Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

- Personalized Target Date Accounts (PTDAs) use risk capacity, not risk tolerance, to set asset mixes for defaulted 401(k) participants, exposing them to excess risk.

- PTDAs as Qualified Default Investment Alternatives (QDIAs) cannot truly personalize investments for disengaged participants, since risk tolerance cannot be inferred from data.

- Wealth is used to determine risk capacity, but (1) the rich don’t default because they are financially savvy and (2) the rich want to stay rich.

- The one demographic that all defaulted participants have in common is financial naiveté, so they need to be protected. There’s no need for personalization.

- A safer, more protective 'Master PTDA' should serve as the QDIA for defaulted participants, especially those near retirement, rather than risky personalization.

- PTDAs are best suited for self-directed participants who actively disclose their risk tolerance; defaulted participants should avoid PTDAs to protect their retirement savings.

This is a warning to participants in retirement savings plans who do not make an investment election, especially baby boomers who are in the most jeopardy because losses now will ruin the rest of their lives. There’s a movement underway to improve retirement investments through personalization, but it will do more harm than good in the next stock market crash because it uses the wrong information for defaulted participants.

This article recommends a better way to personalize. Personalization is a good idea if implemented correctly, but the current implementation is not correct.

Risk Capacity Is Not Risk Tolerance

You might not have heard of the recent innovation in retirement saving investments, but you can be sure that your plan’s fiduciaries are being pitched, and you might actually be invested in it. If so, you need to know what’s wrong. Personalized Target Date Accounts (PTDAs) integrate your personal information with target date fund glidepaths.

This makes sense on one level, because investing is personal. However, the unfortunate reality is that PTDAs are using the wrong personal information for defaulted participants.

Risk capacity is the personal information that is being used, despite the fact that it has long been understood that risk tolerance should govern the risk in investments. Tolerance is, by definition, less than capacity. This means PTDAs are taking more risk than defaulted participants actually want or need, because they take the most risk that can be afforded — capacity.

Much has been written about the ability to take risk versus the willingness to take risk, including in my recent article. Data can be used to establish capacity, but investors must disclose their tolerance, because it can’t be inferred from data.

Risk tolerance is emotional and personal. Most rich people (with high risk capacity) want to stay rich, so they generally have low risk tolerance. Similarly, poor people might want to take big risks in order to stop being poor. The problem is that those who default into a QDIA do not want to engage, so their risk tolerance is unknowable. Personalization does work for non-defaulted participants, but that’s not a QDIA.

The problem is that PTDA providers are offering their product as a Qualified Default Investment Alternative (QDIA), which means that those participants will not engage — their risk tolerance cannot be known. Capacity is used instead as a (very poor) proxy for tolerance. Here’s how.

Datapoints

PTDA providers use the following recordkeeper data to establish an asset mix for defaulted participants who will not talk to them.

Investment Horizon: Current Age and Target Retirement Age

Risk capacity declines as retirement nears because we will rely on that money to carry us through retirement years when there are no paychecks. This is the basis for glidepaths in target date funds.

Wealth: Account Balance, Salary, Contribution Rate and Marital Status

The presumption is that the wealthy can afford risk, which means their risk capacity is high. That’s true, but most rich people want to stay rich, so their risk tolerance is not high. Big bets (high risk) might have made them rich, but protecting it keeps them rich. Also, please know that rich people don’t default because they are financially savvy and they can afford advice.

Using wealth for defaulted participants typically signals “not rich,” which translates into low risk capacity, so low risk. Why bother segmenting on wealth, when most typically fall into the safe group? Marketing perhaps?

