Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Should you convert your IRA (or 401k) to a Roth?

We recently wrote an article and built an asset location calculator to help investors think about how to allocate your stock and bond investments between your taxable and non-taxable savings accounts. We’re grateful for the all the feedback we received, but the icing on the cake was an email from our friend and Yale Professor Barry Nalebuff, sharing his thoughts on why he converted his Traditional IRA to a Roth account. It’s a topic we had been planning to write about, but Barry’s treatment was so clear and insightful that we decided, with his permission, to share it with our readers pretty much as it came to us in his email.

Barry is a thinker worth listening to. We’ve thoroughly enjoyed reading several of his books, which we highly recommend: The Art of Strategy: A Game Theorist’s Guide to Success in Business and Life (with Avinash Dixit), Lifecycle Investing: A New, Safe, and Audacious Way to Improve the Performance of Your Retirement Portfolio (with Ian Ayres)1 and Split the Pie: A Radical New Way to Negotiate. Barry and Ian’s recommendation that young investors should be leveraged investors in stocks to avail themselves of time diversification has received much attention in the press lately. Barry is also well-known for co-founding Honest Tea with Seth Goldman, one of his Yale students. Their newest beverage is “Just Ice Tea” which tastes equally great.

A few basics about converting your Traditional IRA or 401k to a Roth structure

Converting a Traditional IRA to a Roth IRA – commonly called a “Roth conversion” – is a process that allows you to move retirement savings from a tax-deferred account (traditional IRA) to a tax-free account (Roth IRA). In this article, we’ll discuss IRA conversions, though the same analysis applies to the conversion of a 401k.

Anyone can convert a traditional IRA to a Roth IRA; there are no income limits for conversions. When you convert, the amount you move from your traditional IRA to your Roth IRA is treated as taxable income for that year. Once in the Roth IRA, your money grows tax-free, and qualified withdrawals are income tax-free. Distributions from a Traditional IRA account are taxable and that’s why they are called ‘tax-deferred,’ whereas Roth IRAs are referred to as “tax-free.”

We asked some of our AI friends how to think about the Roth conversion, and it seems the conventional thinking is that if you expect your tax rate in the future to be the same or lower than your tax rate today, you shouldn’t do the conversion. The AIs seem to be making assumptions about growth rates and tax rates and comparing whether $100 in the Traditional IRA or an equivalent post-tax amount in the Roth IRA will result in more post-tax wealth to some horizon.

Barry thinks that’s not the full-credit answer, and we agree. Over to Barry…

Barry’s reasons for converting to a Roth IRA2

Dear Victor…here are the thoughts behind my decision to convert everything to a Roth IRA:

Reason 1:

Converting to a Roth IRA effectively made my IRA more than 50% bigger! The trick is that one is allowed to pay for the taxes associated with the conversion with funds outside the IRA.

Take the case of a $1M Traditional IRA that gets converted and let the person be paying 32% Federal and 6% state taxes, so they owe $380K in taxes. The original after-tax size of the IRA was $620K – now it’s $1M after tax, and the IRA is now more than 50% larger. (If the person is at the 37% Federal bracket and 6% state, then the IRA value grows from $570K to $1M or by 75%!)

The taxes one is paying with money outside the IRA is just like adding to the IRA. The $380K paid in taxes is, in effect, invested in the IRA. Having a $1M Roth IRA is 50% (or $380K) better than having a $1M regular IRA. This allows wealthy people3 to contribute a whole lot more money to fund their IRA.

The value of this is:

τ 1 * τ 2 * Size of IRA * growth

where τ 1 is the income tax rate, τ 2 is the capital gains tax rate and growth is expressed as a gain, so equals 1 if the portfolio doubles in value. The reason is that the extra amount in the IRA is the income taxes paid (τ 1 *Size of IRA) and the savings is the elimination of capital gains taxes on the growth (τ 2*growth).4

Thus, if the person’s income tax rate stays constant at 43% (federal plus state) and the capital gains rate stay constant at 30.8% (federal plus state), then the gain is 0.43 ∗ 0.308 ∗ $1M ∗ growth = $132,000 ∗ growth. If the investments in the IRA double, i.e. growth = 100%, then the after-tax gain is $132,000. If they triple, then the gain is $264,000. Real money.

