With mortgage rates still near 7%, even relatively wealthy households are choosing to rent rather than buy, and it’s easy to understand why. The combination of high home prices and elevated mortgage rates has hit affordability hard, and inventories are mounting. In the quarters ahead, it’s entirely possible for national home prices to experience modest year-over-year price declines. Sun Belt states may be susceptible to even more jarring re-pricings.

Does this portend a sea change in Americans’ housing preferences or an all-out crash in prices? I highly doubt it. Even if that were remotely true, timing the market is hard and potentially pointless, unless you have the option to live rent-free in your parents’ guest house while you wait. What truly matters is whether home prices stay on an upward trajectory over the medium- and long-term. Provided real estate follows its usual pattern and appreciates in value over time, buying may still deliver the best financial outcomes. And despite all the handwringing, there’s a reasonably strong expert consensus that prices will continue to do just that.

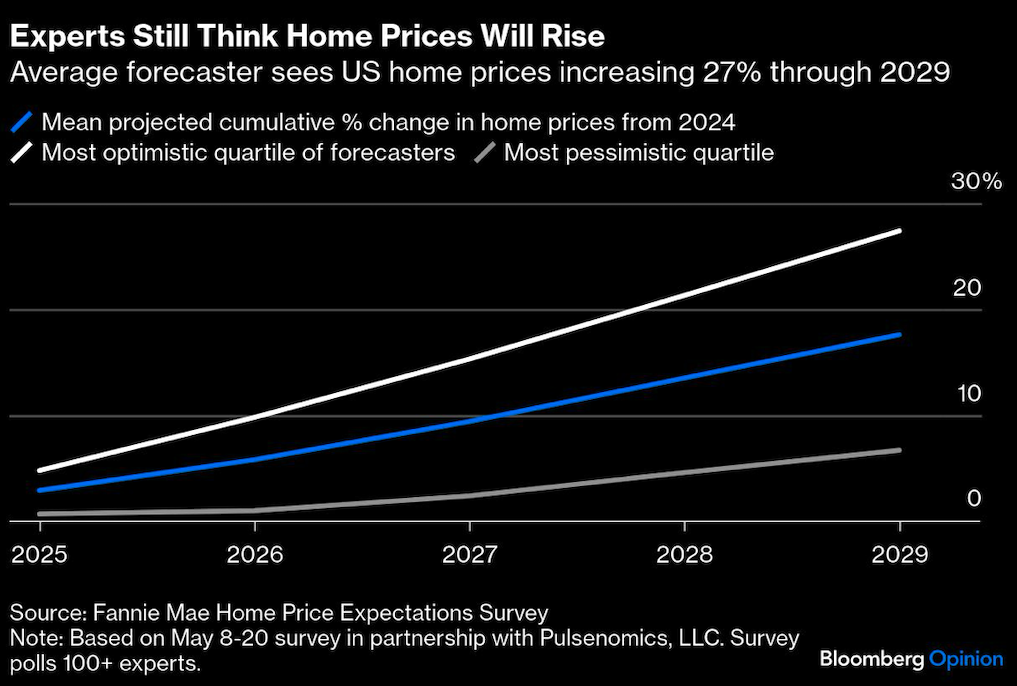

Consider the latest forecasts compiled by Fannie Mae and Pulsenomics. Among professional housing soothsayers, the average expectation was for home prices to increase 17.6% in the five years through the end of 2029 (a 3.3% compound annual growth rate). The most optimistic quartile thinks home values will compound at 5% annually, while the most pessimistic predicts 1.3%. Only two forecasters thought home prices would be lower at the end of 2029 than they are today.

While it feels like the crowd is much more bearish than usual, the panel is nowhere near as pessimistic as it was from 2010-2012 (the latter years of the housing bust), the second quarter of 2020 (in the throes of the pandemic) or early 2023 (after the initial surge in mortgage rates). Today, the implied upside is only a little bit worse than the typical expert outlook. For reference, the realized growth rate over the past quarter century has been about 4.3%.

It’s entirely possible to look at the graphic above and conclude that the “experts” aren’t very good at predicting the future — and fair enough. They stayed bearish too long after the housing bust and completely misjudged the extraordinary buying opportunity in early 2020. In any asset class, longer-term forecasting is a bit of a mug’s game. Even still, it’s clear that the folks who are supposed to know residential housing best are, in the aggregate, fairly unperturbed by the current setup.

