The Federal Reserve kept benchmark interest rates unchanged on Wednesday but edged closer to a resumption of cuts, perhaps as soon as the next monetary policy meeting in mid-September. Keep the champagne on ice; the central bank’s growing dovishness should have all of us concerned.

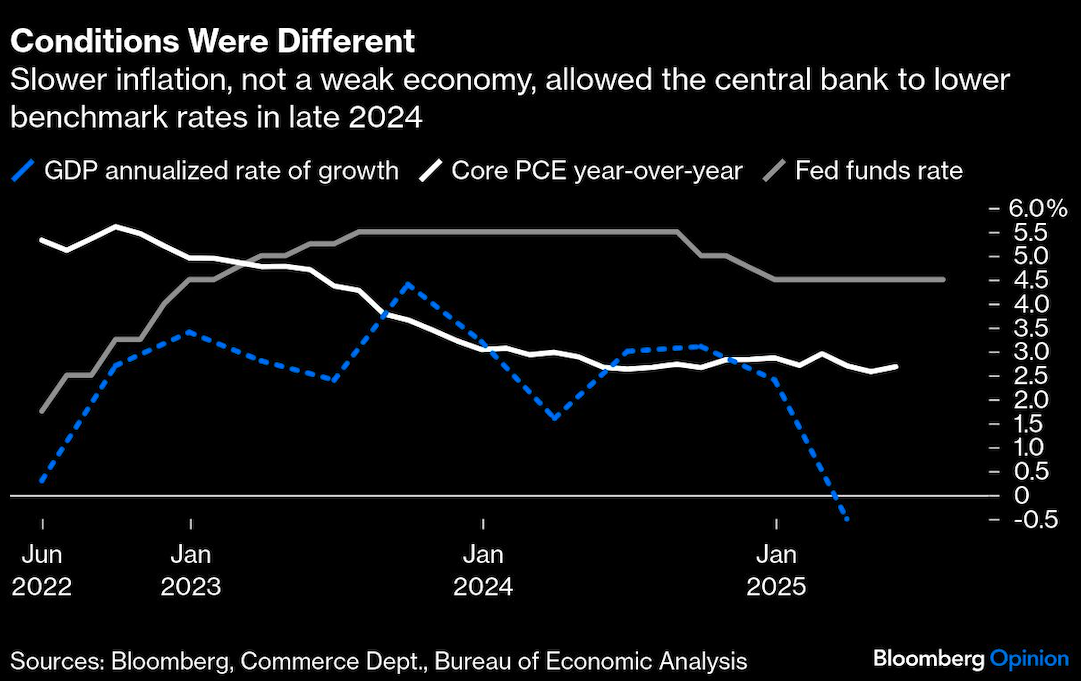

Unlike in late 2024 when a benign environment for inflation gave policymakers the confidence to lower the target for the federal funds rate three times, from 5.50% to 4.50%, this time the easing will be in response to economic weakness that typically leads to job losses and rising unemployment. The Fed suggested as much, acknowledging in a statement that “growth of economic activity moderated in the first half of the year.” That’s a clear downgrade from just six weeks ago, when it said the economy “has continued to expand at a solid pace.”

During the press conference, to explain the reason for keeping rates unchanged, Fed Chair Jerome Powell emphasized the downside risks to the labor market while saying any inflation tied to the Trump administration’s tariff policies might only be temporary. Inflation is “most of the way back” to the central bank’s 2% target, he said. In a sign of the growing pressure to ease policy, two Fed governors dissented for the first time since 1993, wanting to see a rate cut now.

Already, uncertainty over the Trump administration’s tariffs — essentially taxes paid by US importers on foreign goods brought into the country — is showing signs of paralyzing businesses and concerning households. Consider the gross domestic product report for the second quarter that was released earlier Wednesday. The Commerce Department said the economy expanded at a 3% annualized rate in the April through June period, rebounding from a 0.5% decline in the previous three months. But those reports were skewed by businesses front-running tariffs. The important thing to know is that personal consumption — which accounts for two-thirds of the economy — was anemic, gaining 1.4% after a very soft 0.5% increase in the first quarter. Add them together and you have the worst six-month stretch for spending since the last half of 2022.

And there’s more: On Tuesday the Labor Department said the hiring rate was just 3.3% in June, which is well below the pre-Covid average of about 3.9% and in line with levels generally associated with recessions. The Budget Lab at Yale estimates that the levies put on so far — with more to come — will reduce annual gross domestic product by $115 billion and result in average per household income loss of $2,400.

Responses to the Dallas Fed’s monthly manufacturing outlook survey of businesses in a deeply red district of the US reveal the extent of the unease. “Demand has been soft all summer. Our outlook has dimmed recently, with the volume of new orders declining. New business has been tougher to convert,” is how one respondent in the food manufacturing sector put it. “We are implementing layoffs and reduced working hours in August,” was the response from an executive in the transportation equipment manufacturing sector. From a furniture and related product manufacturer: “Tariff changes require a sit back and watch attitude. There is no way to forecast.”

