Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

To start the year, President Trump’s uncertain policy with respect to trading partners, paired with the expected increased debt load coming from the One Big Beautiful Bill, has renewed speculation among investors about the dollar’s supremacy around the world.

Accompany this uncertainty, we have seen the yield on U.S. long-term debt jump close to 5% and the U.S. dollar drop 10% in value. In tandem, these two things are never a good sign for the world’s reserve currency, and the developments have sparked new debates about the nature of the dollar as a safe haven asset.

Now, of course we have heard all this before — many arguments have been made in the past on how the euro would replace the dollar as the dominant currency in world trade or how BRICs would come together to challenge U.S. dollar supremacy. I will not repeat those arguments, but I will point out that one particular oft-overlooked capability will most likely determine the dominant currency in the future — the ability of a currency to preserve and protect the value of intangible assets into the future.

The rise of intangible assets

A currency traditionally has three dimensions: It acts as a medium of exchange, a unit of account, and a store of value. Each of these features of a currency have different importance throughout history. And, it is the third feature in a very specific form that will most likely be the crucial feature a currency will need to have to enjoy supremacy in a 21st-century world economy.

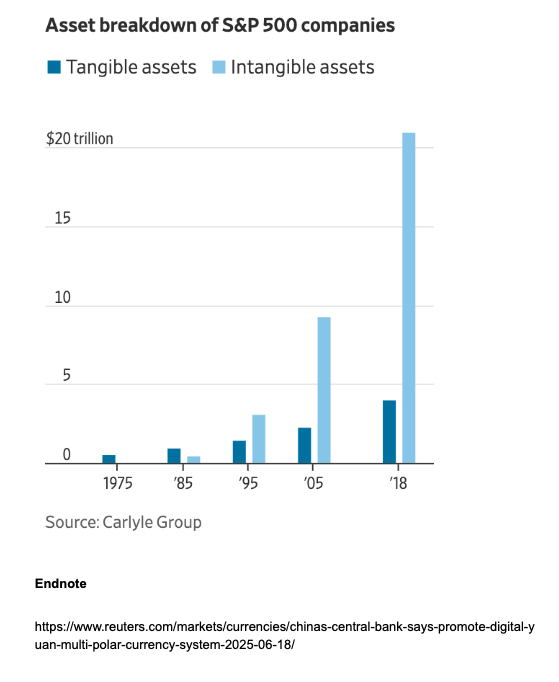

To highlight this, consider the degree to which our economic engines and wealth are driven by intangible assets these days. The Carlyle Group did an asset breakdown study of the S&P 500 in aggregate throughout time (it should be noted that the S&P 500 constitutes approximately 60% of world market cap). In 1985, one-third of the assets in the S&P 500 were intangible assets and two-thirds were tangible assets. By 1995, this had flipped to approximately two-thirds being intangible and one-third being tangible. And, by 2018, the S&P asset makeup was just 15% tangible assets and 85% intangible assets.

The protection of intangible assets and preserving the value of such over time is now an incredibly important feature of a currency. It is no longer the case that the wealthiest people in the world hold hard assets that are easily converted into cash in the future. Most wealth is tied up in intangible assets like human capital, intellectual property, etc., that have no or little value in the future unless protected by a nation state or some other feature.

Intangible assets are difficult to collateralize and difficult to secure into the future without a strong legal framework. For this reason, the U.S. dollar is still supreme at this moment in time due to the legal protections we offer (e.g., strong corporate rule of law, monetary independence) and timely resolution without expropriation.

If the vast majority of wealth is held in intangible assets, then the dominant currency will need to protect these rights to future claims through legal frameworks and treaties around the world. We have already seen, once again, China hinting at a digital yuan to rival the U.S. dollar in transactions around the world. Yet, if the yuan and China do not do more to protect intangible assets on a consistent basis, the currency will never hold the mantle of supreme world currency in transactions or sovereign savings.

Derek Horstmeyer is a Professor of Finance at George Mason University's Costello College of Business.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Derek Horstmeyer

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.