Glidepaths

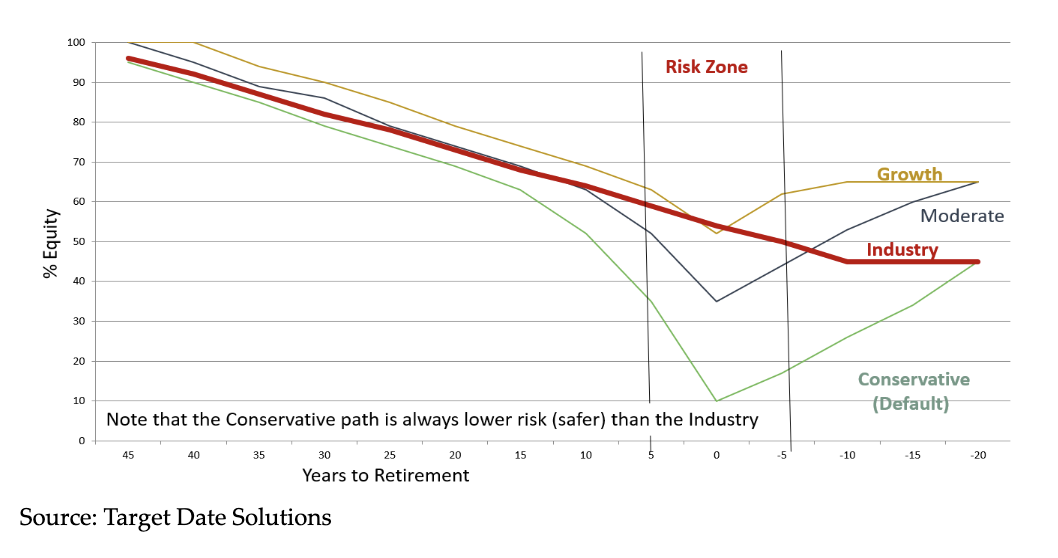

Unlike most target date funds (TDFs) with a single glidepath, PTDAs come with an array of glidepaths with varying risk, such as those shown in the following graphic.

The “industry” shown in the graph is the S&P target date fund index aggregate of all TDFs. It is 85% in risky assets at the target date on average. By contrast, the “conservative” glidepath is 30% risky at the target date. It is like the glidepath followed by the Federal Thrift Savings (TSP) TDF, Dimensional Fund Advisors, and Soteria.

