US Treasuries tentatively resumed their gains on Tuesday after the wildest day for bond traders since the height of the pandemic in March 2020.

Yields on 10-year US bonds fell three basis points to 4.16%, after a volatile start to the week that saw yields whip between gains and losses. German rates remained higher, while UK gilts recouped some gains after long-end yields surged on Monday by the most since former Prime Minister Liz Truss’ 2022 mini-budget.

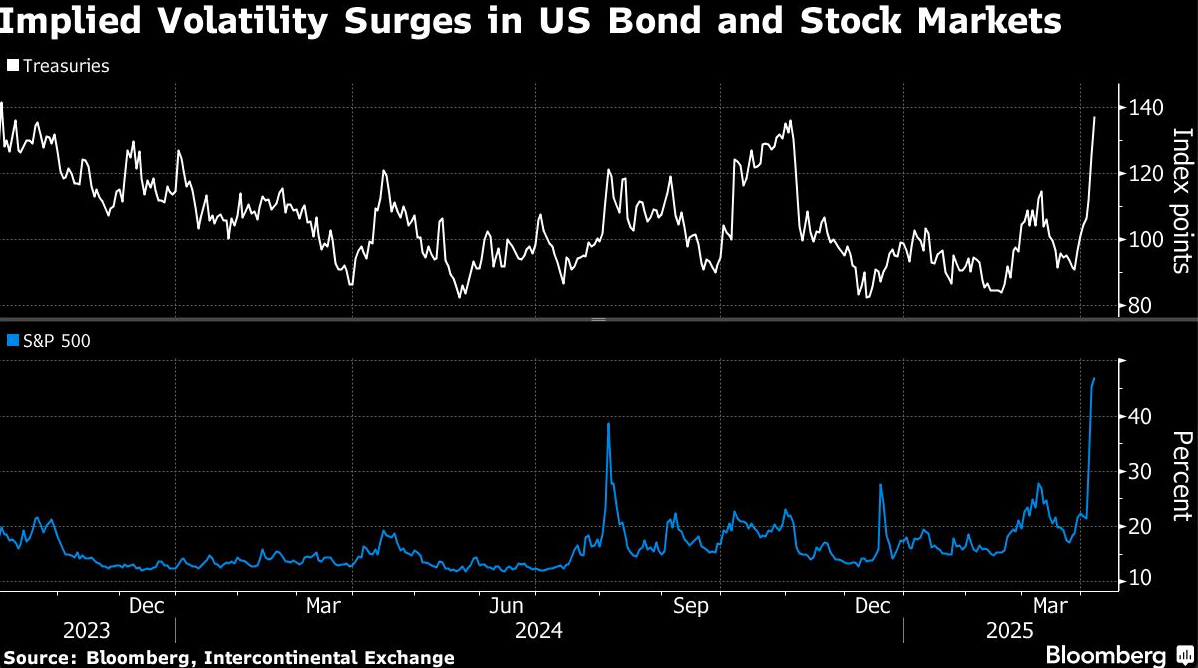

The relative lull came as a relief to traders after a fraught day of trading in the US. With little clarity on whether President Donald Trump is willing to offer relief on his tariffs, a gauge of Treasuries implied volatility has soared to its most extreme level since October 2023. Currency fluctuations are at the highest in two years, and the VIX index of equity volatility has hit an eight-month high.

Traders threw out a number of possible reasons for Monday’s whiplash: a market primed for a pullback after such a sharp rally; lurking concerns about tariffs stirring inflation or necessitating government stimulus; liquidations in favor of cash-like instruments; or even rumors that foreign owners, including China, were selling.

“Markets have somewhat stabilized after a couple of dizzying trading days,” said Elias Haddad, senior markets strategist at Brown Brothers Harriman. “Regardless, the pervasive uncertainty created by continuously changing US tariff threats and the scope of potential retaliatory measures remain a major blow to the global economy. Bottom line: relief rallies in risk assets will likely be short-lived.”

Treasuries were in the grip of a third-straight day of gains when rumors surfaced on Monday that the administration was considering a 90-day pause on tariffs. Bonds quickly reversed, with the US benchmark yield abruptly soaring about 15 basis points over the following 5 minutes, before the White House labeled the report “fake news.”

The speed of the reversal was arguably unsurprising; markets remain desperate for any sign that the Trump administration will tone down or negotiate its tariff demands. But its stickiness was notable in the wake of the White House denial.

Investors meanwhile scoured US dollar funding markets for signs of weakness, with memories of liquidations in 2020 that created a crunch in the Treasury market and necessitated Fed intervention. While dealer holdings of Treasuries remain near an all-time high, the market for repurchase agreements so far looks stable.

“Until yesterday, you would have said financial conditions tightened but bond markets remain orderly. Yesterday was a bit of a shift in that,” Maya Bhandari, multi-asset strategies EMEA CIO at Neuberger Berman, said on BTV. “If this bond rout has legs, that strengthens the case for the Fed to respond. But it’s got weaker growth and stickier inflation so it’s not in an easy spot.”

The market’s next big test will come from the Treasury’s sale of $58 billion new three-year notes on Tuesday, followed later this week by offerings of 10-and 30-year debt.

An auction of 30-year government bonds in Japan met weak investor demand. The cut-off price at the auction relative to the average price was minus 0.75 yen, the lowest since December 2023 when it registered a record low.

“Trump’s policies have low predictability and are prone to changes,” said Winson Phoon, head of fixed income at Maybank Securities Pte in Singapore. “The volatility in bond yields and rates pricing are likely to persist for the US and, to a certain extent, other markets too.”

Still, traders are starting to find alternatives to Treasuries as havens, with bunds and Japanese debt looking more attractive to foreign buyers on a currency-hedged basis.

The US bond selloff “may be signaling a regime shift whereby US Treasuries are no longer the global fixed income safe haven in periods of risk-off,” Ben Wiltshire, G-10 rates trading desk strategist at Citi wrote in an e-mailed note.

Markets are pricing about 97 basis points of interest-rate cuts in the US this year — equivalent to three quarter-point cuts and an 88% chance of a fourth, after pricing as many as five cuts on Monday.

BlackRock Inc. warns the chance of a recession has increased if tariffs stay at this level but that it’s unlikely the Fed will be able to cut rates aggressively given the likelihood trade policies will boost inflation.

“The effect of tariffs is stagflationary,” said Wei Li, global chief investment strategist at BlackRock on Bloomberg TV. “The Fed is not going to be able to come to the rescue of the economy as readily as they were able to before.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Alice Atkins, Masaki Kondo