Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Private equity has officially conquered the registered investment advisor (RIA) landscape. It is now responsible for a significant portion of RIA-linked M&A activity, as the industry's unprecedented consolidation wave, building on momentum from 2024, reaches new heights in 2025.1 This evolving landscape, with much of the activity focused on firms with demonstrable growth potential, is creating both challenges and opportunities.

The primary opportunity lies in the market's fragmentation and diverse buyer motivations. This creates multiple pathways for successful transactions across different buyer types and target segments.

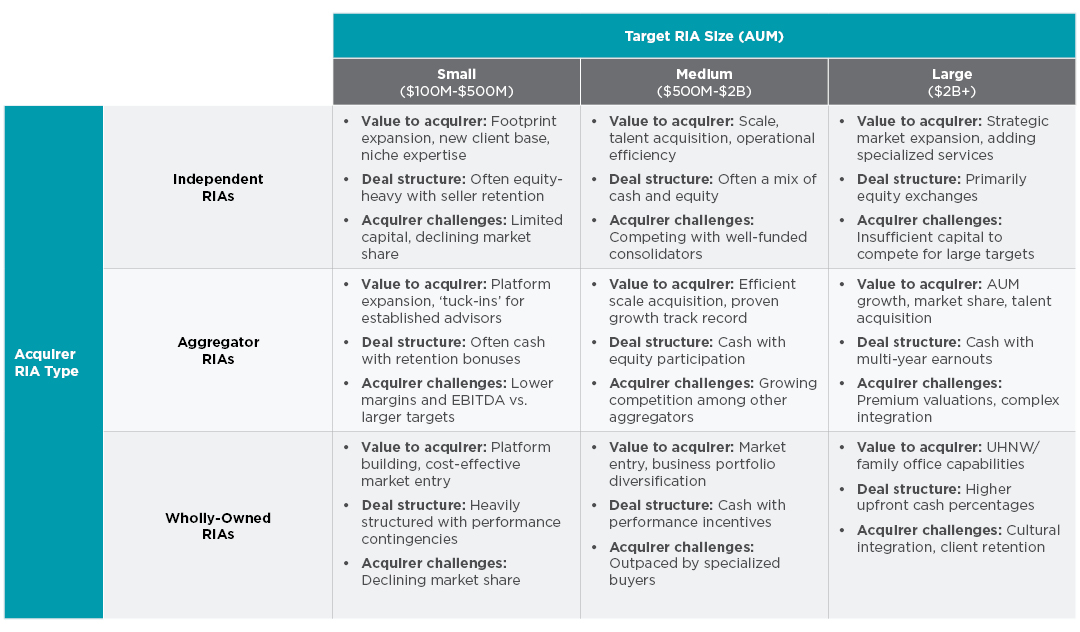

RIA market segmentation

Key challenges are emerging as aggregators face growing integration complexity while managing diverse firm cultures, capital constraints, regulatory differences, and hybrid business models.

Success increasingly depends on buyers developing specialized approaches that align their unique capabilities with appropriate target segments. Accordingly, firms of all sizes continue to aggressively pursue growth through strategic acquisitions:

-

Independent RIAs, including individual advisory firms and smaller regional players, are acquiring other players to enhance organic growth without private equity backing. Independent firms typically focus on culturally aligned targets and favor equity-heavy deal structures with longer-term seller involvement. Despite maintaining steady transaction volume — with 25 deals in 2025 Q1 — independents face significant challenges due to their relatively limited capital resources.2

-

Aggregator RIAs, including RIA networks and platform/service providers, view acquisition as a natural business model. They increasingly target larger firms — with AUM of $1 billion or more — using cash-heavy deal structures with growth incentives and equity participation. Aggregators have accelerated acquisitions as interest rates have dropped. They face ongoing challenges balancing aggressive growth demands from private equity sponsors with complex integrations of diverse firms.

-

Wholly-owned RIAs, including those with direct private equity owners or owned by retail banks and broker/dealers, typically pursue cash-heavy acquisition deals with defined transitions and performance contingencies. These owners can struggle with cultural integration and client retention when institutional ownership replaces high-touch independent advisory relationships.

Tailwinds for the RIA M&A environment

M&A activity among RIAs is expected to remain healthy due to a strong appetite for growth, increasing private equity involvement, and the acquisition of high net worth client segments. Some 75 M&A deals were reported during 2025 Q1, the most active first quarter on record.2

High first-quarter volume was driven by an increasing alignment of M&A goals between buyers and sellers. In recent years, growth has been cited as the top priority for both:

- 65% of sellers listed growth as a primary driver to entering a transaction, followed by liquidity (55%) and succession (49%).

- 85% of buyers ranked growth as the biggest driver, up significantly from 49% in 2022.2

Aggregator RIAs, typically backed by private equity, have surpassed direct RIA buyers to become the dominant buyers in the market, with their market share increasing to 51%.1

It is projected that private equity-backed transactions will continue to be prominent, with 2025 total expected deal volume projected to surpass the 272 volume from 2024.2

In contrast, wholly-owned buyers have pulled away from deal involvement, only accounting for 16% of acquisitions in 2025 Q1.2 Independent RIAs have maintained their strong 2024 momentum, accounting for one-third of deals in 2025 Q1.2

The growing activity among ultra-high net worth and multifamily office firms represents a significant tailwind for RIA M&A activity in 2025. These sophisticated segments were 21% of all transactions in 2025 Q1,2 reflecting their importance as strategic targets that command premium valuations due to their specialized offerings and higher profit margins.

As the needs of ultra-wealthy clients become more complex, these specialized firms provide high-quality acquisition opportunities with the potential to enhance acquirers’ enterprise value.

Headwinds for the RIA M&A environment

RIA buyers must also be wary of headwinds from the current administration’s evolving tariff policies, which have introduced market volatility and valuation uncertainties. The resulting economic unpredictability is forcing RIA buyers to reassess acquisition strategies amid shifts in both capital costs and compliance demands.

Existing and upcoming regulatory and compliance rulings — such as the SEC’s rules regarding the assignment of advisory contracts, marketing rules, and cybersecurity disclosure, along with the FinCEN anti-money laundering mandate — may also complicate M&A considerations.

Approaches to consolidation

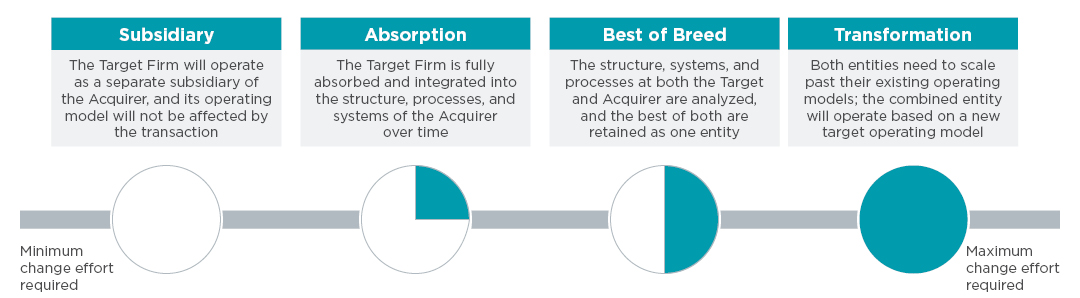

The RIA M&A market is poised for continued robust activity throughout 2025, building on the record-breaking pace established in the first quarter of the year. Acquiring firms must select an integration strategy that balances the need of the target to preserve autonomy with the need for the acquirer to gain integration benefits.

As we outline in the above graphic:

- The Subsidiary approach keeps the target firm operating separately, which is a common strategy for independent RIA buyers who emphasize cultural preservation and autonomy.

-

Absorption integrates the target firm into the acquirer’s structure, and is more common among wholly-owned and aggregator RIA buyers who pursue deeper integration to achieve economies of scale.

-

Best of Breed retains the most effective elements from both firms.

-

Transformation focuses on scaling both entities through a new unified operating model, and is an approach typically seen at later-stage aggregator RIAs.

Looking ahead

Independent RIA buyers will need to focus on strategic niches where their specialized knowledge and cultural fit outweigh financial resource considerations.

Aggregator RIAs will likely continue to gain market share, particularly regarding transactions that involve the most attractive and profitable targets. Their established integration infrastructure and proven processes reduce operational risk and offer economies of scale.

Finally, wholly-owned RIA buyers are likely to become increasingly selective in their approach to the market, as many leverage existing lending relationships or pursue minority investments.

Phil Kerkel is a Partner at Capco. Gregory Feldman is a Managing Principal at Capco. Soumik Chatterjee is a Principal Consultant at Capco.

References

1. Investment News, Record RIA M&A Activity Marks Strong Start to 2025, April 2025, https://www.investmentnews.com/rias/record-ria-ma-activity-marks-strong-start-to-2025/260308

2. DeVoe & Company RIA Deal Book, Q1 2025, https://static1.squarespace.com/static/5410ec1be4b0b9bdbd0cc342/t/680f8b13c929a4531049de85/1745849113348/Q1+2025+DeVoe+Deal+Book_vFINAL.pdf

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Phil Kerkel, Gregory Feldman, Soumik Chatterjee

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.