Treasuries Cling to Best Rally Since July on Mild Inflation Data

Membership required

Membership is now required to use this feature. To learn more:

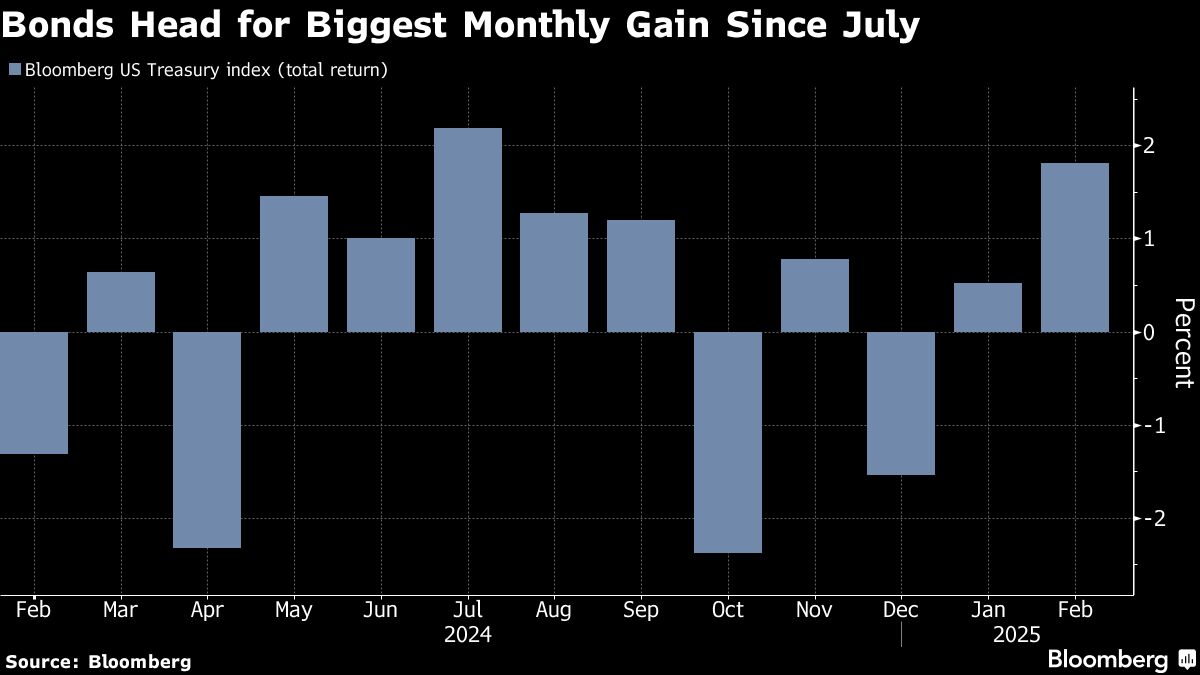

View Membership BenefitsInvestors in US government bonds are wrapping up their biggest monthly gain since July as the Federal Reserve’s preferred gauge of underlying inflation rose at a tepid pace in January.

The advance this week in Treasuries pushed the benchmark 10-year note’s yield to briefly touch 4.22% on Friday, the lowest level since December, as a series of weak economic growth indicators revived the case for the Federal Reserve to resume cutting interest rates after its recent pause. The yield was near 4.25% after the report.

The price indexes for January personal consumption expenditures, or PCE, came in line with economists’ estimates, offering some relief on the inflation front. Traders continued to bet on two interest-rate reduction for the year, with the first fully priced in by July.

Now, the focus turns to February employment data to be released next week

“The evolution of the labor market is going to be a big one,” said Neil Sutherland, portfolio manager at Schroders. “The tradeoff at the moment in the bond market is between the higher inflation and lower growth. And the lower growth dynamic is starting to pull through at the moment.”

The drop in yields over recent sessions helped nudge the Bloomberg US Treasury Index higher by 1.7% in February, as of Thursday’s close. It’s also the best start to a year for Treasuries since 2020, with the index up 2.2%.

It’s a demonstration of how rapidly fortunes can shift in the world’s biggest bond market. Just over a week ago, the 10-year yield was still above 4.5% and seen as likely to entice sellers at that level based on the potential for a trade war to promote inflation.

But since then, a string of softer secondary economic indicators in the US combined with US President Donald Trump’s tariff threats and the elimination of federal government jobs as key drivers.

“The market’s really forward looking here and focusing on the knock-on effects of those government job cuts,” said Brian Quigley, senior portfolio manager at Vanguard. “If they’re cutting spending, they’re cutting funding for other programs, you can have government contractors and the like being negatively impacted as well.”

What Bloomberg Strategists Say...

“Debt is clearly outpacing stocks this year — fitting right into the set of so-called Trump trades that have fallen by the wayside. Treasuries don’t often enjoy the sort of strong start to a year they are experiencing — 2008, 2016 and 2020 were the only better initial rallies this century.”

— Garfield Reynolds, MLIV Asia Team Leader

Investors exited bearish positions, and activity in Treasury options featured wagers anticipating the 10-year yield could fall below 4%. Morgan Stanley strategists said such a move was possible if investors come around to the view that the Fed will cut interest rates by another full percentage point, about twice as much as they currently expect. That could happen if hiring trends soften, driving unemployment higher.

For now, the Fed remains sidelined by inflation rates that still exceed its long-term target of 2%. But if it has to choose between supporting growth and fighting inflation, “the Fed will focus on growth,” Quigley said. “Whether they ease or they don’t in a growth scare, the market will price in more aggressive Fed easing.”

A Citigroup Inc. gauge of divergence between the data and economists’ expectations for it this week reached the most negative level since September.

George Catrambone, head of fixed income, DWS Americas, said the firm turned neutral on 10-year Treasury debt this week after buying in January when the yield reached 4.8%.

Inflation angst is likely to keep the 10-year yield between 4.25% and 4.75%, said Janet Rilling, senior portfolio manager at Allspring Global Investments.

“Labor markets are largely balanced, but inflation is stubborn,” she said. “There’s still work to be done on inflation,” which “to us, presents a risk for fixed income markets. We don’t feel like it’s all clear on that front.”

The ICE BofA MOVE Index, which measures implied volatility on a basket of fixed-income assets, has risen to a six-week high as expectations for Fed policy have shifted.

Later Friday, the bond market could find support from month-end buying by index funds and other passive investors. Month-end rebalancing of bond indexes to add securities sold during the month and remove ones that no longer fit the criteria is projected to provide a larger-than-average boost to its duration, a key risk metric, around when the changes take effect at 4 p.m. New York time.

While sellers prepare for the event, it can still lead to higher prices if demand exceeds expectations. The projected duration increase is 0.12 year versus a monthly average of 0.08 year over the past year, related to the large quarterly auctions of new 10-, 20- and 30-year notes and bonds in February.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All