After it emerged from the rubble of Lehman Brothers, Trilantic Capital Partners exemplified the success of private equity’s vast middle market for more than a decade.

Profitable bets on energy companies and consumer names like Traeger Pellet Grills bolstered its reputation as low interest rates fueled a boom across the industry. In 2019, investor appetite was so plentiful that Trilantic hit the upper limit of money it was willing to accept for the sixth iteration of its flagship fund.

But these days, the firm is one of many that reflect shifting fortunes. It collected one-sixth of its target for Fund VII, and is now focused on raising $1 billion for a different aim: buying more time for Fund VI. That multi-asset continuation fund is being pitched at a steep discount of 30% of the current asset values, according to people with knowledge of the discussions.

Trilantic, which manages about $8 billion, declined to comment. Evercore Inc., the adviser on the transaction, didn’t return requests for comment.

Midsize private equity firms are getting hit particularly hard by the industry’s vicious cycle — firms aren’t finding the price they want for businesses they own, so their clients aren’t getting money back to invest in the next round of funds. The industry’s giants, including KKR & Co. and Apollo Global Management Inc., used the boom times to branch out into new businesses like private credit, infrastructure and insurance.

Smaller firms have no such refuge.

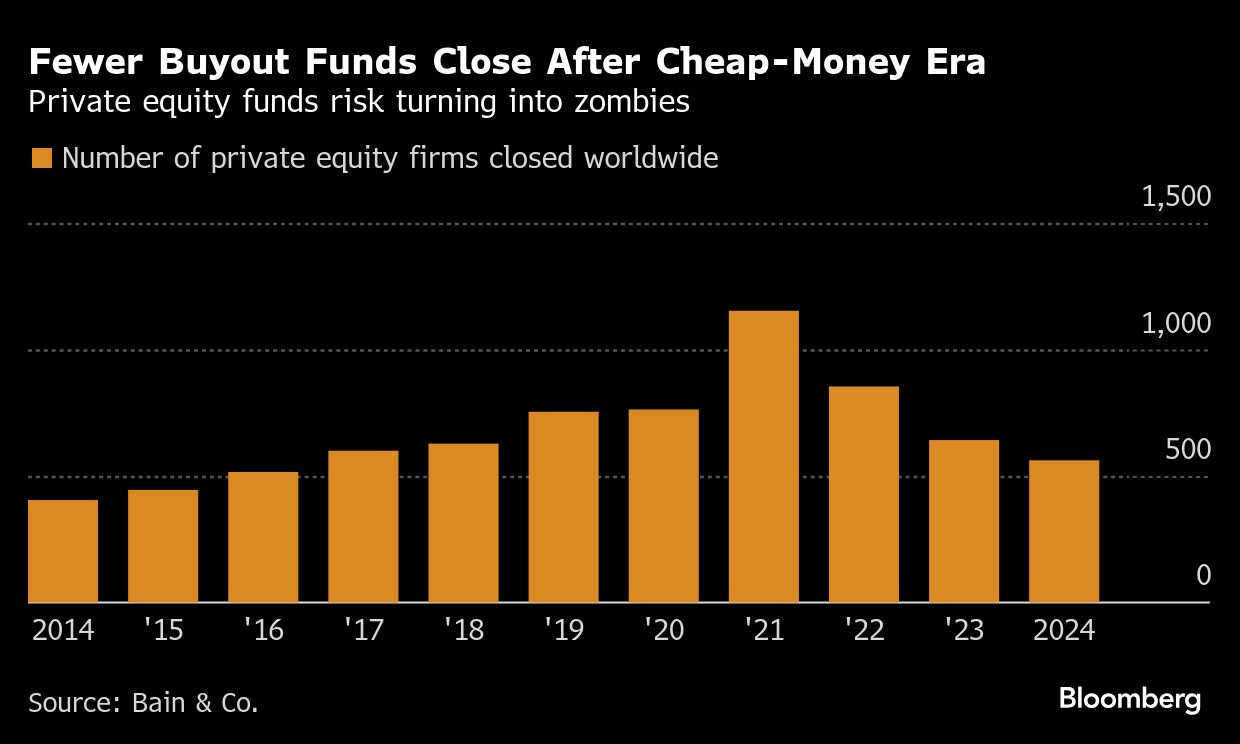

Buyout firms almost never collapse. Instead, they risk turning into so-called zombie firms, with a reduced staff trying to shepherd a shrinking pile of existing investments rather than chasing the next big deals with fresh money. That threat is growing since more than 18,000 private capital funds worldwide are now soliciting investor cash, according to a Bain & Co. report released in June. Collectively, they’re seeking $3.3 trillion, translating into $3 of demand for every $1 of supply.

