“The size, scale and scope of JPMorgan Chase also offer huge advantages,” Jamie Dimon wrote in a letter to shareholders — his first as chief executive officer at the end of 2005. Two decades later, the claim seems almost quaint. The bank’s balance sheet is now four times larger; its stock market capitalization has ballooned by more than five times; and profit this year is forecast to be nearly seven times higher than then.

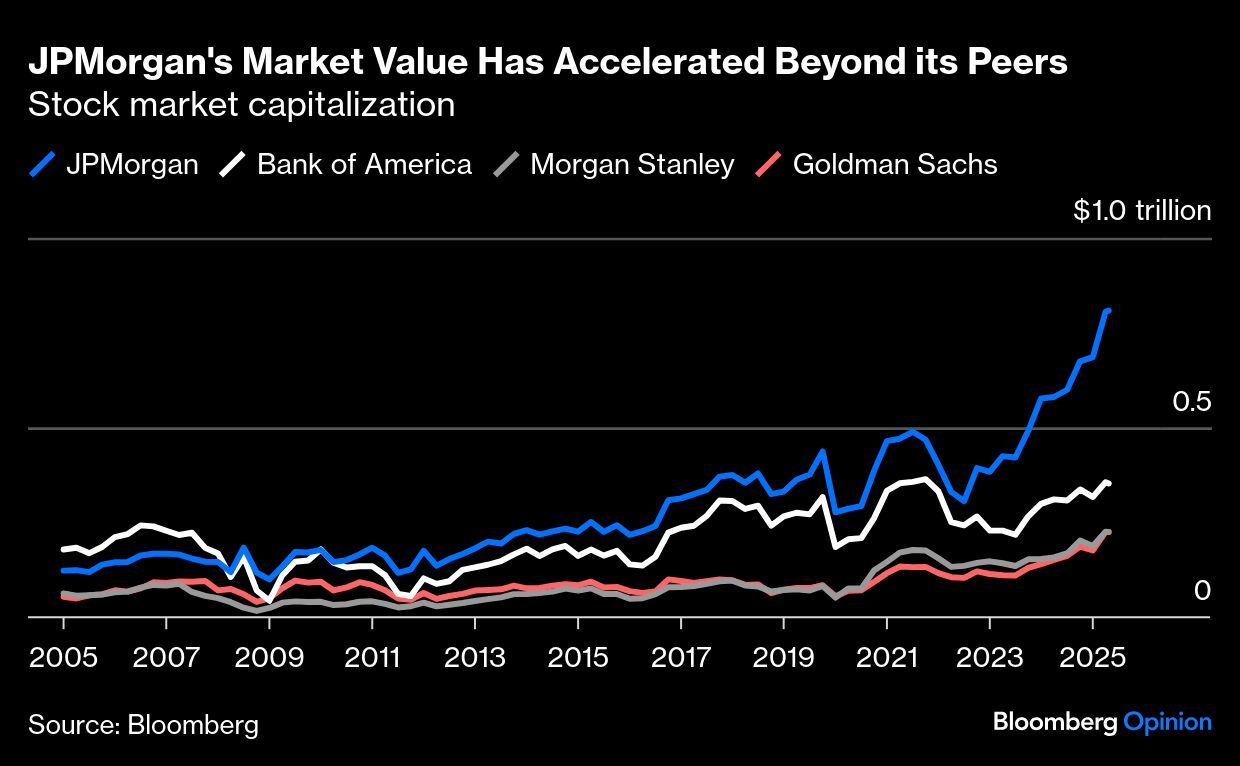

JPMorgan Chase & Co. has left the competition behind, even its biggest and most consistent peers including Bank of America Corp., Goldman Sachs Group Inc. and Morgan Stanley. At more than $800 billion, the bank is now worth as much as these three combined.

Can it keep winning? And is it too big? These are related questions. To find growth that doesn’t make the bank more of a risk to itself and the economy it inhabits, it has to be very well run. But its immediate problem is an extremely high stock valuation and billions of dollars of excess capital – both of which threaten its returns if mishandled. Size alone “is not enough to win,” Dimon wrote two decades ago. “In fact, if not properly managed, it can bring many negatives.”