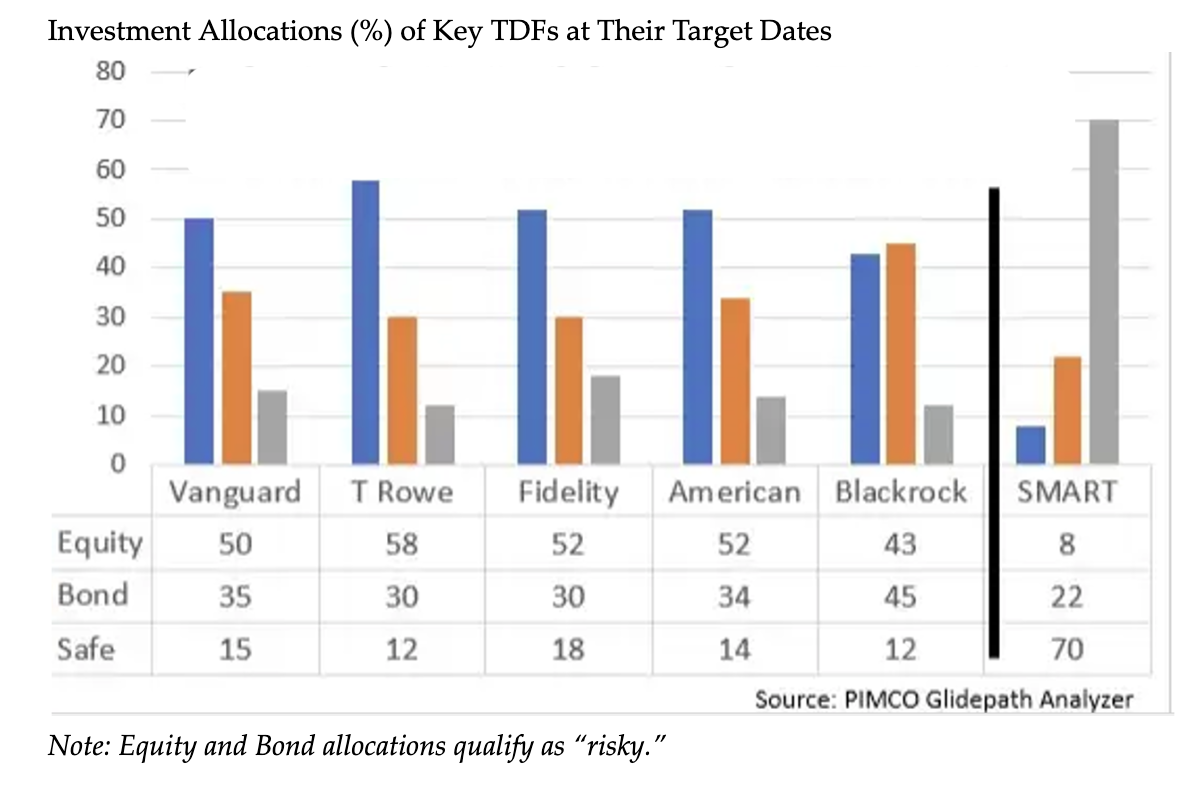

PTDAs as a QDIA tend to mimic the industry, which is dominated by the Big Three oligopoly. Vanguard, Fidelity and T Rowe Price manage 65% of the $4 trillion in TDFs. The use of risk capacity in PTDAs favors the Industry glidepath.

Also note the U shape in the PTDAs paths that re-risk in retirement to extend the life of assets. This is unique to my design, Soteria, which takes the recommendation of Kitces and Pfau in optimizing the post-retirement glidepath.

A Better Approach for Defaulted Participants: A Master PTDA as the Plan’s QDIA

Instead of confusing risk capacity with risk tolerance/aversion, safety is the answer for those who default because they are financially naïve and in need of protection. Also, academic lifetime investing theory argues for safety near retirement.

In other words, personalization is not the answer for defaulted people; safety is the answer. Since the rich don’t default, the right “answer” for most defaulted participants with low wealth (risk capacity) is safety, so no need to glamorize it with “personalization.”

“Personalization” is an important advancement in retirement investing and a differentiator against the Big Three oligopoly. But it simply does not work as QDIA.

In a master PTDA, the plan sponsor chooses a risk level and a retirement age for all defaulted participants, unlike a TDF where the fiduciary must accept the provider’s glidepath. For most plans, the risk choice should be conservative, but some plans’ demographic is wealthy, for example a doctor’s group, so the choice could be for more risk.

A master PTDA for all defaulted participants is a good QDIA. This master PTDA is the ultimate custom TDF. For most plans, this master PTDA should protect those near retirement, despite the fact that most TDFs do not protect near retirement, as shown above. Importantly, this master PTDA uses investments on the plan’s platform, so they are, in principle, the best. By contrast, target date funds use the proprietary investments of the offering fund company, which are unlikely to be the best in every asset class.

True Personalization for Non-defaulted Participants (Not a QDIA)

Individual PTDAs should be used by self-directed (non-defaulted) participants because they want to engage and they do disclose their risk tolerance. How do they know their risk tolerance? It’s personal. Self-directed participants choose their risk, which they can change at any time, and they choose the day that they will leave the plan, which they can also change at any time.

