Futures traders have been unwinding some large bullish bets on Treasury bonds, adding to the recent upward pressure on US yields after a surprisingly strong jobs report last week.

Traders had built up substantial long positions in Treasury markets ahead of Thursday’s payrolls data, anticipating that a weak reading would bolster the case for lower rates.

But since those expectations were quickly confounded, the amount of risk held by futures traders — the open interest — has fallen rapidly over the past couple of sessions. The de-leveraging is putting a profit squeeze on Treasury bulls, with changes concentrated in futures tied to 5- and 10-year notes.

On Thursday, approximately $5 million per basis point of risk was liquidated on contracts tied to the 10-year note. This is roughly equivalent to traders offloading $7 billion of the 10-year Treasuries.

The market came under pressure again Tuesday, as demand for long-term sovereign debt across the globe waned amid concerns that governments are becoming overly reliant on long-dated bonds.

Big Liquidations Seen in US 10-Year Note Futures After Payrolls

“The strong NFP print drove the market to cut expectations of a July rate cut to zero with cheapening driven by long liquidation as recent longs came under pressure,” Citi strategist David Bieber wrote in a note.

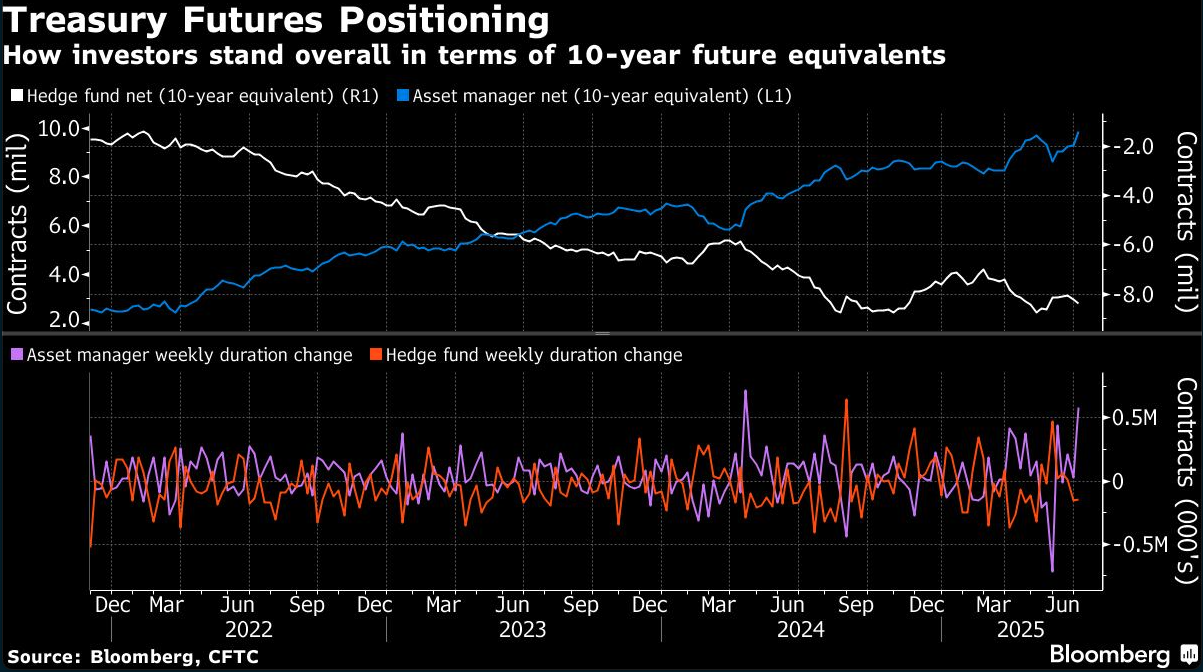

He added, though, that tactical positioning in Treasuries “still remains extended long” with recent bullish bets now in the red. Data released Monday by the Commodity Futures Trading Commission showed a big jump in bullish positioning among asset managers in both 5- and 10-year note futures, which now sit at record-long levels.

Asset Managers 5-, 10-Year Net US Futures Longs Hit Records: CFTC

The upcoming sales of $39 billion in 10-year notes and $22 billion of 30-year bonds on Wednesday and Thursday have the potential to further squeeze Treasury bulls concentrated in long-duration bets, especially if there are any signs of weak demand. Tuesday’s $58 billion 3-year note sale saw a solid reception.