The big bumps JPMorgan has ridden along the way are memorable because they’ve been relatively scarce: The so-called London Whale trading losses in 2012 and the more recent acquisition of what turned out to be a fraudulent fintech, Frank, stick out. But when Dimon wrote his first shareholder reviews for 2005 and 2006, JPMorgan was producing less-than-stellar results. The new CEO was being criticized for too much caution in a credit and trading boom that delivered huge profit for its rivals, some of which were making returns on equity of 30% or more while JPMorgan languished at 20% or below.

Its strict limiting of subprime mortgages and trendy off-balance-sheet vehicles for investing in complex bonds appeared very conservative to shareholders and rivals at the time. But by early 2008 – when Dimon first coined his “fortress balance sheet” catchphrase – those choices instead looked like some of the smartest made on Wall Street.

Dimon’s strength has always been a patient, paranoid and honest approach to risk – and an ability to course correct when things don’t work out. His early missives insisted that the bank would never pursue short-term wins at the cost of longer-term value (similar phrases were repeated at this year’s investor day). They were also refreshingly simple and clear – and when it comes to running any organization, nothing beats clarity of communication.

For example, in breaking down possible losses from various risks in 2006, he wrote: “It’s important to share these numbers with you, not to worry you, but to be as transparent as possible about the potential impacts … We do not know exactly what will occur or when, but we do know that bad things happen.”

The aim, then and now, is to be well prepared for “bad things” and ready to take advantage when rivals cannot. After 2008, for instance, JPMorgan made a fortune hoovering up senior bonds issued by collateralized loan obligations, a type of structured credit vehicle, that many banks were ditching at huge discounts.

Patience and adaptability not only help to avoid taking big hits or reacting appropriately when they do happen; they also encourage correcting for missed opportunities. Dimon has been a colorful critic of cryptocurrencies, calling the industry a Ponzi scheme. But JPMorgan has built an internal payments “coin” that’s been adapted as a tokenized deposit, just in time to help defend it against the coming wave of stablecoins under new US regulations. It may also start making loans to customers against crypto asset collateral, the Financial Times reported.

It has a catch-up strategy in private credit, too. If the best time to commit to the market could have been in 2015 when it let go of HPS Investment Partners, recently acquired by BlackRock Inc., then the second-best time is now, when the excesses are easier to spot and the diversity of borrowers is improving.

This reflexive, adaptive strategy has always been there, but Dimon formalized it for investors in 2023 with reference to the military practice of the OODA loop: Observe, Orient (analyze and check your assumptions or biases), Decide and Act – then observe and repeat. None of this is unique: The hard part is doing it properly and persistently. If Dimon has successfully instilled this practice throughout executives and management, then this vast bank will survive his inevitable retirement, as I’ve written before.

That’s a theory many investors still aren’t keen to test. But it will be tested – and perhaps even before Dimon steps down. JPMorgan has roughly $60 billion of equity capital more than it needs to meet regulatory requirements. It is expected to spend about one-quarter of that on share buybacks over the rest of this year, having already repurchased about $15 billion of stock so far in 2025, according to figures compiled by Bloomberg.