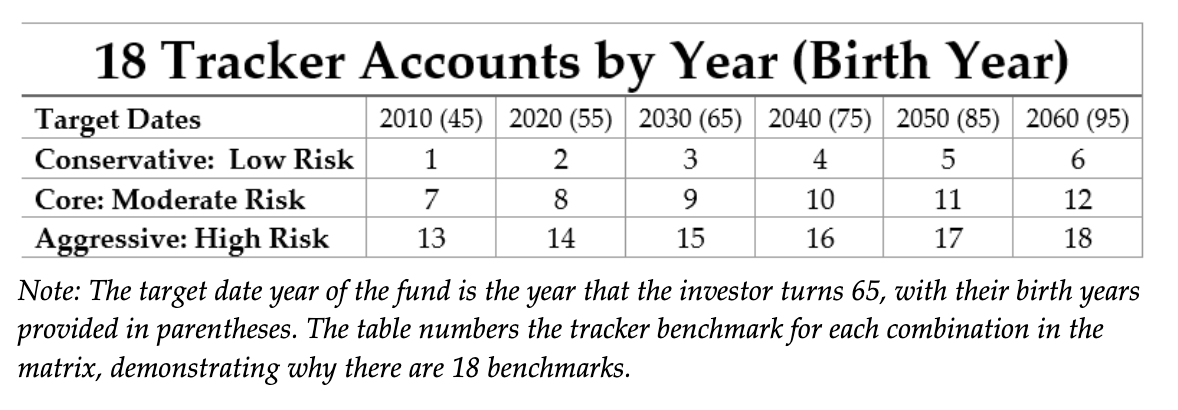

Self-directed (non-defaulted) participants manage their own unique target date accounts. There are as many glidepaths (accounts) as there are self-directed participants using PTDAs, creating a benchmark challenge that, nonetheless, can be addressed. A family of benchmarks like the 18 shown in the following matrix will help these participants put their actual performance into perspective. They own their performance, so they should be able to evaluate themselves.

Recommendation Summary

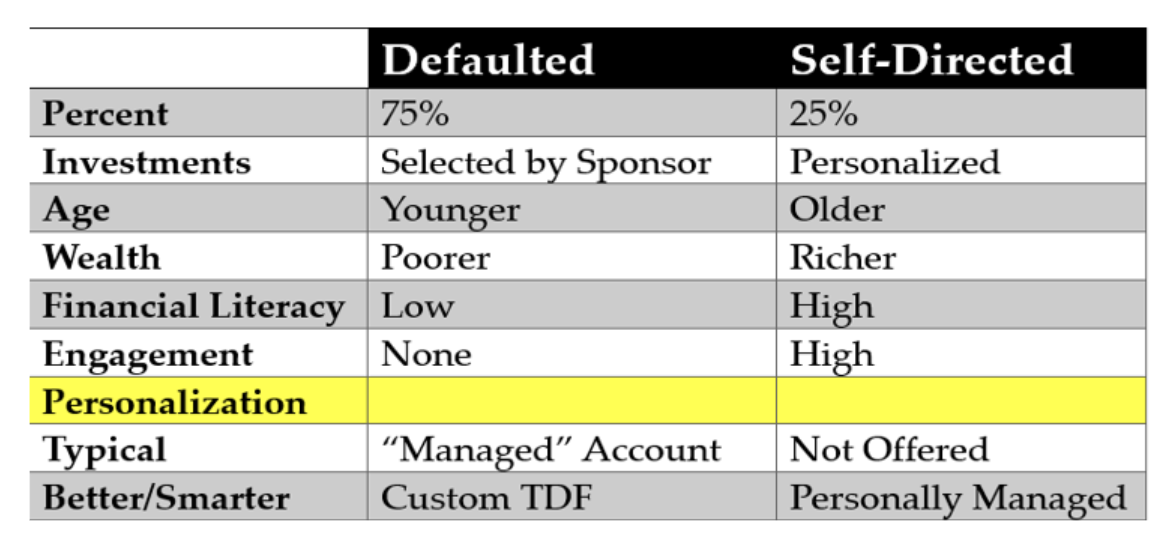

The following table summarizes the two distinct groups and the two different approaches for personalizing their investments:

Conclusion

PTDAs are coming to market as QDIAs, but their promise of personalization cannot be kept. No one can personalize investments for someone they don’t know. Data can give the provider clues about the investor’s ability to take risk, but providers really need to know the investor’s willingness to take risk, which defaulted participants don’t know —even if they do know, they won’t tell their provider.

Fiduciaries need to be leery of PTDAs that serve as QDIAs. Participants who default in 401(k) plans need to know if they are in a PTDA. If they are, they should get out.

PTDAs should be provided to self-directed participants, and a master PTDA should be used for all defaulted participants.

Baby boomers need to be especially concerned because they are in the Retirement Risk Zone, when investment losses can devastate the rest of life. Their risk capacity is low, and their risk tolerance is likely even lower. Baby boomers could find their retirement nest eggs radically diminished, reducing how long their savings last, as well as their standard of living.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

For anyone who relies on TDFs — or advises those who do — Surz’s new book is a must-read guide to understanding the risks, solutions, and future of a secure retirement.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.