And as the deal drought continues, Trilantic and many others — including Onex Partners, Crestview Partners, Vestar Capital Partners and Madison Dearborn Partners — are either pausing efforts, missing targets or scaling back on new fundraises.

Some midmarket shops — which typically raise funds ranging from $500 million to $2.5 billion, according to Bain — are also turning to the secondary market for more time to prove themselves on their current bets.

Certain firms of this size “weren’t structured right to handle this moment,” said Andrea Auerbach, global head of private investments at Cambridge Associates.

Missed Target

Trilantic’s fundraising stalled after the Federal Reserve started raising interest rates in March 2022. The firm collected $516 million for its last round of fundraising, giving up on a $3 billion target and closing the round early. At least 10 dealmakers have left since 2023, a significant portion of a workforce that employs fewer than 50 people, according to its website.

The firm stopped making new energy bets following the defection of some staff, and in 2023 it shuttered its special situations unit. Trilantic has exited only two holdings in the past couple of years: residential property management platform Asset Living and artificial intelligence consultancy Hakkoda.

With the continuation fund, Trilantic hopes to raise $1 billion for about 19 assets from its 2017 vintage Trilantic Capital Partners VI North America fund, the people said. The net asset value of Fund VI is about $3.4 billion.

Several large secondary buyers have conducted due diligence on the deal, and if the process goes through as planned, it could close in the third or fourth quarter, the people said.

Not every midsize firm is feeling the pain. Those that specialize in certain industries and use relatively little leverage have tended to perform better than those that don’t.

In June, the largest pension in the US — California Public Employees’ Retirement System — reported that its performance had improved significantly since the fund recomposed its buyout portfolio from mostly mega-size to more middle-market firms three years ago. Calpers achieved the highest private equity return among its peers in 2024, up from 17th out of 30 in 2022.

Recognize Partners, which invests exclusively in technology-services companies, raised $1.7 billion for its second fund, 27% more than its prior fundraise. Levine Leichtman Capital Partners wrapped up its latest fund with $3.8 billion, making it about 150% larger than its prior iteration.

Others are raising smaller pools of capital compared to their prior funds.

Chicago-based Madison Dearborn has outperformed the private equity industry in 13 of the past 15 years and distributes $2 for every $1 invested, it told investors in a letter. Still, it scaled back its latest fund and is seeking the smallest pool of capital since 1999.

Meanwhile, UK-based Mayfair Equity Partners raised £500 million ($675 million) for its latest fund, less than the £650 million fund it wrapped up the predecessor with in 2019. Paris-based Astorg closed its latest fund at €4.4 billion, about €2 billion short of what it had targeted.

The list goes on: Vestar paused its fundraising plans, and in 2023 Toronto-based Onex halted fundraising for its flagship private equity fund. Crestview also put fundraising on hold. That firm generated $1 billion from two exits earlier this year and opted to focus on investing that money rather than gathering new cash, according to a person familiar with the matter.

High Stakes

Fundraising isn’t Trilantic’s only challenge. In early 2022, Christopher R. Manning, its then-managing partner, spun out to launch Greenbelt Capital Management, an energy-focused midmarket private equity firm, and took several executives with him.

In addition to its entire energy team, Trilantic lost seven senior executives in the past two years. Among them: Grant Palmer, partner, who left the firm in July 2023 and Daniel Siegman, another partner, who exited in June. Investor relations head Kristin DePlatchett departed in February. Several managing directors also left in recent months.

The individuals who exited either didn’t return requests for comment or declined to comment.

Other middle-market firms are also seeking lifelines in the secondary market. Crestview, Madison Dearborn and Vestar raised hundreds of millions of dollars between them to hold on to some assets from older funds. More midmarket firms are expected to follow suit.

Like most continuation funds led by private equity firms, the Trilantic one has a so-called staple provision requiring investors in secondaries vehicles to back a new fund — stapling one commitment to another.

Typically, the staple is $1 for the flagship fund for every $2.5 or $3 committed to the continuation fund. Trilantic only requires fund investors to pledge $1 for every $5 committed to the continuation fund, reflecting backers’ concerns over the firm’s ability to raise new money, the people said.

Trilantic’s deal terms could change, as could the amount raised for the continuation fund in the final stretch of negotiations.

For Trilantic’s leadership, the stakes are high. They’ll need to demonstrate performance, find exits for those companies and return profits to their new investors through the six-year life of the continuation fund, the people said. Trilantic will also have to retain its remaining key talent.

“The onus is on midmarket firms to prove they can win,” said Hugh MacArthur, chairman of the global private equity practice at Bain.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Preeti Singh, Laura Benitez