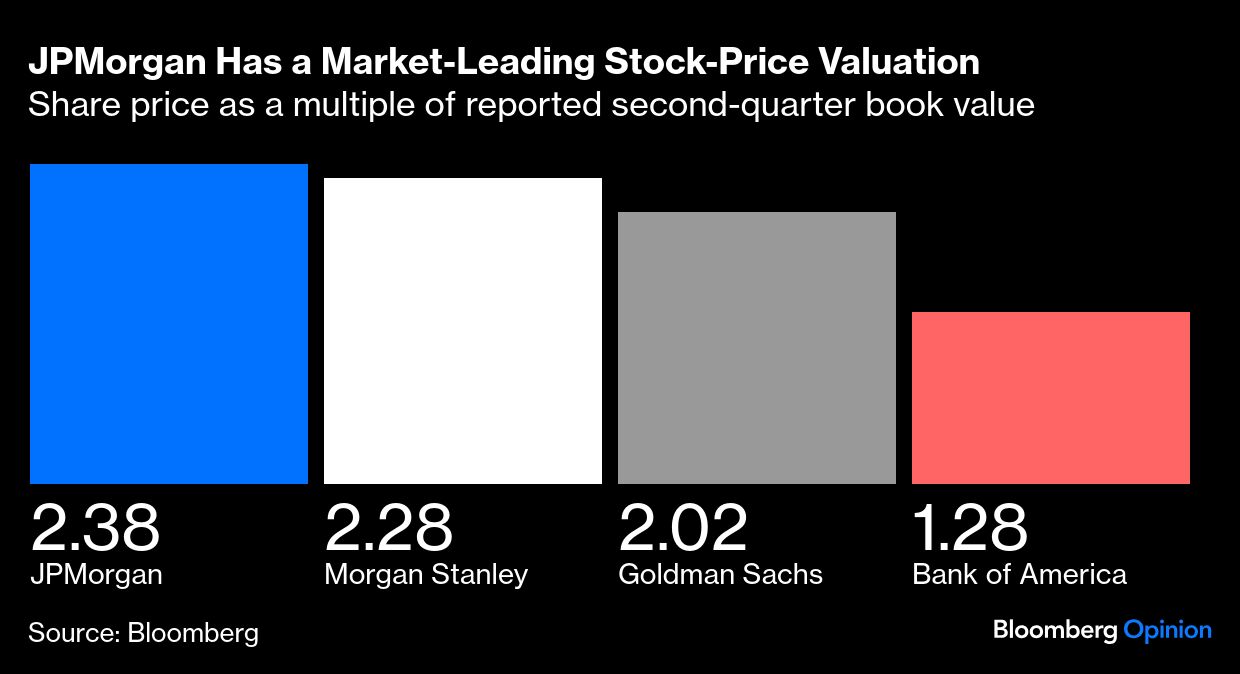

Sounds great, but there’s a problem: Its shares are so highly valued that this is a bad trade for the bank. The current price is 2.4 times the book value per share that JPMorgan reported for the second quarter – buying those shares for investors means paying them more than double the current net asset value of the company they own. “No one's going to convince me that's a brilliant thing to do,” he said on last week’s earnings call.

But the money must be used for something, otherwise it will drag on JPMorgan’s returns — like a fund manager sittng on too much idle cash. More acquisitions could be the answer; not in US banking, where it’s already well beyond the antitrust threshold of about 10% of national deposits, but perhaps in technology. Here, the bank could be a bit shy after being bitten a couple of times lately. There was the $175 million Frank debacle and another fintech deal in Europe, Viva Wallet, that has led to rounds of litigation. As Jeremy Barnum, JPMorgan’s chief financial officer, put it in his eternally dry style on the recent earnings call: “We have learned some lessons. We don't want to overlearn those lessons.”

Lending more or taking greater risks in trading aren’t straightforward options either, especially while credit and equity markets are at high valuations and the economy faces huge uncertainties, driven mainly by the mercurial leadership of President Donald Trump. Regardless, Dimon and Barnum believe there’s plenty of space to grow JPMorgan’s balance sheet over time without deals and still hit its 17% return on equity target through a range of outcomes and business cycles.

