Student Loans Drive US Delinquency Rate to Highest Since 2020

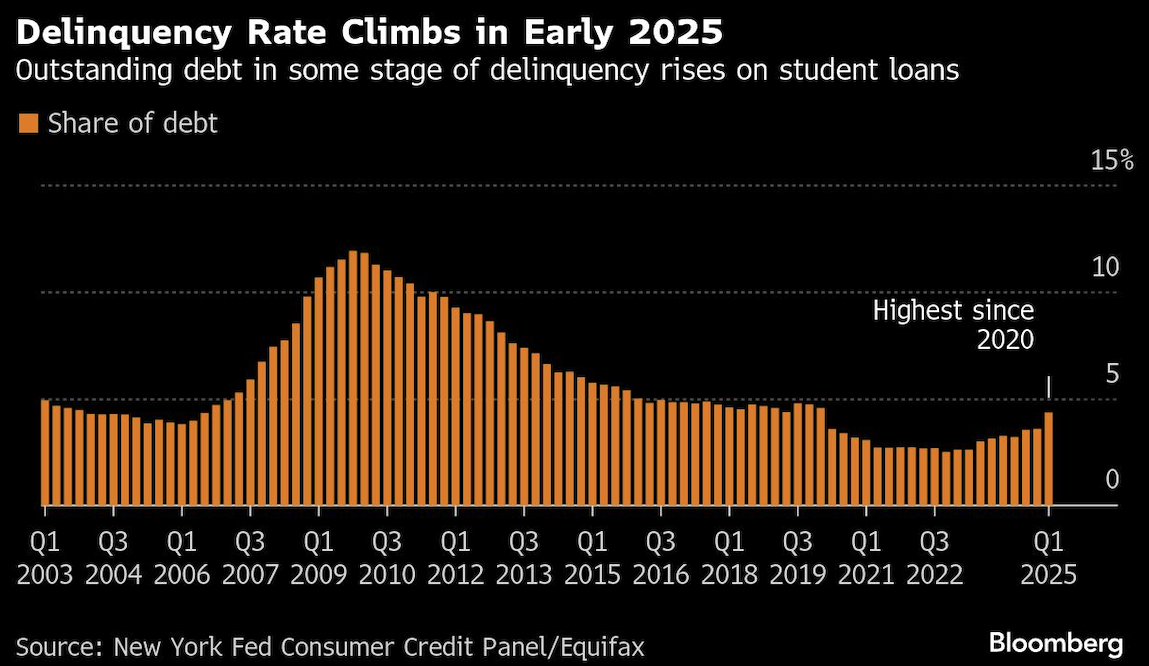

The share of outstanding US consumer debt that’s in delinquency rose in the first quarter to the highest in five years, reflecting an end to the pandemic-era pause on reporting delinquent student loan payments on credit reports.

Some 4.3% of debt was delinquent in the first three months of this year, the most since 2020 and up from 3.6% in the prior quarter, the New York Fed said Tuesday in its Quarterly Report on Household Debt and Credit. Outside of student loans, however, transition to early delinquency held steady for nearly all debt types.

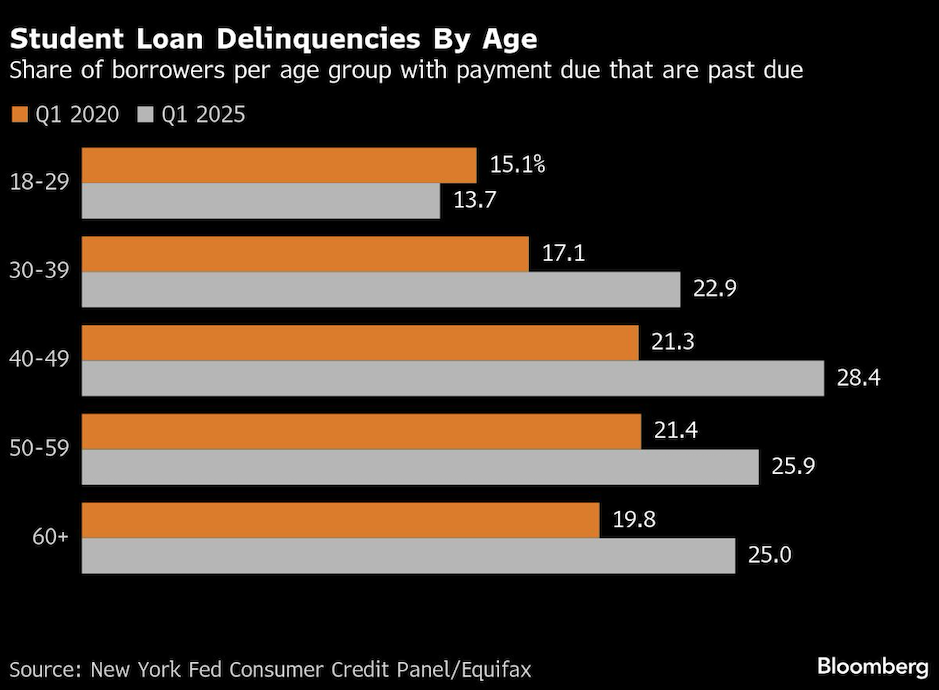

Missing payments on federal student loans have just begun to reappear on credit reports, following a years-long payment freeze. As a result, about 8% of student debt fell into serious delinquency — or was 90 or more days late — in the first quarter, up from less than 1% a year earlier.

“Transition rates into serious delinquency have leveled off for credit card and auto loans over the past year,” Daniel Mangrum, a research economist at the New York Fed, said in a statement. “However, the first batch of past due student loans were reported in the first quarter of 2025, resulting in a large jump in seriously delinquent borrowers.”

Debt delinquency rates have been on the rise since late 2023, as consumers battled elevated inflation and high borrowing costs. Total household debt — which is primarily composed of mortgages, student loans, auto loans and credit-card balances — increased by $167 billion in the first quarter to a record $18.2 trillion.

A pause on federal student loan payments gave some borrowers breathing room to pay off other debt and improve their credit scores. But now that those payments are once again being reported to credit bureaus, student loan delinquencies have returned more toward pre-pandemic levels, the New York Fed found.