A Dividend Is Not a Gain (or a Loss)

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

“Everyone knows” there are two ways to make money with stocks: price appreciation and dividends. “Everyone” is wrong. There is only one way to make money with stocks: capital appreciation. A dividend is not a gain.

Of course I overstate the “everyone” here. In fact, the truth is readily ascertained by anyone who has studied corporate or investment finance. Yet we indulge the myth of dividends-as-gains for rhetorical convenience, and in doing so, we encourage all manner of dividend-related nonsense1 to pervade the spheres of finfluence, where susceptible masses ingest investment ideas, quite often to their detriment.

Allow me to elucidate with a story problem:

Q: Ian Ingenuous heard that Acme Mothballs Inc. had upped its annual dividend to $2/share, so he funded an investment account and purchased one share for $100 exactly. Assuming no market movement, what is the value of Ian’s account after the annual dividend is paid out?

A: $100, just as before, because a dividend is not a gain. If you answered $102, then this article is for you!

There is no magic investment return fairy

If a dividend is not a gain, then what is it? Here is my irony-drenched-but-accurate definition: A dividend is a sale of stock forced upon every investor by the company in which they are invested, in exchange for cash to which they already had a claim, for which the government demands you pay taxes on the entire transaction instead of just the portion that represents accrued capital gains.

To unpack that definition, let’s begin in the middle: When a company pays out a dividend, it does not magically conjure previously nonexistent cash to do so. The cash comes from the company’s balance sheet, and the money that is paid out to you represents a portion of the balance sheet to which you were already entitled, by virtue of the partial company ownership you acquired when you bought the stock.

As I recently discussed in a series of posts on LinkedIn, there is no magic investment return fairy, and this general principle therefore implies specifically that a dividend is not a miracle performed by a magic investment return fairy. A company cannot create value simply by paying out a dividend. Rather, a dividend is nothing more than a transfer of cash from your share of a company’s balance sheet directly to your own balance sheet.

In doing this, the company shrinks its own asset base, and the value of your ownership claim shrinks proportionally.2 This means you have more value in cash and less value in company stock than you had before, which is what makes a dividend functionally equivalent to selling some of your stock.3

While the sale of stock might “capture” a gain, the gain itself is accrued through market-driven appreciation in the value of the stock before you sell it. The same is true for a dividend-paying stock: If you make money, it is from the stock appreciating in value. The appreciation may be – and, in the long run, likely is – driven by the company earning profits, profits it may then choose to dividend-out.4 However, do not mistake the dividend itself for the profitability that both drove the stock gains and made possible the dividend.

Note also that just as the gain capture upon asset sale triggers a tax liability (if the stock is held in a taxable account), so too does a dividend. But note the dividend is worse in this regard for two reasons:

- The company, not you, decided to swap the cash for the stock, and you get no say in the timing of any resulting taxation.

- Whereas taxes are only due on the portion of a stock sale that represents a capital gain, the entire dividend is effectively taxed as though it were a capital gain … even if, in fact, you had no gains at all in the stock.

Also, a dividend is not a loss

One source of confusion for the notion that a dividend is a gain is the way dividend accounting is performed. When your quantity of cash goes up and the value of your stock goes down by equivalent amounts, there are two forms in which the latter element could be represented:

- Your share count could be proportionally reduced. This is, of course, how the accounting works when you sell some of your stock.

- Your value per share could be proportionally reduced. This is how it is done when a dividend is paid out.

This is merely an accounting convention,5 but it lends itself readily to a mistaken belief that you’ve suffered losses in your stock. Just as the “dividend gain” is a myth, so too is the offsetting “stock loss” upon the distribution of the dividend. Yet this method of accounting for dividends lends itself readily to a false “price return” versus “total return” dichotomy, whereby the stock is inappropriately “punished” for losing value and the dividend inappropriately “rewarded” for creating value, when in fact all that has occurred is an exchange of value from stock to cash.

In consequence, even those who know better – including those who correctly preach that only total return matters6 – slide easily into speaking about total return as “a combination of capital gains and dividends” or “price return plus dividend return.” This extremely common but lazy practice gives aid and comfort to the twin myths that a dividend is a gain (thanks to the magic return fairy manifesting cash) and a loss (since the offsetting drop in the stock price is thereby falsely promoted to a negative capital gain).

‘Price return’ vs. ‘total return’ indexes

A major culprit for this widespread misconception is an inexcusable holdover from the precomputer age: that popular monument to calculational indolence, the “price return” index.

In the olden days before modern technology, accurate stock dividend data could be difficult to obtain in a timely fashion and was therefore difficult to incorporate into return calculations for stock indexes (such as the Dow or the S&P 500).7 Due to the above accounting convention, the construction of such indexes incorporated “price return” only, thus effectively – and falsely; don’t miss this point – punishing the stock of any index component company when it issued a dividend. This was always bad, but in pen-and-paper times, it was at least understandable.