Reason 2:

The Roth IRA has no RMD (Required Minimum Distribution). Thus, one gains the advantage of being able to leave money in the IRA longer. This is also true for an inherited IRA, where the beneficiaries get to keep all the funds in the Roth for ten years rather than have to withdraw evenly over ten years. This effectively doubles the investment period.

Reason 3:

In my case, my 91-year-old mom is living in Florida which has no state income tax, but the beneficiaries of her IRA live in NY and CT. Thus, she will pay 6% or 7% lower taxes on the conversion than they’ll pay when taking the distributions.

So why don’t more (wealthy) people do this?

One bad answer is that people would rather see an IRA with $5M in assets than a Roth with $3M. They feel less rich. I think one has to look at one’s after-tax wealth.

Another bad answer is that they think it is a mistake to pre-pay taxes because they then lose the ability to invest the amount they paid in taxes. That is true in the case of a stock with capital gains, but that’s a mistake in the case of a Roth conversion. Consider the case where the person pays the taxes using the money inside the IRA.

Case 1: No conversion. They end up with

S * (1 + G) * (1 — τ)

where S is initial amount, 1 + G is the growth, and τ is the tax rate.

Case 2: Conversion. They end up with

(1 — τ) * S * (1 + G)

…it makes no difference if one pre-multiplies or post-multiplies by (1 - τ ). Assuming the tax rate will be the same at the time of the Roth conversion and at the time of the IRA distributions, the financial results will be 100% identical if the conversion taxes are paid using funds from inside the IRA.

And now you can see the benefits of using funds from outside the IRA. Imagine the person first pays the taxes using funds from inside (which creates the wash) and then replenishes the Roth with a contribution of the tax amount. This effectively expands the IRA by the size of the taxes. Thus, on the tax amount (τ 1*S), the person gains by not having to pay taxes on the growth, which is a savings of τ 2*G. And, while one can’t pay the taxes using money inside the IRA and then replenish, if one pays the taxes using funds outside the IRA it has the very same effect.

– Barry Nalebuff

Additional Factors to Consider

We love Professor Nalebuff’s analysis. For completeness, we’ll add a few more considerations to the primary ones he addressed so clearly:

Tax rates: It is useful to build in potentially different tax rates on ordinary income today and in the future.

Tax rate risk: The Roth conversion reduces your tax risk in two ways. First, it reduces your risk to changes in tax rates in the future. Tax rates on ordinary income can change over time, both due to changes in tax policy and from changes in personal circumstances shifting your tax bracket. Secondly, savings in taxable accounts are subject to the asymmetric treatment of capitals gains and losses – we are taxed on gains, but with losses we don’t get a tax payment from the government, we just have a loss carry-forward which we hope we can use against gains in the future. Neither of these are huge effects, but they are not de minimis either.

Returns risk: The benefit of the Roth conversion increases the more your portfolio grows. Because the benefit is so aligned with investment returns, the risk-adjusted value of the conversion will be less than the expected value.

Time: The choice to convert from Traditional to Roth is not a “now or never” choice – you could convert next year, or five years from now instead of this year, or partially convert on some schedule over time. If converting today would generate significant value, but next year you expect to be tax-resident in Florida instead of New York, waiting to convert will almost certainly generate even more value. As an example: if you have a 30-year total horizon but expect a lower income tax rate in five years, you need a 3% lower tax rate to make waiting worthwhile.5

Realized gains: When you convert, you may have to realize gains in your taxable account earlier than you otherwise would, to raise the funds to pay the taxes owed on conversion. This is a small effect for normal situations, but it could become more material in the case of large, realized gains and a very low or zero horizon gains rate.6

Modeling and Sensitivities

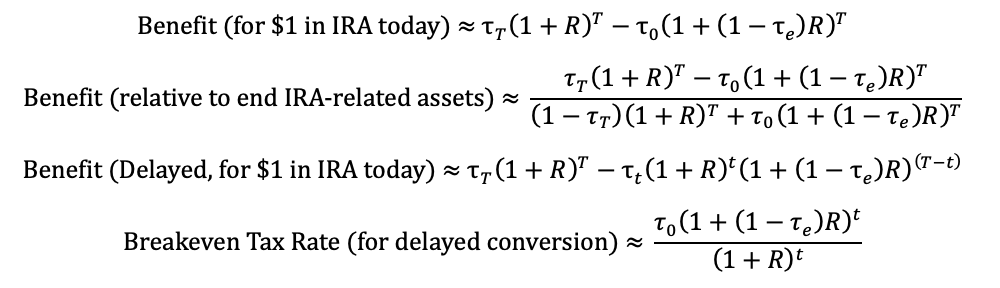

The comprehensive way to incorporate the factors above is to value the conversion benefit as the change in your expected utility under uncertain investment return and tax-rates. Keeping with the spirit of Barry’s email to us, we’ve found that a simple approximation for the benefit of immediate conversion produces an estimate very close to the full procedure. You can find the formula for this approximation in the Appendix.