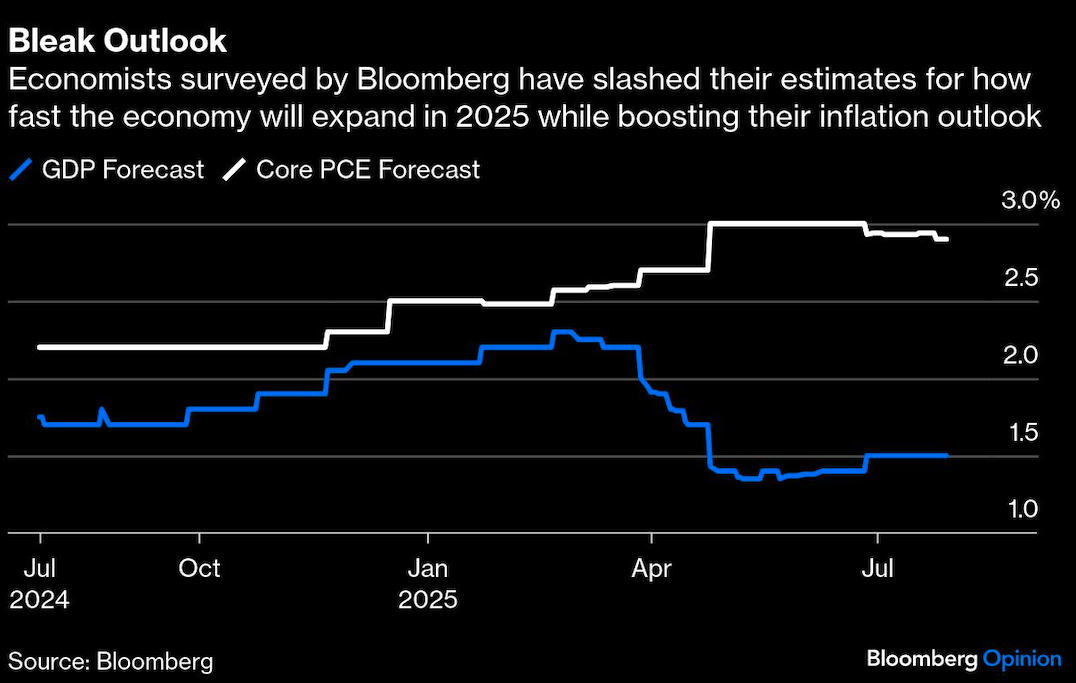

Given such comments it’s easy to see why economists have slashed their growth forecasts. From a peak of 2.30% in February, the more than 70 economists surveyed by Bloomberg now see GDP expanding just 1.50% this year, down from 2.8% in 2024 and the slowest since the 2020 recession that was caused by the global pandemic. And 2026 isn’t looking much better, with growth forecast at just 1.6%.

Slow growth isn’t the only concern. Both economists and investors expect inflation to accelerate as companies attempt to pass on the tariffs they must pay on imported goods to customers. Again, here’s how one respondent in the textiles manufacturing sector described the situation in the Dallas Fed survey: “We are starting to see vendors and suppliers pass on more price increases, with ‘tariffs’ being the explanation. We are weighing our options for passing this price increase on to our buyers, eating the additional cost/reducing our margin, or a combination of the two.” The derivatives market shows the outlook for inflation rates over the next 12 months among bond traders has more than doubled since September to around 3.44%, which is uncomfortably higher than the Fed’s target of 2% inflation.