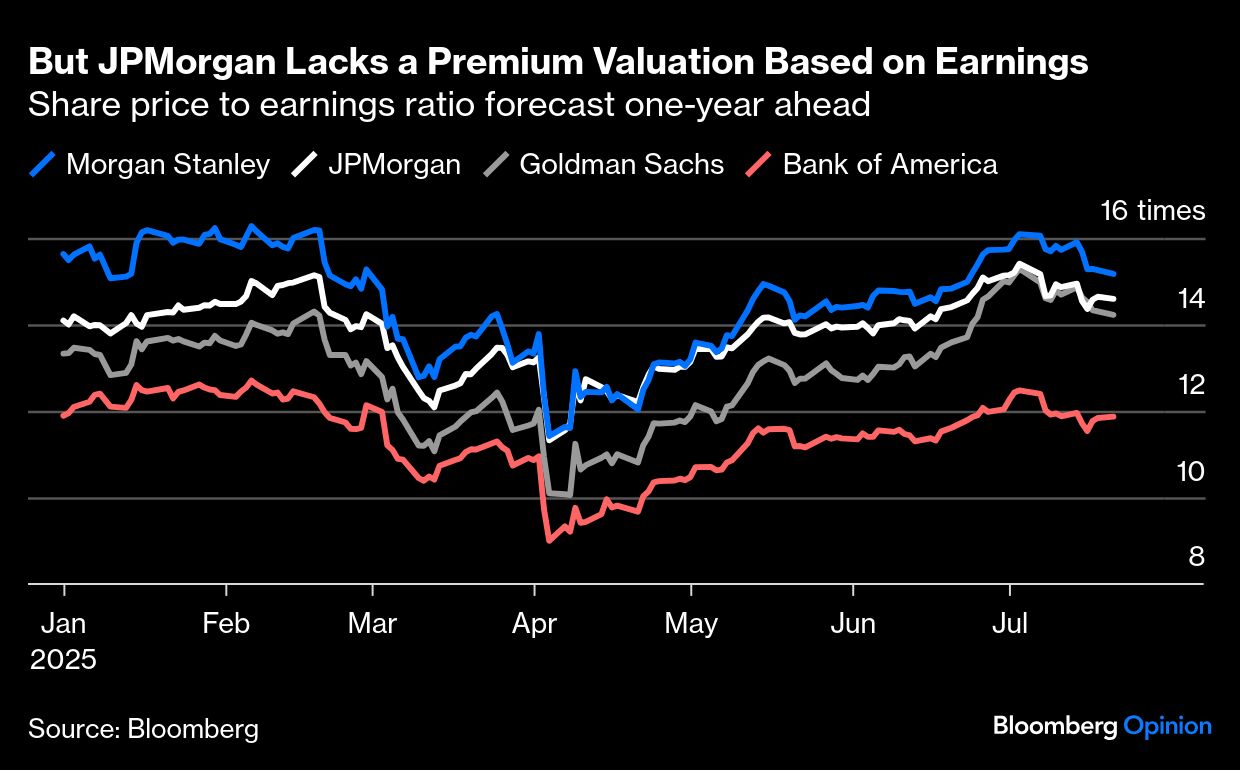

Others want or expect to see more. Mike Mayo, a banking analyst at Wells Fargo & Co., reckons JPMorgan can become the first $1 trillion market cap bank within three years. Ebrahim Poonawala, his counterpart at Bank of America, says the stock is undervalued in terms of its price-to-earnings ratio because in other industries the leading companies trade on much bigger premiums than the rest.

If investors push JPMorgan’s stock price even higher on that basis, its already stretched price-to-book valuation will be even more inflated, making buybacks more costly and increasing the pressure on the bank to spend its excess capital in other ways – all of which could be terrible for returns.

The goodwill Dimon has among investors offers him space to navigate this in the medium term, although that won’t be true forever. The bank might just sit on larger-than-normal buffers of equity for now. “I like having excess capital,” he told investors at first-quarter results in April. “We are prepared for any environment.”

This is a set of problems others would wish for, but it could bring another period of slowing profit growth or even returns that fall behind rivals again. History says that may not be a bad thing for JPMorgan; it may just signal the same patience, paranoia and adaptability that has seen the firm come to dominate American finance and become one of the biggest banks in the world with $4.5 trillion of assets.

Size alone isn’t enough to cause disaster, to re-purpose Dimon’s early quote, especially when more than $1 trillion of JPMorgan’s assets today are essentially cash. What matters is that the bank continues to be properly managed and that the pressure of its high valuation doesn’t lead to bad decisions. That’s what investors and regulators should care about today — and even more so once Dimon hands responsibility for running this behemoth to someone else.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.