We’ve built a new Roth Conversion Calculator which does this analysis, as well as providing sensitivities to all the inputs, and have used it to provide the numbers in the example which follows.

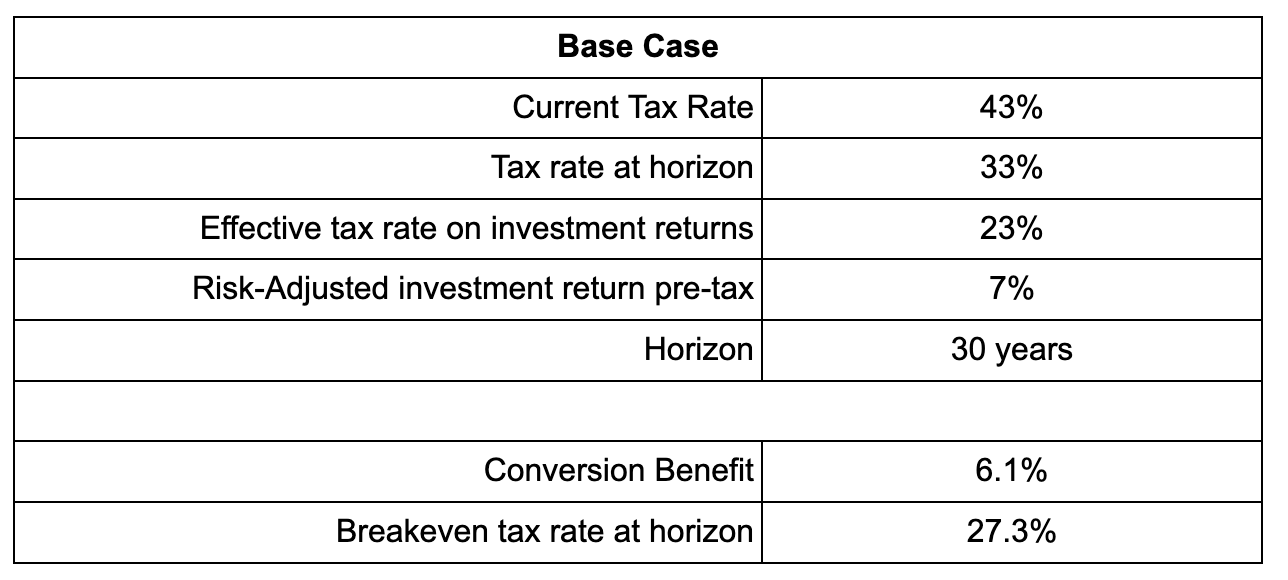

A Concrete Example

Let’s say you are currently subject to a 43% marginal income tax rate as you are a high earner living in a high-tax state. We agree with Barry that many wealthy people shouldn’t expect to be subject to lower marginal tax rates in the distant future, but we want to work through an example with a lower future tax rate. So, let’s assume that you expect to be subject to a 33% tax rate in your later years, as moving to a low-tax state and perhaps having income in a lower bracket will outweigh higher expected Federal tax rates. We’ll assume that you expect your effective tax rate on investment income in your taxable pool of savings will be 23%, and we’re going to zoom in on only that portion of your wealth affected by the conversion choice, which is your Traditional IRA plus the amount you need to pay in conversion taxes – we’ll call this your “conversion wealth.” Then, to a 30-year horizon and with a 7% pre-tax risk-adjusted return on your investments, the Roth conversion results in 6.1% more after-tax, risk-adjusted wealth than you’d otherwise have at the horizon from your conversion wealth. The break-even future tax rate at which the conversion adds no value is 27.3%, a drop in your current tax rate of 15.7%.

