The tiny German village of Rehden, halfway between Hamburg and Frankfurt, is the unlikely ground zero for the next phase of the European energy crisis.

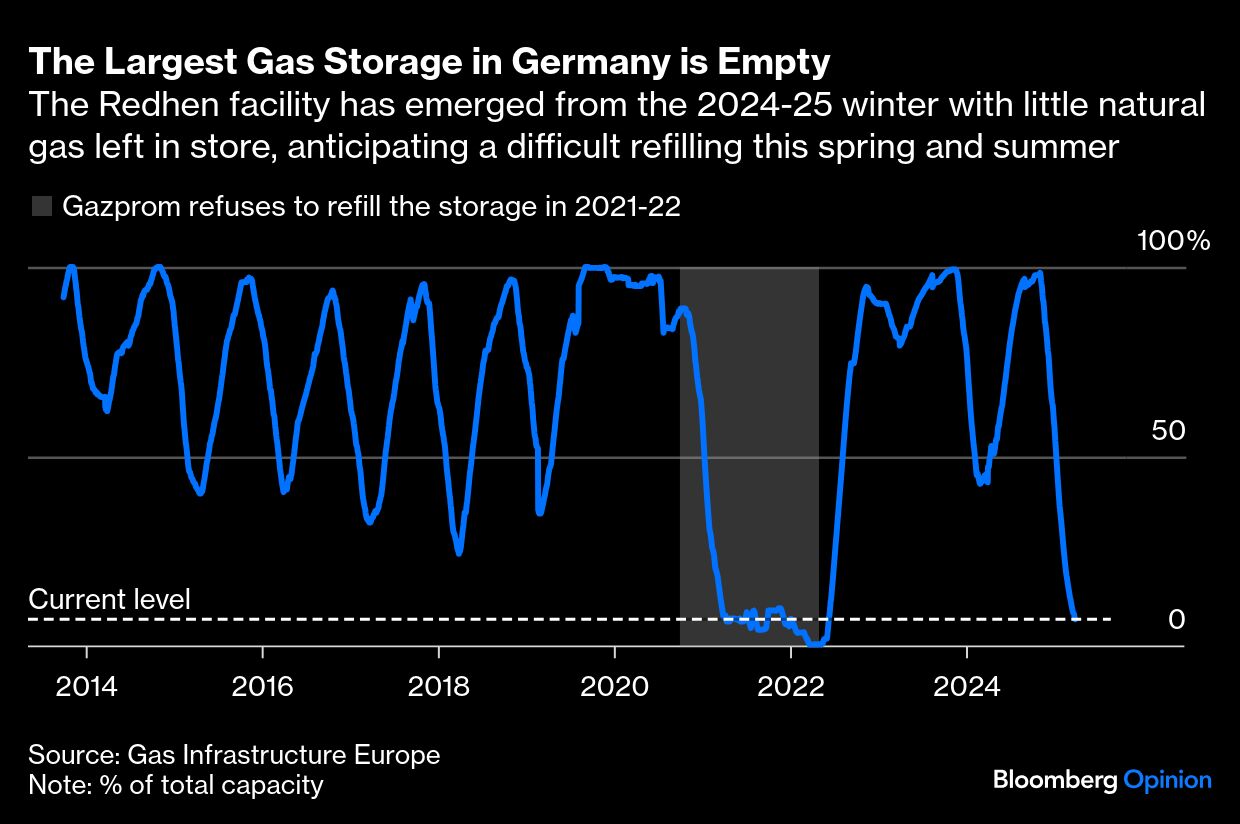

In the pastoral scene above ground, the cows graze. It’s below where the drama is playing out: 2,000 meters (1 ¼ miles) beneath the surface lies Germany’s largest natural gas storage site, capable of stocking enough gas to heat 2 million homes for a year. Now almost empty, the cost to fill it for next winter totals almost €2 billion ($2.2 billion) at current prices.

But a once-routine process has given way to questions of when to fill it and who will foot the bill. At stake: the cost of heating for European families next winter — and for policymakers, a potential inflationary surprise. The underground Rehden storage, which spreads over a surface equal to 910 soccer pitches, is now hostage to a game of chicken, involving commodity traders, utilities, Brussels regulators and even Vladimir Putin.1

The outcome, replicated across dozens of other European gas storage sites, will shape the summer season for the market, which formally started on Tuesday as traders closed the books on the 2024-25 winter. If nothing changes, the summer season will be the fifth in a row to see Europe fighting high prices and uncertain supply due to Russia’s invasion of Ukraine.

