The Most Revealing Question in Personal Investing…and How Warren Buffett Helps Us Answer It

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The Question

This is our single favorite question for shedding light on how you’re thinking about investing:

What is the lowest risk-free, after-tax, after-inflation rate of return you would accept in order to forgo all other investment opportunities for the rest of your life?1

The answer, along with the thinking behind it, speaks to whether and by how much you think you can beat the market in the long run, your level of personal risk-aversion, and the average tax rate you think you’ll pay on your investment returns. It’s a useful reference point to keep in mind when evaluating real-world investments, and also as one of the key inputs to figuring out your long-term spending policy.

Over the past ten years, we’ve discussed this question with about 50 of our friends and clients, resulting in many animated and productive conversations.2 We’d like to briefly explain our thinking, and then invite you to use our calculator, where you’ll also have the option to submit your answers for a survey we’re compiling.

Elm’s Answer

Here’s how we think a typical Elm investor might reasonably answer this question.

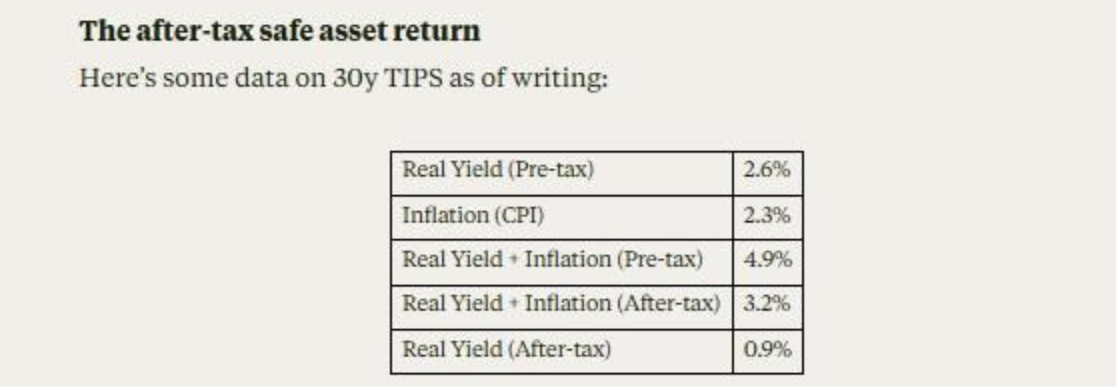

A good starting point is to calculate the after-tax, after-inflation return you could get from investing in 30-year TIPS.

We’ve assumed a blended income tax rate of 35% between taxable and non-taxable accounts,3 and based our CPI Inflation estimate on inflation swaps.4 We apply the tax rate to the total TIPS coupon including inflation, then subtract CPI to get the after-tax real yield. And we see 30y TIPS are offering a post-tax yield of inflation + 0.9%,5 which we’ll treat as the after-tax safe asset return.6

Now add stocks…

Inflation + 0.9% is a lower bound on what you would be willing to accept to forgo all other investments, since much of the investment universe should give you the opportunity to earn higher risk-adjusted returns. Let’s say you expect that investing in global stocks will give you an extra 4% return above 30y TIPS, on a pre-tax basis, or inflation + 6.6%. In fact, this is close to what we show in our Elm Wealth Capital Market Assumptions, which also happen to line up pretty well with the average from 15 leading asset managers and investment advisors. We’ll assume that investing in stocks is subject to a blended tax-rate of 18%, since much of the return comes as qualified dividends and long-term, deferred capital gains.7 This results in an inflation + 5% expected, after-tax return of stocks.8, compared to inflation + 0.9% for TIPS.

…but risk-adjust their expected return

Let’s say that given those expected returns, and your view of the long-term riskiness of stocks, you want to have 80% of your portfolio invested in stocks, and the rest in TIPS. Then the blended expected return on your portfolio will be inflation + 4.2%.

But stocks are risky! You need to turn that risky return into an equivalent risk-free return. A good rule of thumb is that the risk-free return equivalent to an appropriately sized risky return is equal to the expected risky return minus one-half of the excess risky return over the safe asset. In this case, the expected return is 4.2%, and the excess risky return is 3.3%, so we should be willing to accept inflation + 2.5% risk-free to forego our blended 80/20 portfolio.9

What if I can do better than passive index fund returns?

So far, we’ve only considered our investment opportunity set as comprising a static allocation to two assets: long-term TIPS and global equities. This might be what John Bogle would have advised, and what many Bogleheads today would settle on.

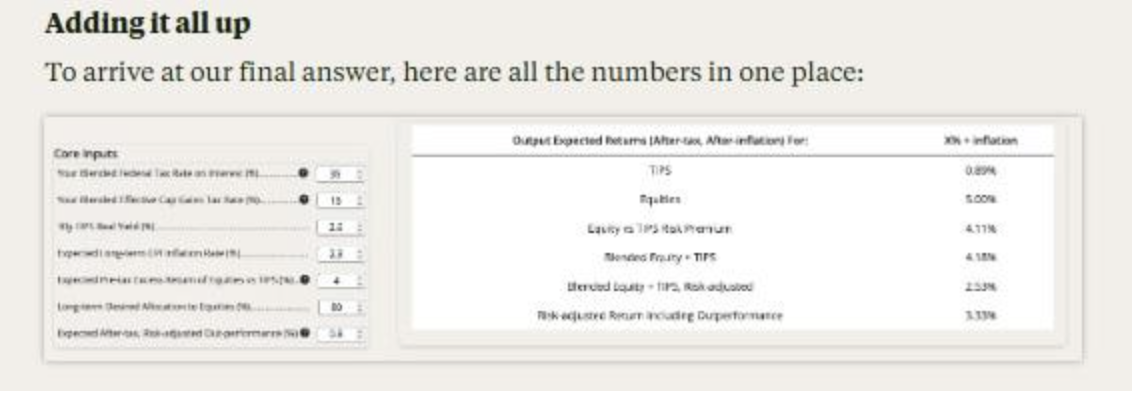

However, many investors think they can do better than that. For example at Elm, we expect that our Dynamic Index Investing® will add about 1% in pre-tax returns in the long run with a mild reduction in risk. So in today’s conditions and crediting our investment approach with an extra 0.8% of after-tax risk-adjusted return, our answer would be that inflation + 3.3% is the lowest after-tax, risk-free return we think a typical Elm investor would accept to abstain from all other investing forever.

Other investors may believe in other sources of extra return. They may believe that their ability to pick stocks, or to invest in alternatives such as private equity, venture capital or hedge funds will give them a higher risk-adjusted return. It’s challenging to quantify how much your acumen as an investor is worth, but there are some places to look for guidance on this question.

“I have long argued that the most important lesson of ‘financial literacy,’ one that is never taught in any ‘financial literacy’ classes, is: If I offer you a 20% annual risk-free return, am I lying?” – Matt Levine10

Good versus great: rating your inner Warren Buffett

To help narrow down the range of reasonable answers, let’s consider how much extra return the world’s most celebrated investors have been able to generate. When it comes to acclaimed investors, no one comes to mind more readily than Warren Buffett, often referred to as the GOAT of investing.11

Over the past 50 years, his investments through his holding company Berkshire Hathaway have generated a 20% compound return, a full 8% in excess of that delivered by the US stock market. That compound return would have turned $100 50 years ago into $1 million today. However, a more careful analysis of Buffett’s returns, such as by Frazzini et al in “Buffett’s Alpha”,12 finds that the outperformance taking into account Berkshire’s use of leverage is more like 4% per annum, still a remarkable achievement and probably the best over a 40-plus year horizon by any known investor. Between Buffett’s investment performance and the frequent glimpses we get into his investing thought process, there is little doubt that his performance is primarily attributable to skill rather than luck.

It may also be useful in forming your own expectations to note that Buffett’s returns over the past 25 years have been about 2.5% above the US stock market, much lower than the 8% excess return over the past 50 years. When adjusted for leverage, the 25 year outperformance is likely close to zero.

How about private market investing?

While Buffett generated his remarkable performance primarily through ownership of publicly traded stocks, mostly in the US, many investors these days are attracted to private, alternative investments. The closest comparable we have to Buffett’s achievement, but in the alternative investing space, is the excess return generated by the Yale endowment. For many years it was the most celebrated investor in private assets, particularly under the stewardship of David Swensen. Over the past 40 years, the return of the Yale endowment was about 2.5% in excess of the US stock market, with most of that outperformance occurring in the first half of Swensen’s time in charge.

Risk matters too

When thinking about how much extra return to add to what’s offered by broad, public equity markets, it’s also important to realize that there are only two ways to beat the market: 1) concentrated holdings and/or 2) leverage.13 Both of these bring extra risk to your portfolio, and so it’s not enough to generate extra return – you have to generate extra return in excess of the extra risk. For example, Buffett generated his returns with about 25% more risk than the US stock market.14 You should expect that if you’re going to generate higher returns through your investment selection, you will most likely be taking extra risk.