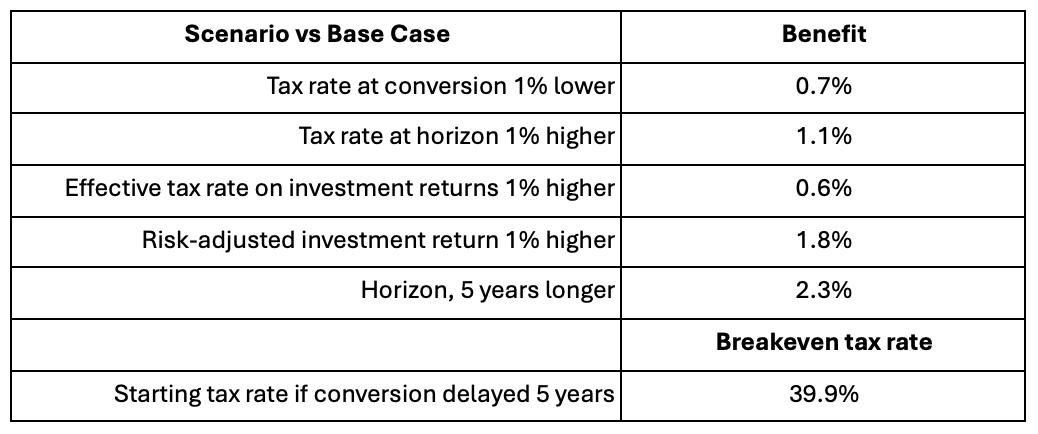

In the table below, we show sensitivities to all the inputs, and we also provide the breakeven tax rate (a drop of 3.1%) at time of conversion that makes waiting five years to convert as attractive as converting today.

The above analysis leaves out many factors mentioned in early sections of this note. Almost all of the non-modeled considerations – such as no Required Minimum Distributions (RMD), reduction in tax risk, benefits from intergenerational perspective – point in the direction of doing the Roth conversion. Roth IRAs having no RMDs is perhaps the most significant of these effects. A 65-year-old investor can expect to roughly double the tax-free investing period in her IRA in Roth versus Traditional form.

Connecting the dots

As of 2022, about 10% of assets in IRAs in the US were in Roth form. This is pretty close to our experience at Elm Wealth, where we manage about 100 IRA and 401k accounts on behalf of our roughly 600 clients, with about 10% of these in Roth form. The majority of our clients have sufficient assets outside their retirement accounts to be able to pay the tax on the conversion with those funds.

We suspect that for many of our clients, converting to a Roth will make sense, either today or in the near future. We hope this note and our calculator will encourage many of you – our clients and readers – to give the conversion decision another look. Victor is looking forward to going over this with one client in particular – his 91-year-old mother – who he hopes will follow in the footsteps of Barry’s mother in doing the conversion!

Finally, please consult a tax expert on this important decision. The purpose of this note was to give you lots of questions to ask!

Elm Resources

Appendix

where τ0 your current income tax rate, τT is the expected income tax rate at horizon T, R is the risk-adjusted return of your investment portfolio, and τe the effective tax rate on your taxable portfolio. R and τe will primarily depend on your portfolio expected risk and returns, your coefficient of risk aversion, personal tax rates, and horizon. t is how many years you delay conversion from the present time.

Endnotes

1 If you can’t get your hands on a hard copy of this book, we suggest you read their 2008 article, “Life-Cycle Investing and Leverage: Buying Stock on Margin Can Reduce Retirement Risk,” on SSRN and NBER.

2 Lightly edited by Elm.

3 Specifically, you must have enough wealth outside your IRA to fund the taxes on the conversion.

4 From VH & JW: Barry’s analysis here holds exactly assuming current and future tax rates on ordinary income and the effective tax rate on investment remain constant.

5 We flesh this out in more detail below.

6 For example, with the expectation of contributing appreciated assets to charity, or receiving step-up basis on death.

This is not an offer or solicitation to invest, nor are we tax experts and nothing herein should be construed as tax advice. Past returns are not indicative of future performance.

This article is based on an email exchange with Yale Professor Barry Nalebuff in which he shared his insightful analysis of the Roth IRA conversion decision. Thanks also to our friend Larry Hilibrand, as well as our colleague Jerry Bell, for sharing their comments on this article, and to ChatGPT for encouraging us to share this comprehensive analysis by sharing its not-so-comprehensive analysis with us.

Victor Haghani is founder & CIO of Elm Wealth, a Philadelphia-based asset manager. James White is Elm Wealth’s CEO.

Learn more at www.elmwealth.com.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Victor Haghani, James White

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.