Should Your Clients Use Savings to Defer Social Security?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

Last month, the Bipartisan Policy Center released “Hedging the Risk of a Longer-than-Expected Life—The Value of a Social Security Bridge Strategy” authored by Emerson Sprick. Among the report’s key findings, Mr. Sprick says,

“A well-designed bridge strategy can significantly enhance retirement security and improve retirees’ financial well-being.”

In June of this year, Dr. Michael Finke wrote an article for Think Advisor entitled, “Why Advisors Should Never Recommend Social Security Claiming at 62.” In that article, he said,

“To understand why delaying Social Security increases total wealth, it is best to use a holistic balance sheet approach that includes the present value of income streams such as pensions and Social Security as well as stocks, bonds, cash and home and business equity. Then split the balance sheet into bond-like and equity-like assets.

Delayed claiming increases the present value of wealth from Social Security.”

Dr. Finke also notes that current fears about Social Security’s funding and administration, and uncertainty about the system’s future is driving more retirees to claim earlier than they may have wanted. He said,

“It's not surprising that many clients are concerned about whether they can count on Social Security in the future. While it may appear that an easy solution is to simply take the money now before the fraud-riddled program blows up, they shouldn’t. Early claiming means giving up tens or even hundreds of thousands of dollars of retirement wealth as well as an important source of inflation-protected lifetime income.”

The Actuarial Financial Planner (AFP) models I make available in my website use the “holistic balance sheet approach” utilizing present value calculations referred to by Dr. Finke. In this article, I will discuss the automatic Social Security bridge strategy built into the AFP models and look at several hypothetical client situations to quantify how much a Social Security bridge strategy (SSBS) may actually enhance your retired client’s retirement security.

Key Takeaways

Here are my take-aways regarding Social Security bridge strategies:

- If your retired client wants to use a “safety first” approach to fund essential expenses, and the present value of their future essential expenses exceeds the present value of their Floor Portfolio of non-risky assets/investments, implementing an SSBS will be generally financially favorable and will increase the client’s funded status (the ratio of the present value of their assets to the present value of their spending liabilities).

- Based on the default assumptions in the AFP, implementing an SSBS will increase a retirees’ real dollar annual income derived from Social Security and a bridge compared with the annual real dollar income expected to be derived from immediate commencement of Social Security plus annual withdrawals from the client’s assets that would have been used to fund the bridge. For deferral of commencement from age 62 to age 70, this ratio is 1.13 for non-smoking males and 1.16 for non-smoking females under the default assumptions.

- To the extent that the client has additional sources of income other than just the amount necessary to fund the bridge period, the increase in expected annual real income associated with the 62 to 70 SSBS will be less than 13% (or 16% for females) under the default assumptions, but it will still be positive.

- The planning assumptions used to determine the financial effect of an SSBS should be consistent with the planning assumptions used to value the client’s spending liabilities. For example, the longer the assumed lifetime for determining both the client’s assets and spending liabilities, the more value to implementing an SSBS, all things being equal. Also, the lower the assumed real rate of return used to discount floor plan assets/essential expense liabilities, the more value to implementing an SSBS.

- Based on current lifetime income annuity purchase rates and default assumptions in the AFP, implementing the age 62 to age 70 SSBS is more favorable financially than purchase of a single life annuity with accumulated savings equal to the present value of expected bridge payments. (a comparable ratio of 1.08 vs. 1.13 for purchase of a single life annuity for a 62-year-old male).

- Implementing an SSBS can involve the depletion of a significant portion of a client’s accumulated savings early in retirement.

- Not all retired clients will be able to afford to — or will want to — implement an SSBS. As noted by Dr. Finke, an SSBS will generally be more attractive to clients who:

-

- plan to live longer;

- have sufficient assets to relatively easily fund their bridge payments;

- want to bolster their floor portfolios; and

- have other accumulated savings to invest in more risky assets.

- Under most reasonable sets of planning assumptions, it will be financially advantageous to implement an SSBS. Whether the resulting increase in a particular client’s financial security can be considered to be “significant,” as claimed by Mr. Sprick, is debatable.

- While the size of the Social Security benefit will affect the amount of accumulated savings required to bridge, it has no effect on the relative financial benefits of deferring (assuming the same planning assumptions are used).

- It is more financially advantageous to implement an SSBS that defers commencement from age 62 to age 70 (or even to age 67) than one that defers commencement from age 67 to 70.

- It will still be financially advantageous to implement a “62 to 70” SSBS today even if Social Security benefits are assumed to be reduced by 20% across the board eight years from now, but the extent of the expected increase in financial wealth in that event is closer to the expected increase from purchase of an annuity today based on current purchase rates.

Background & Using the AFP Models to Build Your Client’s Bridge

It is almost always financially advantageous to keep working after age 62, keep saving and keep deferring commencement of one’s Social Security benefits (but not beyond age 70). What’s being analyzed in this article is the financial benefits of ceasing employment on or after age 62, delaying claiming Social Security benefits that one might be eligible to receive and using accumulated household savings (or other sources of income) to “bridge” the period of deferral prior to one’s desired Social Security claiming age.