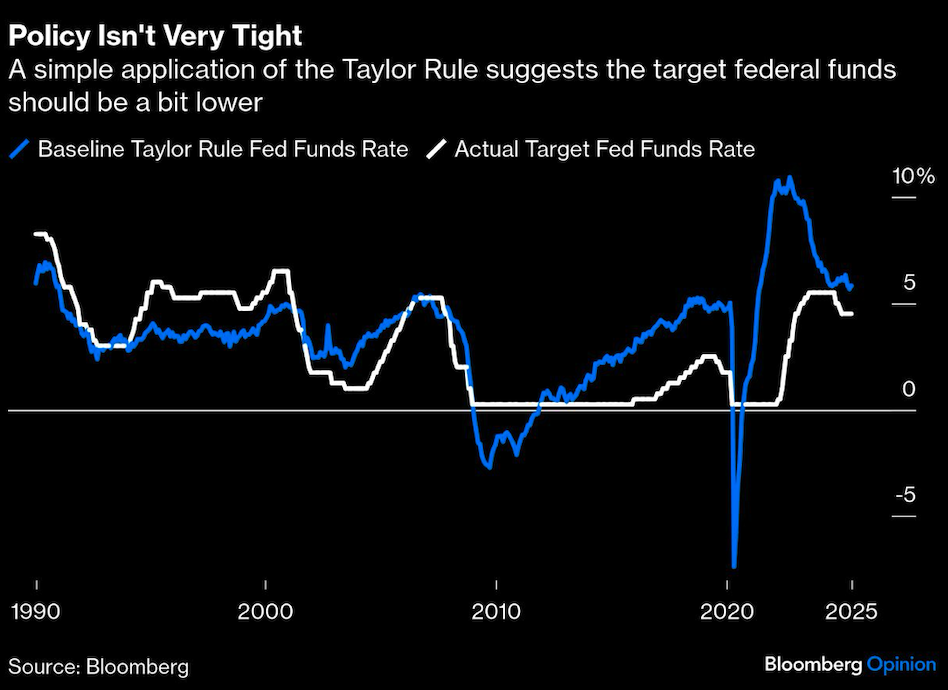

It’s not like monetary policy is overly tight. A conventional Taylor Rule would suggest the fed funds rate be set at around 4.1% based on the current unemployment rate of 4.1%, inflation that is around 3% and the Federal Open Market Committee’s estimate of a 1% neutral fed funds rate. And the FOMC has penciled in two rate cuts for 2025, based on the median estimate of FOMC members in the Summary of Economic Projections from the June policy meeting. (Note that we’ll get two more Consumer Price Index reports and two more monthly jobs reports before policymakers convene again to decide monetary policy, meaning much can change between now and then.)

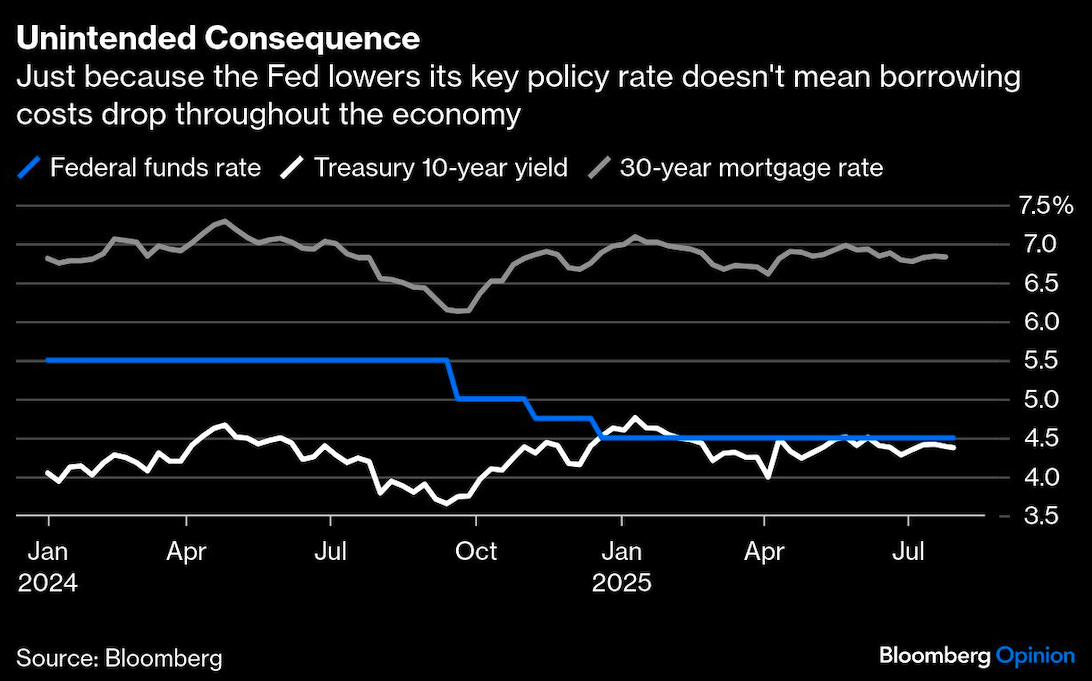

The risk for the Fed is that rate cuts end up having the opposite of the intended effect. When the central bank lowered its target for the fed funds rate late last year from 5.50% to 4.50%, borrowing costs throughout the economy actually rose, with the yield on the benchmark 10-year Treasury note rising from around 3.65% to 4.76% by early January because investors believed that the move by policymakers was premature and would only keep inflation elevated. As a consequence, rates on 30-year mortgages jumped from 6.13% in September to around 7%, according to the Mortgage Bankers Association.

The Fed has been under much pressure from the White House to lower rates, with President Donald Trump declaring: “Too Late—Powell is the WORST. A real dummy, who’s costing America $Billions!” But Trump’s argument lies in his belief that the Fed should ease because inflation has been whipped. Of course, that’s not true. Still, he may get his wish on rates sooner rather than later, but for all the wrong reasons.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.