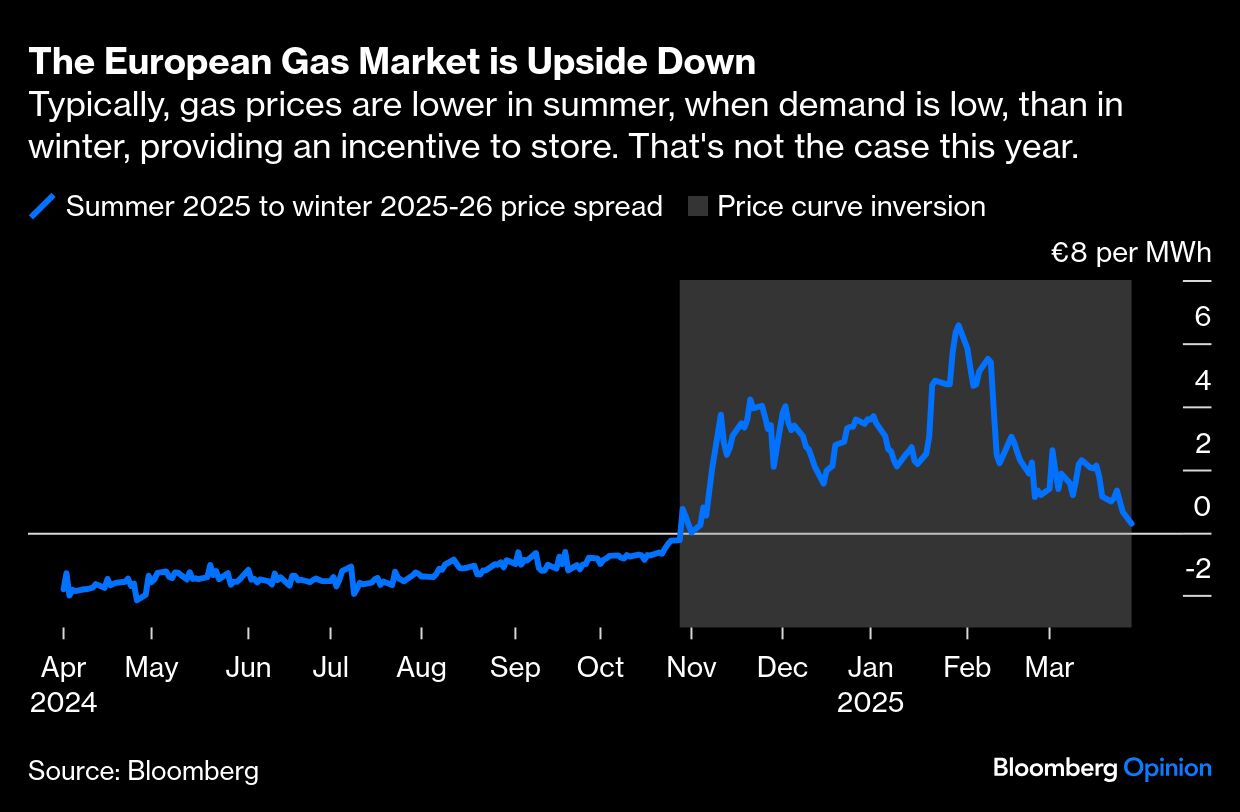

Typically, everyone chips in to refill storages like Rehden via the invisible hand of the market. Because demand for gas is low during the spring and summer, the fuel is cheapest so that’s when utilities and traders buy gas and store it underground. At the same time, they sell forward the same gas for delivery in winter to customers seeking to lock in costs. Typically, the summer-to-winter price spread is wide enough to cover the storage fees and financing costs, plus a profit.

But that hasn’t been the case for five months. The market is inverted from its typical structure: Gas is as expensive this spring and summer as for delivery next winter. The reason has a lot to do with the situation in places like Rheden: Inventories have finished the winter lower than usual, and without Russian pipeline supplies, Europe needs to pay higher prices to attract liquefied natural gas cargoes away from other regions. Fortunately for Europe, global LNG production is rising and, so far this year at least, China isn’t buying a lot of LNG, so the competition isn’t intense