There are many other factors to consider when helping a client select when to commence Social Security benefits, including potential spousal benefits, possible Roth conversions, possible future Social Security reform, etc. This article will not address these other factors.

If your client is considering implementing an SSBS, the Actuarial Financial Planner models available in my website can be very helpful. To determine the present value and impact on your client’s funded status of immediate commencement of their current Social Security benefit, simply enter the amount of the annual Social Security benefit in the appropriate cell (E(12) of the AFP for Single Retirees) and “0” as the deferral period (cell G (12)). The present value of this benefit under input assumptions is shown in the PV Calcs tab.

To determine the present value and impact on your client’s Funded Status of deferring your Social Security benefit, simply enter the projected annual Social Security benefit at later commencement (including adjustments for different early retirement factors, late retirement factors and inflation during the deferral period) in cell E (12) and the number of years of deferral in cell G (12).

The AFP can also be used to calculate the present value of the annual bridge payments from the client’s accumulated savings that are designed to increase by inflation each year and produce a constant real dollar annual income from the combination of bridge payments and Social Security. Of course, these calculations should be revisited annually to adjust for any changes in the projected Social Security benefit at desired commencement age.

Following the process outlined above, the AFP will automatically develop an SSBS assuming the client has sufficient assets to fund the bridge payments.

As noted above, when performing an analysis of the relative benefits of an SSBS vs. immediate commencement, it is important to use the same planning assumptions that are used to value the present value of essential expense liabilities. Therefore, if the client and advisor want to use conservative investment return and longevity assumptions to value the client’s essential expense liabilities, those same planning assumptions should also be used to value the financial viability of implementing an SSBS.

Example Tables of SSBS

I show results for the following five SSBS examples using the AFP to generate and compare the present values of bridge strategies under various planning assumptions for the future:

Table 1. Commencement at age 62 vs. at age 70, average benefit

Table 2. Commencement at age 62 vs. at age 70, high benefit

Table 3. Commencement at age 62 vs. at age 67, average benefit

Table 4. Commencement at age 67 vs. at age 70, average benefit

Table 5. Commencement at age 62 vs. at age 70, average benefit with 20% across-the-board reduction after eight years

Different lifetime planning periods were based on results from the Actuaries Longevity Illustrator for a non-smoking 62-year-old (or 67-year-old in Table 4) male in excellent health. The 25% probability of survival for a 62-year-old male is 31 years (age 93), the 50% probability of survival is 26 years (age 88) and the 75% probability of survival is 19 years (age 81). Note that these survival probabilities differ slightly from the current default assumptions used by the AFP, which are based on 2022 planning horizons.

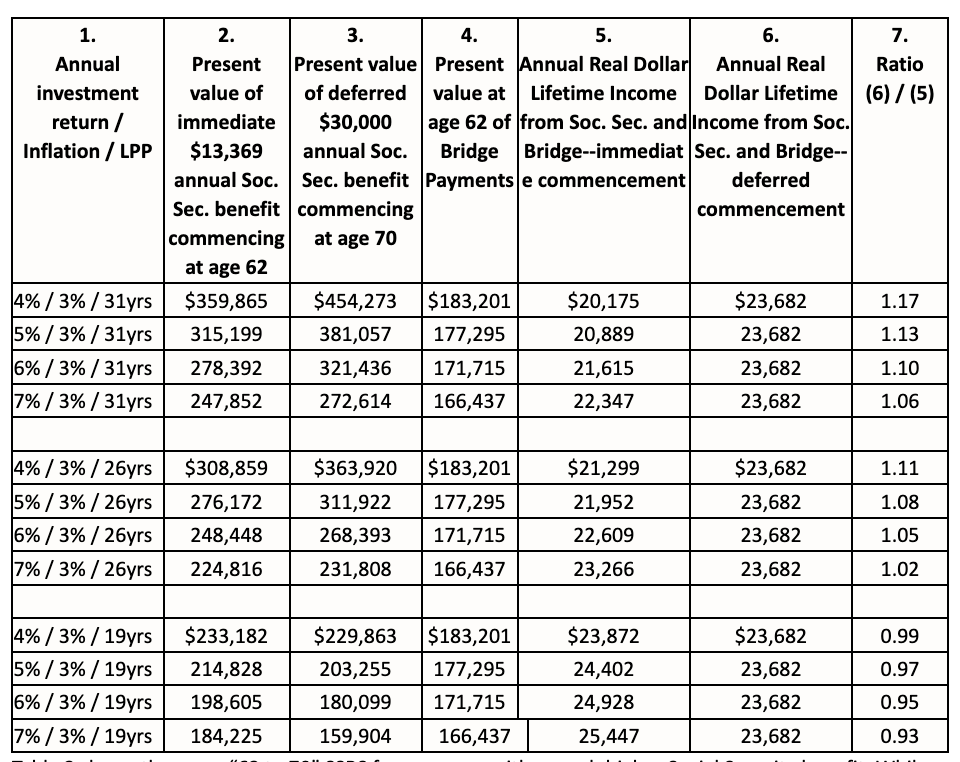

Table 1 shows present values of an immediate annual benefit of $13,369 payable at age 62 for an average-income retiree vs. present values of a deferred annual benefit payable at age 70 of $30,000 under the planning assumptions shown in Column 1. It also shows the present value at age 62 of the expected bridge payments during the eight-year deferral period. Column 5 shows the annual real dollar lifetime income expected from the total of the age 62 Social Security benefit plus annual withdrawals from accumulated savings assumed to be equal to the present value of the bridge payments. Column 6 shows the annual real dollar lifetime income expected under the assumptions from the SSBS. Column 7 shows the ratio of these two annual expected lifetime income streams.