Later, when modern technology made it easy to handle dividends properly – i.e., recognizing that they represent neither creation nor destruction of wealth, but rather just conversion of wealth from stock to cash – this gave birth to a vastly superior construct: the total return index.

However, due to an extraordinary degree of industry inertia, price return indexes – which should long ago have been entirely supplanted by their total return brethren8 – are often still referenced, quoted, employed in calculations, etc.

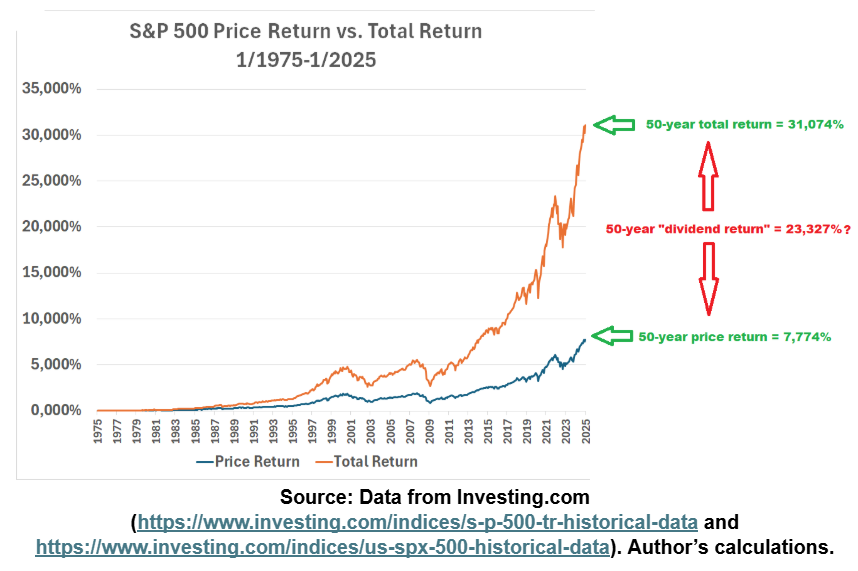

Combined with the previously discussed fiction that the difference between price return and total return is somehow “dividend return,” the persistence of the price return index gives rise to a diabolical bit of mathiness, in the form of a belief that “dividends account for most of the stock market’s return over the long run.”

The argument sets up as follows:

“Over the past 50 years, S&P 500 Index total returns (~31,000%) are much higher than S&P 500 price returns (~7,800%). Therefore, dividends account for about 75% of stock market returns over the long run.”

So say the blind to the blind.

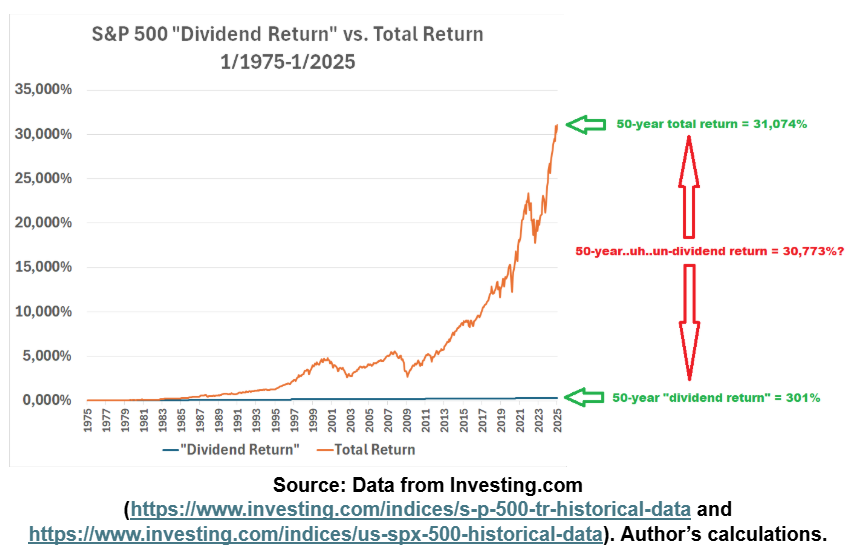

The sliver of truth in this towering tomfoolery is that if the magic investment return fairy’s evil twin caused all dividend cash to disappear into the ether (i.e., if a dividend really was a loss, as falsely implied by a “price return” index), then you would indeed have accrued 75% less return. However, crediting the long-run arithmetic return difference to “dividend return” stems from ignorance of the mathematics of compounding. To see this, suppose we construct a “dividend return” monthly series, comprising the total return less the price return each month, compounded over time:

In annualized terms, the 50-year S&P 500 Index total return is about 12.2%/year. The illusory “price return” is about 9.1%/year and the yet-more-illusory “dividend return” is about 2.8%/year. In the absence of a magic investment return fairy, 2.8% does not become larger than 9.1% over time, and the only sense in which “dividend return” accounts for 75% of historical stock market performance is a sense in which “price return” accounts for 99%. Yet even that observation is silliness, because “dividend return” is not a thing at all (a dividend is not a gain), and “price return” blindly ignores the reality that a dividend is not a loss.