Here’s a rundown of the latest positioning indicators across the rates market:

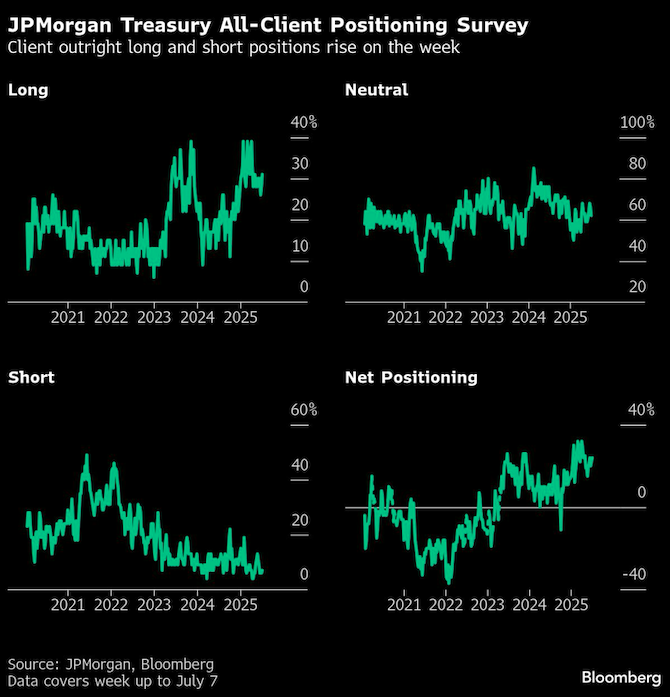

JPMorgan Treasury Client Survey

In the cash market JPMorgan clients extended both long and short positions in the week up to July 7, a survey shows. The net long now sits at the biggest since June 16, although outright short positions are the most elevated in a month.

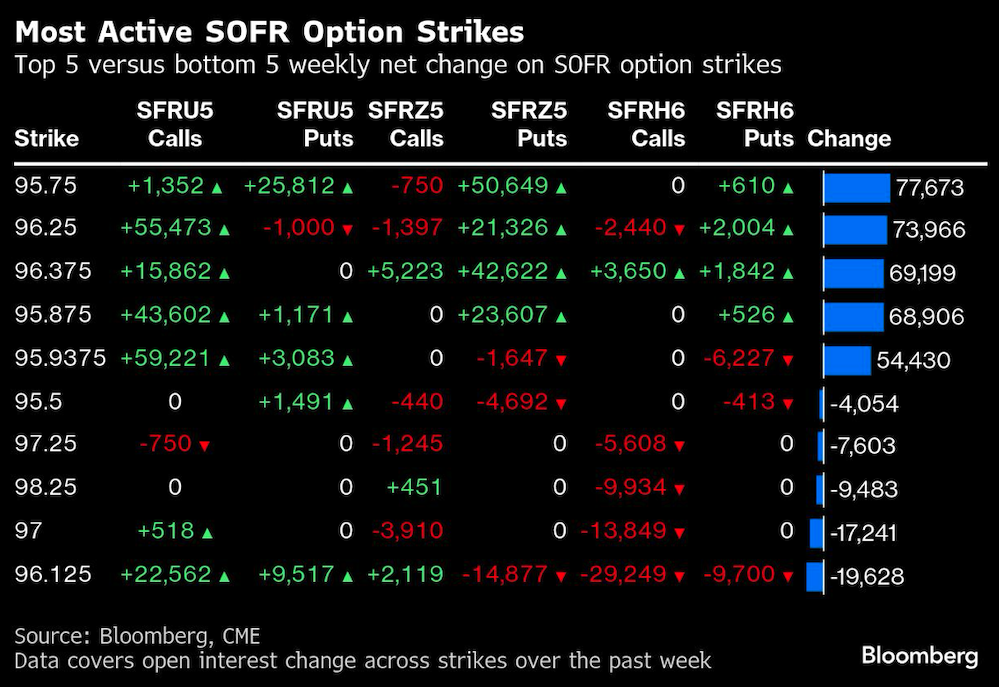

Most Active SOFR Options

In SOFR options out to the March 2026 tenor, one trade has dominated the weekly change in open interest, following heavy buying in the Dec25 96.375/96.25/95.875/95.75 put condor for new risk. The position targets the Fed remaining on hold for the rest of the year, going against the roughly 50 basis points of easing priced in over its four remaining FOMC meetings. There has also been a large buyer of the Sep25 95.875/95.9375/96.00/96.125 call condor, adding to new positioning seen over the past week.

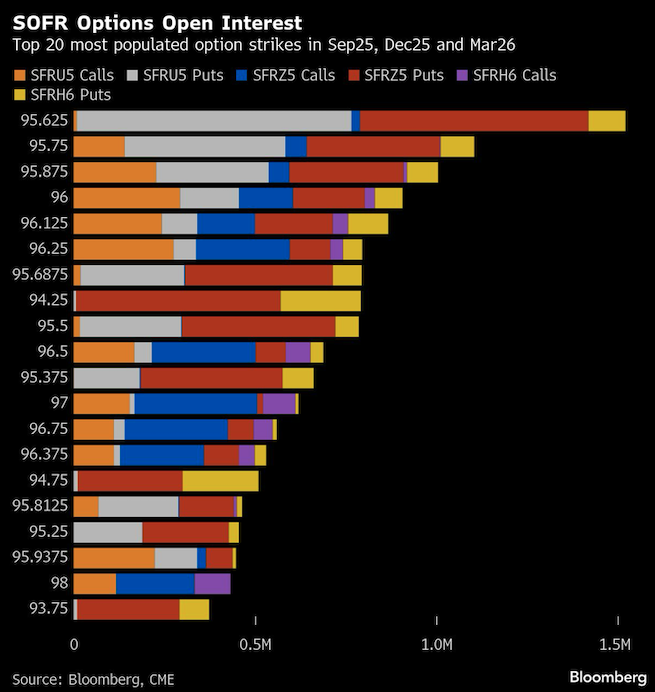

SOFR Options Heatmap

The 95.625 strike remains most popular across Sep25, Dec25 and Mar26 options, with a large amount of risk seen in the level via Sep25 puts and Dec25 puts. Other populated strikes include 95.75 and 95.875, where Sep25 puts are prominent. Recent flows in SOFR have included both upside and downside protection in the aftermath of Thursday’s strong payrolls data.

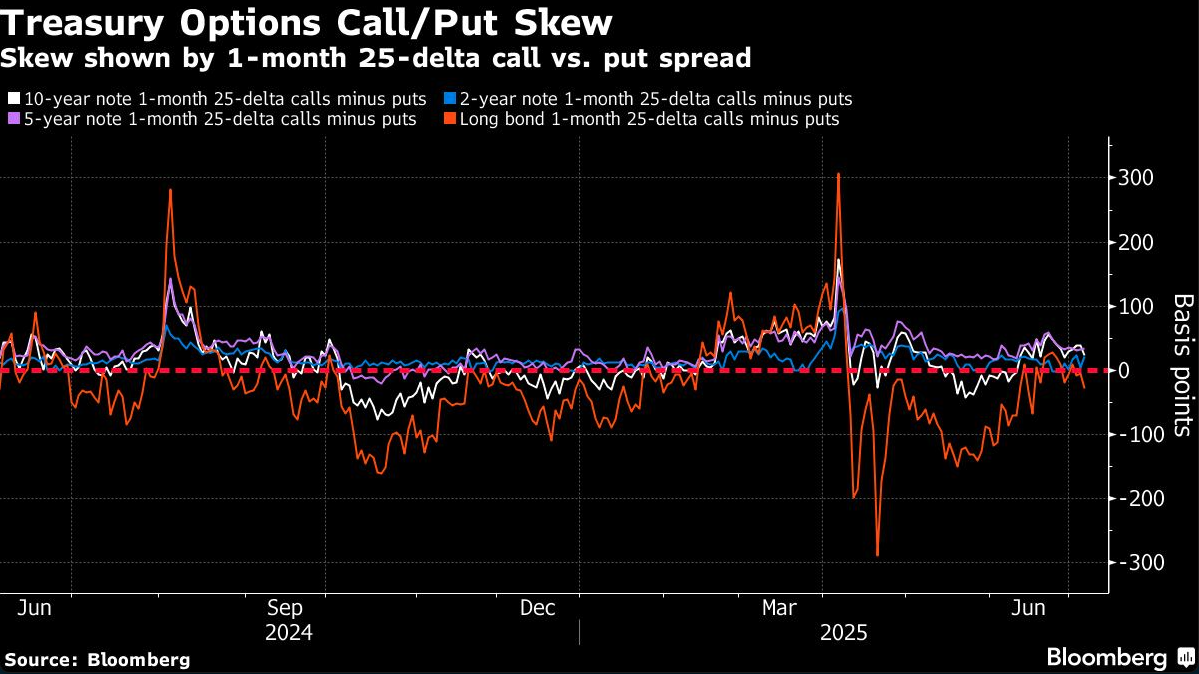

Treasury Options Skew

Following Treasury weakness on Thursday and Monday, skew in the long-end bond futures has moved to favor puts, indicating traders are once again paying a premium to hedge a bond selloff vs. a rally in the long-end of the curve. In Treasury options, recent flows have included an $8 million short vol trade via straddle sales and a $32 million premium options trade targeting a bigger bond market rally.

CFTC Futures Positioning

In the build-up to last week’s payrolls report, asset managers had aggressively ramped-up long positions in Treasury futures, notably in both 5- and 10-year note contracts which hit a record net long amount, along with the ultra 10-year note futures. On the week, shown by CFTC data up to July 1, asset managers extended net duration long by about 582,000 10-year note futures equivalents, the biggest weekly long extension since April 2024. On the flip-side hedge funds added around 148,000 10-year note futures equivalents to net duration short.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.