All in all, we think that for people who are confident they can beat the market, adding something in the ballpark of 0.5% – 1.5% (remember, we’re talking about after-tax and risk-adjusted here) to the risk-adjusted returns offered by broad public market asset classes is about as much as seems reasonable. For many investors who believe they won’t beat the market through active investing, it makes more sense to subtract a small amount for the fees charged by index funds, and possibly a low-cost wealth advisor if needed.

Connecting the Dots

Depending on your personal degree of risk-aversion, expected blended tax rate, and confidence in earning risk-adjusted returns in excess of those offered by broad public market portfolios, we think your answer to our question could reasonably fall somewhere between 2.5% to 6% above inflation, a pretty wide range. For investors that have most of their savings in taxable form, the range is quite a bit narrower, more like 2.5% – 4% above inflation.

We hope you’ll take a few minutes to explore our calculator and share with us your personal answer to this important question. If you provide your details, we’ll send you the survey results once we’ve compiled them.

You can find the calculator here: Lifetime Certainty-Equivalent Return Calculator

For those of you who enjoy investing so much that there’s virtually no return you’d accept to completely surrender the fun of investing, please think of the question as applying to 90% of your wealth, leaving the rest for your amusement.

Endnotes

1. Assume you’re starting from a clean slate, as if you just realized all your existing investments. Being paid to run an investing business is allowed, but you can’t invest any capital or participate in the investment returns yourself. Buying a house and collectibles for consumption purposes is also allowed, but not if the primary purpose is to generate investment returns.

2. Part of the variability in answers to this question come from the variability in market conditions over the past ten years. Long-term real interest rates offered by US Treasury Inflation-Protected bonds (TIPS) have being as low as -0.5% and as high as 2.6%, and the expected return and risk of US and non-US equities have also fluctuated widely. Answers also depend on the effective tax rate we bear on investment income, which also is quite variable across investors.

3. We have framed this note in the context of a US person subject to US taxation, but the framework is equally applicable for non-US investors subject to differing regimes of taxation on investment returns.

4. Or equivalently on the breakeven inflation rate implied by the difference between the TIPS real yield and the yield on equal maturity nominal Treasury bonds.

5. For the purposes of this note we use CPI and “inflation” interchangeably, recognizing that each of us has our own personal inflation basket which differs from the CPI basket.

6. Of course this isn’t a perfectly risk-free return, because US Treasury debt is not entirely risk-free, as is recognized by US sovereign CDS rates. If you wanted to factor this in, you might want to reduce the 0.9% by a credit spread of 0.4% or so.

7. Note the deferral here is particularly important in lowering this rate below the plain blend of the qualified dividend and capital gains rate.

8. (2.3% + 6.6%) * (1-18%) – 2.3% = 5%

9. 4.2% – (1/2) * 3.3% = 2.5%

10. “Gambling Is Not a Retirement Plan,” Money Stuff, June 2, 2020.

11. GOAT is not a reference to his age or personality, but rather as an acronym for “Greatest Of All Time”

12. Financial Analysts Journal 2018.

13. A cautionary note on the challenges of beating the market as a non-full-time investor is humorously-expressed by Agustin Lebron, a former Jane Street trader, in his excellent book, The Laws of Trading: “The profitable trades that exist in the world are either (a) the ones you’re intimately involved in running, or (b) the ones that are inaccessible to you. There is no ©. And what’s funny about the situation in trading is that, if we were talking about just about any other industry, the very notion of a © would be laughable. Imagine if someone who’s good at manufacturing cars came to you and said: ‘Hey. I’m a profitable car-maker. If you like, I’ll let you take all the profit from my car-making skill in exchange for a small fee for me.’ You would rightly suspect they’re trying to pull one over on you. So why is the situation different in trading?”

14. Over the past 35 years, using daily returns. Given Berkshire’s use of leverage, we’d expect most of this extra volatility from the leverage alone.

This is not an offer or solicitation to invest, nor are we tax experts and nothing herein should be construed as tax advice. Past returns are not indicative of future performance.

All errors are our own, they are fewer due to the help of our friends David Blob, Larry Hilibrand, Mark Jansen, and Jeffrey Rosenbluth, as well as our colleague Jerry Bell, who gave their comments on this article. An extra thanks to Larry Hilibrand – the first time we heard this question was from Larry over 30 years ago.

Victor Haghani is founder & CIO of Elm Wealth, a Philadelphia-based asset manager. James White is Elm Wealth’s CEO.

Learn more at www.elmwealth.com.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All