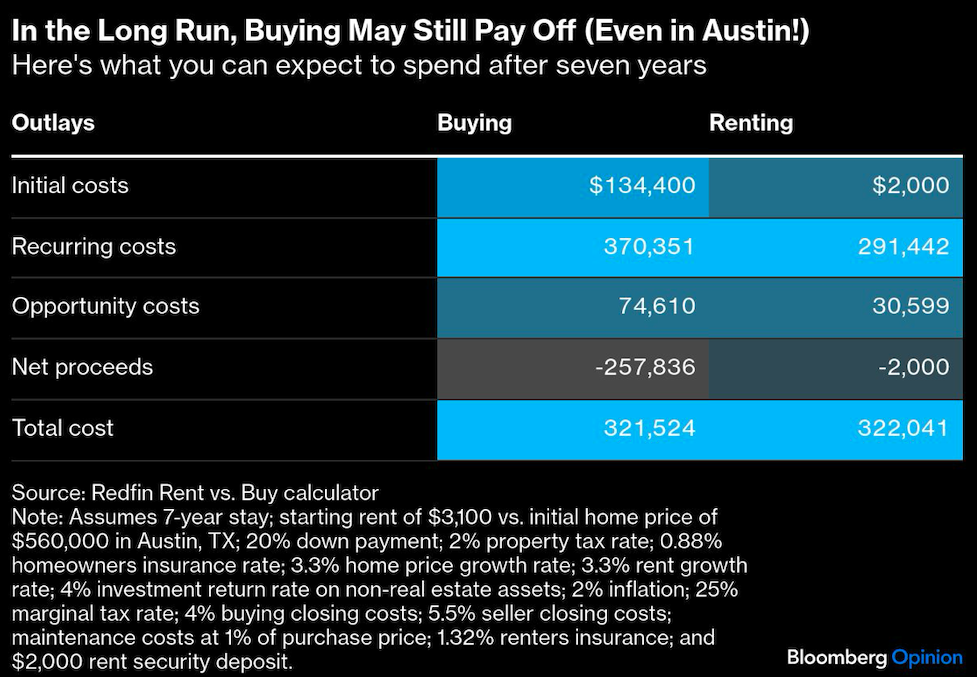

Let’s say you’re new to Austin, Texas, and shopping for a primary residence. A median priced home is running at around $560,000, and you’ll have to pony up something for a deposit (let’s use the classic 20%) and incur upfront fees (appraisals, loan origination, etc.). Even after parting with all that cash, you’ll still be paying around $4,200 a month1 toward a fixed-rated 30-year mortgage payment at the prevailing 6.7%, including typical property taxes and homeowners insurance. You’ll also have to account for maintenance costs, bringing your total monthly outlay up to around $4,700. Ouch! You can rent something similar for $3,100.

But using Redfin’s calculator, buying still ends up being a better deal after about five years if you assume the 3.3% home price appreciation scenario.2 That’s largely because of the capital gains and the tax advantages of homeownership.

Granted, Austin inspires a special degree of bearishness these days. According to Redfin data, the median sale price on single-family homes in the Austin metropolitan area is down about 19% from the highs in 2022. In the Fannie survey, 23% of forecasters thought Austin would “significantly” underperform over the next 12 months, and another 48% thought it would “moderately” underperform.

Of course, we’re focused on the longer run. If we very conservatively assume just 2% compound annual home-price growth in perpetuity, buyers would be waiting around nine years for their investments to pay off versus renting.3 That would be very frustrating indeed, and it’s an interesting thought experiment. But you would have to go back to the housing bubble-and-bust period to find a time when Austin housing delivered such abysmal prospective returns over such a long period. Is that too bearish even for Austin?

I have left out one big factor: opportunity costs. A 20% down payment of $112,000 is cash that you can’t invest in stocks and government bonds. For simplicity’s sake, we can use the Redfin default assumption and say that non-real estate investments will return 4%. In that case, your Austin home purchase would take seven years to become a better deal than renting under the 3.3% base-case scenario for home-price growth.

Some people will disagree with that assumption, saying stock investments or a mixed portfolio of 60% US stocks and 40% government bonds would deliver far higher returns based on the experience of the past 30 years. But if you’re going to make opportunity costs an impediment to buying a home, you have to be brutally honest with yourself: Will you actually put your spare cash toward an ideal portfolio of financial assets, or will you spend it? Similarly, why should you believe that stocks will perform very well in an environment in which housing does not, given that they’re subject to the same macroeconomic forces?

There’s one other detail worth mentioning: the ability to refinance. While it may be crazy to bank on a return to sub-4% mortgage rates, it’s still the case that rates are unusually high by the standards of the past 25 years. Fixed-rate borrowers are protected if rates move higher, but homeowners can pounce if rates make a run at 5%. If that refinancing opportunity materializes in the next two to three years, it can dramatically improve the math for homeownership in a jiffy. The bottom line is that renting isn’t necessarily an obvious move, even in a challenging market like Austin — and under pretty conservative assumptions for prospective home price appreciation. Don’t bank on a rental revolution replacing the American homeownership dream.

Oftentimes, inducements to rent are actually just bearish housing market forecast in disguise. Some buyers may be wagering that home prices in certain markets will dip in the near-term — as they’ve already been doing in Texas and Florida — and that they’ll manage to time the bottom. That’s certainly possible. But housing market timing is devilishly hard in practice, and the risk is that the gamblers end up putting their lives on hold while they wait for the perfect moment to arrive. And it’s far from guaranteed to leave them any better off financially.

1.This is based on outputs using the Redfin calculator. Principal and interest was assumed to be $2,891, property taxes $933 (~2%) and homeowners insurance $411. In practice, taxes will vary based on location and homestead status, among other things.

2. Assumptions: 30-year fixed-rate mortgage at 6.7%; 2% property tax rate; no monthly HOA; homeowners insurance rate of 0.88%; home price growth rate 3.3%; rent growth rate 3.3%; investment return rate on non-real estate assets 0%; expected inflation rate 2%; marginal tax rate 25%; buying closing costs 4%; seller closing costs 5.5%; maintenance costs 1%; renters insurance 1.32%; renter security deposit $2,000.

3. This also depends on what happens with rents. Here I'm using the Redfin calculator again and assuming 2% home price growth coupled with 2% rent growth.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin