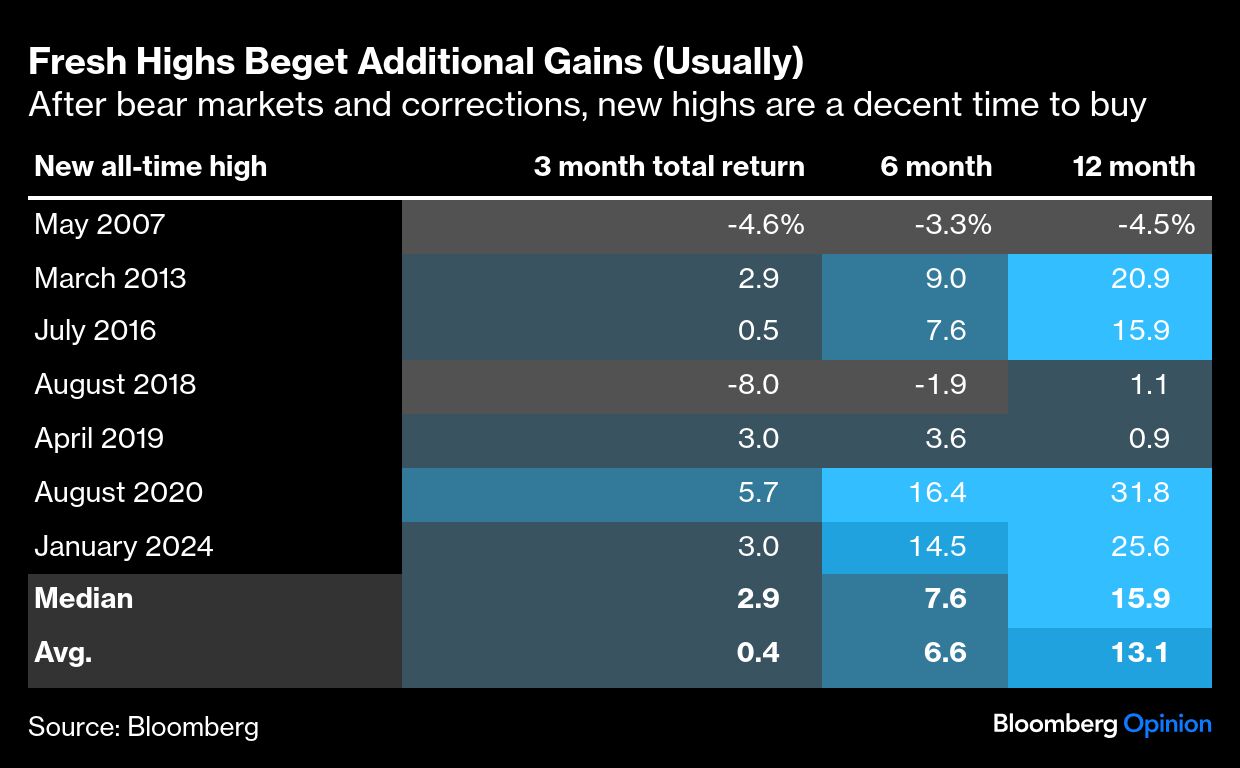

The S&P 500 Index just rallied back to all-time highs, brushing off the April tariff shock, the conflict with Iran and the insidious and persistent increase in US continuing jobless claims. A growing chorus of bears thinks traders are whistling past the graveyard, and they’re far from crazy to think so. But then again, index highs almost always feel like this.

Consider August 2020, when the Covid-19 pandemic was still in full swing. The government data had put unemployment at over 10%, and yet blended forward price-earnings ratios were in the 99th percentile of the previous two decades. There was some general optimism about the prospects for a vaccine, but clinical trials were still ongoing and a summer surge of Sun Belt cases had dashed hopes for a quick resolution to the pandemic disruptions. Meanwhile, a popular narrative posited that “dumb money” retail traders were driving the stock rally. How did that turn out? Even after the Aug. 18 high, the index returned another 11.5% in 2020 and 28.7% in 2021. Not too shabby.

There were plenty of doubters near the all-time highs of early 2024 as well. China concerns were weighing on the global growth outlook, and Middle East tensions were running high after the October 2023 Hamas attacks on Israel. At the same time, Wall Street strategists thought the index had outrun its full-year potential. Yet the S&P 500 closed at a new high on Jan. 19 and never looked back, returning 23% in the rest of 2024.

So what can go right this time for markets to, yet again, defy the naysayers?

The clearest bull case runs through soft-landing interest rate cuts. If the impact of tariffs on consumer prices proves more muted than expected, the Federal Reserve can start to normalize policy rates by September, potentially unlocking a wave of new corporate and consumer borrowing. Consider that the policy range stands at 4.25%-4.5% today, and 11 of 19 Federal Open Market Committee participants think that the so-called longer-run neutral rate is at or below 3%. In other words, they have plenty of room to cut if they get the “all clear” from the data.

While it’s true that some rates cuts are already priced in, the market may be underestimating how quickly and deeply policymakers may move. Lower rates would provide a shot in the arm to the struggling housing, auto and labor markets. Hundreds of thousands of would-be homebuyers could eventually come off the sidelines. New auto sales could comfortably exceed 16 million. And businesses could finally end long-running hiring freezes. Ultimately, many of these developments will depend on the path of 10-year Treasury yields and mortgage rates, but those should follow Fed expectations lower, provided the market gains confidence that the market risks and volatility are fading.

To be clear, such an outcome can only come from a benign inflation scenario. President Donald Trump has advocated for lower rates and unfairly excoriated Fed Chair Jerome Powell for taking a wait-and-see approach. The Wall Street Journal reported Wednesday that Trump was flirting with pre-announcing a Powell replacement to undercut the chair’s sway over markets during the final 11 months of his term. Trump’s campaign against Fed independence doesn’t do the economy any favors. And if market participants come to think that the Fed is cutting for the wrong reasons, 10-year Treasury yields and mortgage rates would certainly move higher — not lower.

To keep my optimist hat on, the market’s other tantalizing possibility is that the artificial intelligence thesis will surprise us yet again. The biggest-single reason that US stocks have shocked the doubters in recent years — from a market returns as well as a fundamentals standpoint — is that Nvidia Corp. blew earnings estimates out of the water. For other stocks including Microsoft Inc. and Meta Platforms Inc., the AI cash flow bonanza is still theoretical.

Could it materialize anytime soon? Hard to say. Even as they invest billions, the titans of Silicon Valley have done their best not to oversell investors on the timeline. On a quarterly call in January, Meta Chief Executive Officer Mark Zuckerberg said that 2024 marked the introduction of some AI products, and this year would be defined by an effort to improve the tools, increase adoption and establish a “durable advantage” among competitors. “But that doesn’t mean that it’s going to be a major contributor to the business this year,” he cautioned. “The improvements to the business are going to be taking the AI methods and applying them to advertising and recommendations and feeds and things like that.” In any case, investors will be reading the tea leaves. If the other AI companies ever manage to break our brains like Nvidia did from 2022-2024, then the entire market is probably underpriced — and there may well be productivity gains in store that could lift the whole economy. (No, I’m not ruling out that this might all end in disappointment, just trying to outline the case for upside.)

Beyond the big macro drivers, there are also a handful of sector-level themes that could deliver. The Fed said Wednesday that it will cut the so-called supplementary leverage ratio, giving banks more flexibility with their balance sheet. Bank analysts are also optimistic about the prospect for mergers under Michelle Bowman, the new vice chair for supervision at the Federal Reserve Board. Large-capitalization health care stocks have been among the biggest underperformers on the S&P 500 this year, despite the exposure through Eli Lilly & Co. to revolutionary GLP-1 obesity drugs. If recent concerns about tariffs and pricing prove overdone, there may be room for recovery.

So sure, it’s a bit scary to see the S&P 500 back at all time highs with so many ostensible risks still on the horizon. For all the delays and pullbacks, average effective tariff rates are still at their highest in around eight decades. With key trade investigations and a “reciprocal tariff” deadline pending, tariffs could conceivably move higher again, and the economy may not absorb their full impacts until businesses finish working through pre-tariff inventory. In geopolitics, Iran Supreme Leader Ayatollah Ali Khamenei delivered an antagonizing address Thursday, in a reminder that the Middle East threat had eased but not vanished. And a report on continuing jobless claims this week put them at the highest since November 2021, showing that hiring remains frustratingly slow, even if layoffs are muted.

The stock market is a risky place, and there are always perils threatening to knock it off course. Yet there’s some room for things to go right, and we may still look back a year from now and realize that this wasn’t such a crazy time to buy some stocks after all.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin