Global central bankers have ducked a chance to push for tight borrowing constraints on the biggest hedge funds, whose importance to core government bond and other financial markets has grown enormously in the past decade. Such funds are at the center of so-called shadow banking, where the use of borrowed money and derivatives is a troubling source of instability that can hurt not only sophisticated investors, but also the pricing and supply of funding to all areas of the economy.

In a world of ever-expanding public debt and volatile politics, it is imperative that policymakers get their arms around this potential epicenter of the next financial crisis, but they remain frustrated by a lack of data and hampered by the lobbying power of the global asset management industry. Hedge funds, dealer banks and others continue to resist calls for more financial reporting and disclosure. The policymakers at the Financial Stability Board have watered down earlier proposals for greater transparency in favor of working with industry to protect confidential information.

There should be a tradeoff to this: Without the timely detail that would help central banks monitor risks and supervise markets, regulators must impose tougher rules to protect economies.

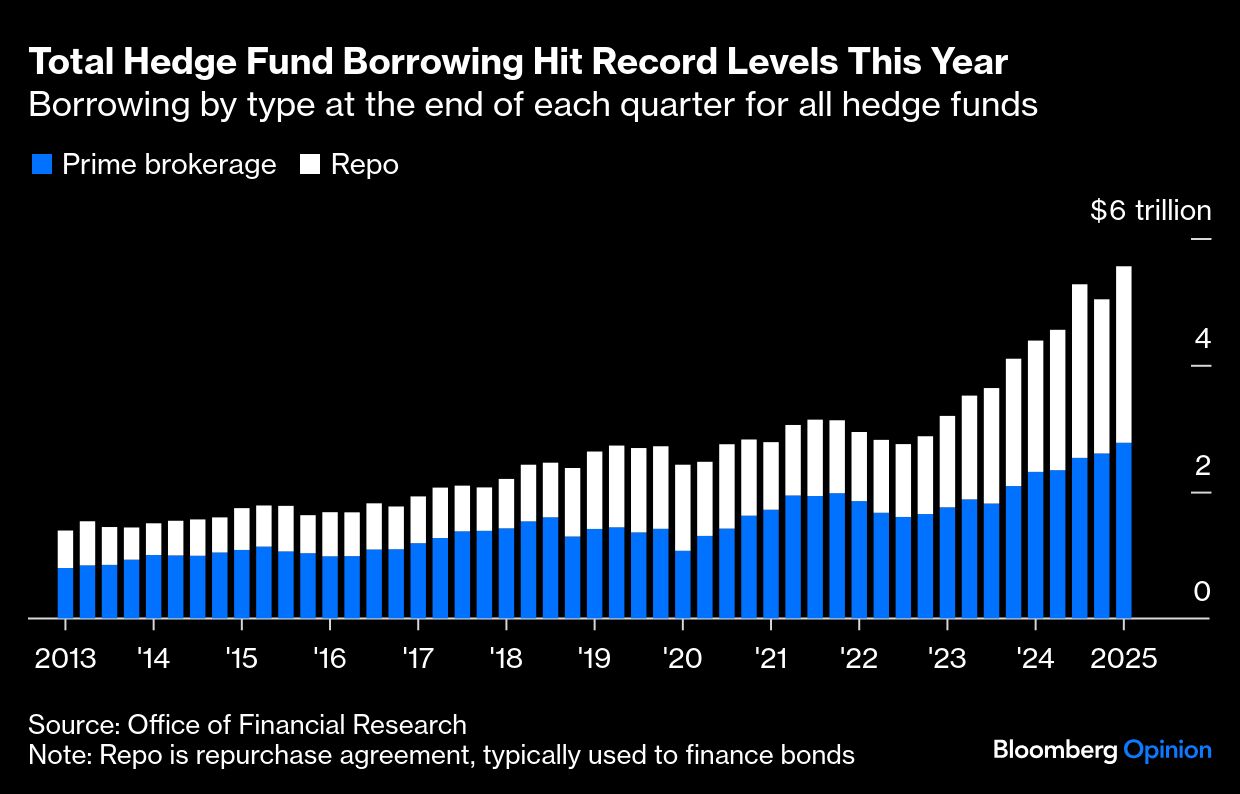

The FSB, which meets in Basel, Switzerland, has been examining the scale and effects of borrowed money across non-bank, market-based finance since several small and large crises between 2020 and 2022 highlighted its power to cause damage. They have dug into vulnerabilities among insurers, pension and mutual funds as well as the hedge funds that are the most dynamic and use the greatest leverage to amplify the impact of their trades. In the US, the total borrowing by hedge funds hit fresh records of more than $5.5 trillion at the end of March.

Also on Wednesday, the Bank of England warned about the risks of hedge funds playing an ever-bigger role in UK gilt markets in its twice-yearly financial stability report. It said that a small number of very big funds accounted for 90% of borrowing to turbocharge their bond trading and that the opaque nature of their activities worsened the threat of destabilizing selloffs.

The FSB’s final report on leverage in non-bank financial intermediation – the technocratic term for shadow banks’ use of borrowed money – published Wednesday, offered a smorgasbord of recommendations from which watchdogs around the world are meant to pick and choose the most relevant, or politically palatable, options.

The FSB hopes that a package of elements can produce safer markets. These include better and more public data to help all investors better assess the risks being taken in markets; more cross-border cooperation between authorities to share information; more centralized clearing of trades and financing; and potentially some limits on the leverage that can be used within certain markets or by certain funds.

However, large, complex hedge funds have successfully campaigned against central bankers relying on firmer borrowing restrictions either on specific trades, or on funds themselves. The final FSB report ends up warning local regulators to be careful with leverage limits to ensure that they avoid losing liquidity or increasing costs in core markets like government bonds.

Regulators face difficulties here because the greater role of hedge funds is a consequence of tougher rules for banks following the 2008 global financial crisis. That forced investment banks to slash leverage and blocked them from making bets on markets with borrowed money.

The US is trying to improve resilience in Treasury markets partly by loosening regulations for banks. Leverage ratio reforms being pushed by Treasury Secretary Scott Bessent should help by giving dealers more balance sheet capacity for low-risk assets like sovereign debt. It will also help them lend more to hedge funds and should make them more able to take up the slack when there is heavy selling by leveraged investors.

The US and other jurisdictions are also pushing more government bond trading and repo financing towards central clearinghouses, which charge borrowers a margin that reduces how much they can borrow. But these moves have faced delays.

Still, leverage limits on big hedge funds should be a key tool for central banks, especially in the US and UK where their role is most significant. A simple limit that doesn’t take account of the riskiness of the assets a fund holds is too blunt and could encourage them to put more money in higher risk bets to maximize returns. Instead what’s needed is a regime of risk-based leverage guardrails, along with rules around how much cash funds should keep aside to meet repayment requests or margin calls on losing trades. This would help ensure their complex, multi-asset and interconnected books of investments are better able to withstand stress without sparking wildfires of losses through markets.

Hedge funds and other asset managers argue that such restraints would treat them like banks, which are funded with deposits and whose failures can create bigger systemic problems than a failing fund ever would. But that’s only half the story. For hedge funds and the broader shadow banking system rely on money market funds to play the role of deposits, supplying short-term cash to finance longer-term bets. This system does suffer bank-like runs on its funding, which lead to credit crunches and real pain for economies, forcing central banks to step in with taxpayer-backed support, as I argued in an April feature.

The idea that better data and monitoring – by central banks and investors and lenders across markets – will offer better defenses against future crises is a hopeful one. It is also a long way from being realized. This year has already seen several troubling selloffs in gilts and Treasuries that central bankers and investors have struggled to understand in real time. The problems exist now. Policymakers need to get a grip.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul J. Davies