Conclusion

Such madness could have been avoided had we been better about imparting the fundamental truth that a dividend is not a gain … or a loss. Go ye henceforth and impart likewise.

In his roles as chief investment officer for Round Table Investment Strategies and portfolio manager for Torren Management, Nathan Dutzmann is responsible for applying financial science and investment research to the process of constructing portfolios tailored to the individual needs and goals of clients nationwide. Nathan was previously an investment strategist with Dimensional Fund Advisors and a partner and chief investment officer with Aspen Partners. He is also a member of the investment industry advisory council for The American College of Financial Services. He holds an MBA from Harvard Business School and a master’s degree in international political economy and a bachelor’s degree in mathematical and computer sciences from the Colorado School of Mines.

Endnotes

1 One example of said nonsense: “Dividends are a stable source of return for stocks, and this makes them safer.” Admittedly, dividend stocks in aggregate tend to have lower volatility than nondividend payers, so how is this nonsense? Let us count the ways:

- A dividend is not a gain. A return of capital is not an investment return.

- Insofar as this aphorism has a grain of truth, it is due to correlation between dividend payers and stably profitable companies. If dividend payers are indeed somewhat safer, it is because a) consistently profitable companies are somewhat safer; and b) consistently profitable companies are more likely to be dividend payers. But if any such company decided to stop paying dividends and to pay out their profits through buybacks instead, the resulting lack of dividend would make them no less safe. (Relatedly, a concentrated investment in dividend payers is likely just an inefficient way to pursue the profitability, quality, and/or value factors.)

- This assertion is often explicitly predicated on the notion that dividends themselves are stable. But there is no requirement for companies to continue paying a dividend, or to hold steady the amount if they do. Companies change their dividend policy all the time. Also, who cares? See points 1 and 2.

- A desire to project spurious “stability” can cause some companies to maintain their dividend long after it ceases to be prudent to do so. Returning capital to shareholders even after a company’s cash balance has dropped below its operating capital requirements is a classic “value trap” move.

2 A complication here is that market movements don’t take a break on the ex-dividend date; i.e., the date on which the dividend is effective. This volatility makes it more difficult to isolate the otherwise precisely offsetting stock drop.

3 Those wishing for more rigorous proof are invited to read the paper, “Dividend Policy, Growth, and the Valuation of Shares” by Profs. Merton H. Miller and Franco Modigliani. Profs. Miller and Modigliani were ultimately awarded the Nobel Prize in economics for brilliant research in which they repeatedly proved that $1 does, in fact, equal $1. They were, in a sense, the final arbiters on the nonexistence of a magic investment return fairy. They are also known in finance circles as “M&M”… which is less relevant but at least equally fun.

4 To be clear, a company choosing to return cash to its shareholders is not, ipso facto, a bad thing. I agree with those who argue that stock buybacks are often a more efficient means of doing so, but dividends are just fine in the abstract. Just don’t confuse them for gains.

5 It is a very understandable convention, as proportional adjustments in share ownership would be a much more complex method of accounting. The share count would have to be reduced by a quantity proportional to the amount of the dividend divided by the closing market capitalization prior to the ex-dividend date. It is understandably not worth doing things this way, since the chosen alternative requires no adjustments to share count. (Conversely, the creation of “Treasury stock” as a nonsense asset when a buyback is performed – which would presumably also be the case if dividends were accounted for in this alternative manner – can itself lead to bogus analyses.) However, this simpler no-adjustment accounting hides the fact that each share now represents the same percentage of a smaller pie – which is why stock prices on average will open on the ex-date “down” by the value of the dividend (though, see endnote 2) – precisely offset by the slice of pie now sitting as cash in your brokerage account. The “dividend as gain and loss” mythology this foments is an unfortunate side effect of accounting ease.

6 I can’t resist calling out another common, noxious myth. Here is a direct quote, the source of which I will hold anonymous to protect the guilty:

“The ‘dividends are irrelevant and only total return matters’ argument doesn't seem to me to hold up in a severe, protracted bear market. If you're selling shares after stock prices have crashed and you still need the same amount of money, you're selling a much larger percentage of your shares than you were before the crash. Depending on the severity of the crash that could be devastating.”

I hope by now you can spot the nonsense. A dividend is economically indistinguishable from a stock sale. If selling stock in a downturn is dangerous (a much longer topic, with no opinions offered here), then extracting an equivalent quantity of dividend “income” rather than reinvesting it is dangerous to the exact same degree, for the exact same reason; there is no difference whatsoever, except that dividends are fully taxable even in a downturn.

7 Pierre-Cyrille Hautcoeur, “The Early History of Stock Market Indices, with Special Reference to the French Case,” Paris School of Economics: https://www.parisschoolofeconomics.com/hautcoeur-pierre-cyrille/Indices_anciens.pdf

8 I applaud the efforts of Index Fund Advisors’ founder Mark Hebner and others to pressure the industry for the rectification of this ongoing travesty.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All