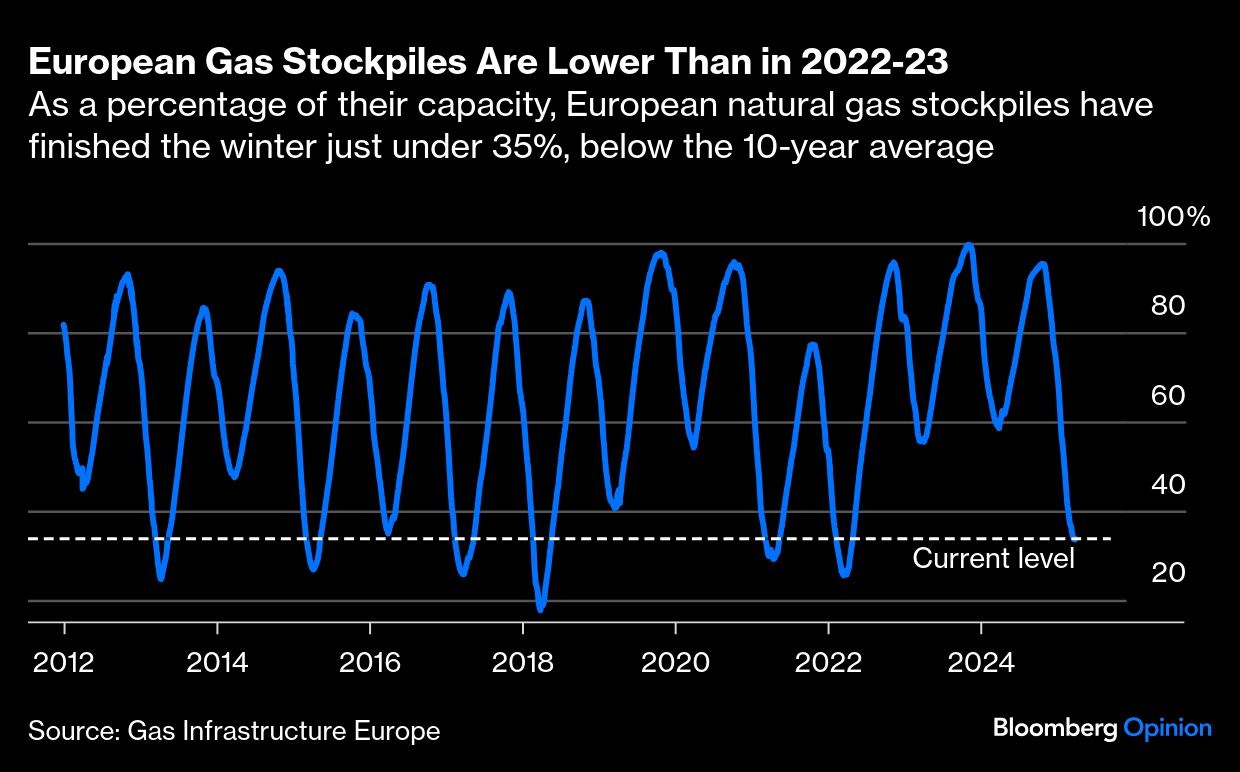

European gas inventories ended the 2024-25 year at one-third of capacity, significantly lower than the 55% and 58% of the last two previous seasons, which were warmer than usual. It only took a normal winter to expose the fragility of the supply-demand balance. The loss on Jan. 1, 2025, of Russian pipeline gas via Ukraine didn’t help; nor did several weeklong periods of windless weather, which lowered renewable electricity output, requiring more gas-fired production. Rehden itself is virtually empty, at about 7% of capacity. Over the last 15 years, the site had only been lower once — in 2021-22, when its owner at the time, Russian state-run gas giant Gazprom, refused to inject molecules into storage. Berlin nationalized the site in late 2022 after the Ukraine invasion.

Here’s where the regulators come in. The European Union has mandated that storage sites need to be refilled to 90% of capacity by Nov. 1. Brussels is reviewing the mandate after multiple member countries complained. Under discussion is an alternative to refill the storage between 80% and 90%, giving countries leeway. Brussels isn’t likely to announce any change until April 14, when officials are scheduled to debate the issue.

Typically, European gas inventories start to climb from late March, particularly during weekends when consumption is lower. So far, very little has gone into storage. Gas traders expect to see more injections as April progresses, in part because some storage – particularly in France – was contracted back in September and October 2024, before the price spread inverted; so pushing gas into those sites makes economic sense.

But the lack of price incentive since November has stopped many from booking storage capacity. Gas traders believe that about 50% of all storage in several European locations – notably Germany – remains uncontracted. SEFE, the German state-owned energy supplier, recently said that “current marketing of storage capacities continues to be challenging, considering the market environment.” When SEFE tried to market storage capacity in the Rehden site back in January, it failed.

The result is the game of chicken.

European policymakers appear to be hopeful that as demand for gas plunges in the first weeks of April, the surplus will push spring-summer prices below those of next winter, creating the economic incentive to store the gas. If Brussels reduces the storage target from 90% to, say, 85% or even 80%, reducing the amount of gas that needs to be procured from April until late October, the spread can shift even quicker. The market is already anticipating that policy move.

So far, the spread is moving in the direction governments want to see. From a peak of more than €6 per megawatt-hour, it has fallen to €0.5 per MWh. Still, that’s far above the minus-€2 per MWh seen in September-October, when some storage was contracted. Unless prices for spring and summer fall well below next winter’s, the gas won’t flow into storage.

On the other side of the game are some utilities, commodity traders and hedge funds. All are anticipating that inventories will only increase slowly this month, which would trigger alarm bells in European capitals about having enough gas for next winter. If they’re right, European countries may put taxpayer money on the table to make sure the gas is purchased and stored. Germany mooted a public intervention in the gas market earlier this year but later adopted a wait-and-see attitude.

The wild card is Putin. If Moscow and the US cut a deal over Ukraine some of its pipeline natural gas flows may return to Europe before next winter.

My guess is that everyone is going to wait until mid-May. By then, the early trajectory of how much gas is set aside at facilities such as Rehden will be clearer. But if 2025-26 winter prices fail to rise significantly above spring-summer quotes by then, governments will need to act.

1. Rehden was originally a natural gas field, in production from the early 1950s. The field was converted into a storage facility in 1993. It accounts for around 20% of the total gas storage capacity available in Germany.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Javier Blas