as his spending cuts slow the economy, resulting in a bout of stagflation that would prompt the Fed to raise interest rates despite a slowdown. Or, more optimistically, spending cuts could make room for more private sector investment, as the administration hopes. That could continue to bolster the economy and the labor market, giving the Fed more time to tackle inflation.

Whatever happens, it’s clear that the White House, aided by an accommodating Congress, is pursuing a new fiscal path. The Fed will have to grapple with the fact that Trump has found some influence on monetary policy, whether it likes the intrusion or not.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Nir Kaissar