Under the default assumptions (5% annual investment return/3% inflation and 31 years lifetime planning period), the ratio of the income streams is 1.13 in favor of deferral, and the present value of the eight expected bridge payments is $177,295. Thus, if the hypothetical individual had accumulated savings of exactly $177,295 at age 62, his total annual real dollar lifetime income from Social Security plus his accumulated savings under the SSBS is expected to be 113% of his total annual real dollar income from Social Security plus his accumulated savings under the immediate age 62 commencement alternative. If he has more accumulated savings, the ratio would be less. So, for example, if his total non-risky investments, including his age 62 immediate Social Security benefit, funded $40,000 of annual lifetime real dollar income, implementing the SSBS would be expected to increase his non-risky annual real dollar lifetime income to $42,793 under the default assumptions, an increase of about 7%.

If our example individual has less than $177,295 in accumulated savings, he would not be able to afford to fully implement a bridge strategy under these assumptions. Also note that even if our example individual had accumulated savings of something like $500,000, the bridge payments in this example would diminish those assets by about 35% over the eight-year deferral period, so SSBS can require a substantial commitment to deploy a large portion of accumulated savings in the early years of retirement. Not all retirees will be comfortable with this level of commitment.

If the example individual had been a female, the lifetime planning periods would have been 34 years (25% probability of survival), 28 years (50% probability) and 22 years (75% probability). Under the default assumptions, the present value of her bridge payments would have been the same, but the ratio of annual real dollar payment streams would have been 1.16 instead of 1.13 in favor of the SSBS.

Table 1. Commencement at age 62 vs. Commencement at age 70—Average Benefit

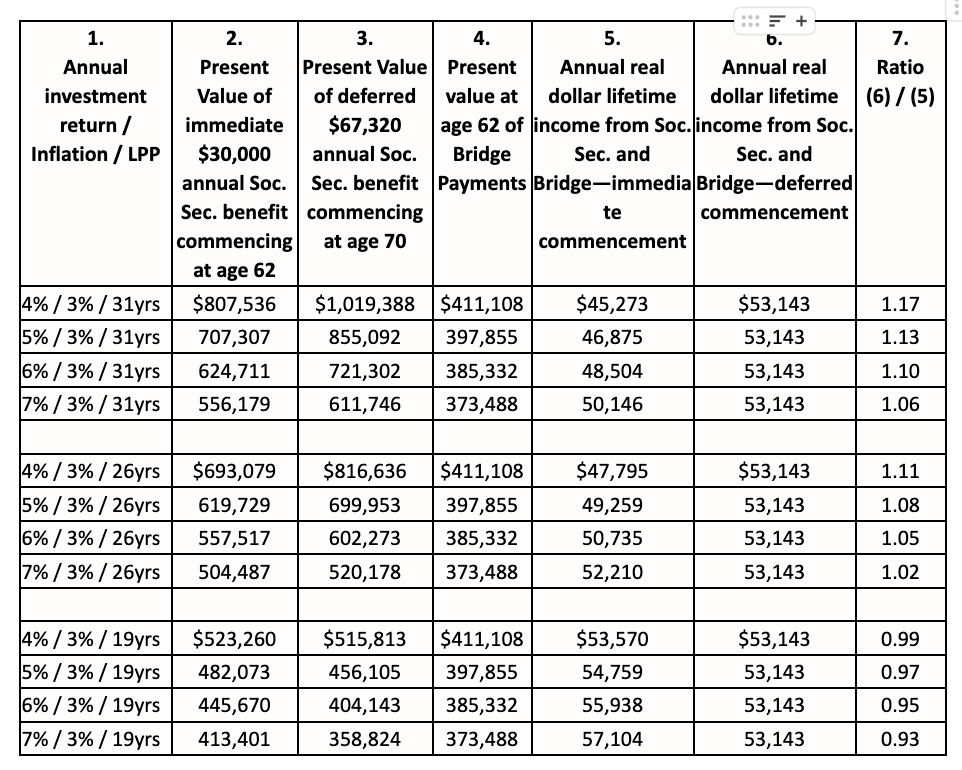

Table 2 shows the same “62 to 70” SSBS for someone with a much higher Social Security benefit. While the ratios of real dollar payment streams for each set of assumptions are the same, the present values of the bridge payments required during the deferral period are much more substantial.

Table 2. Commencement at age 62 vs. commencement at age 70—High Benefit

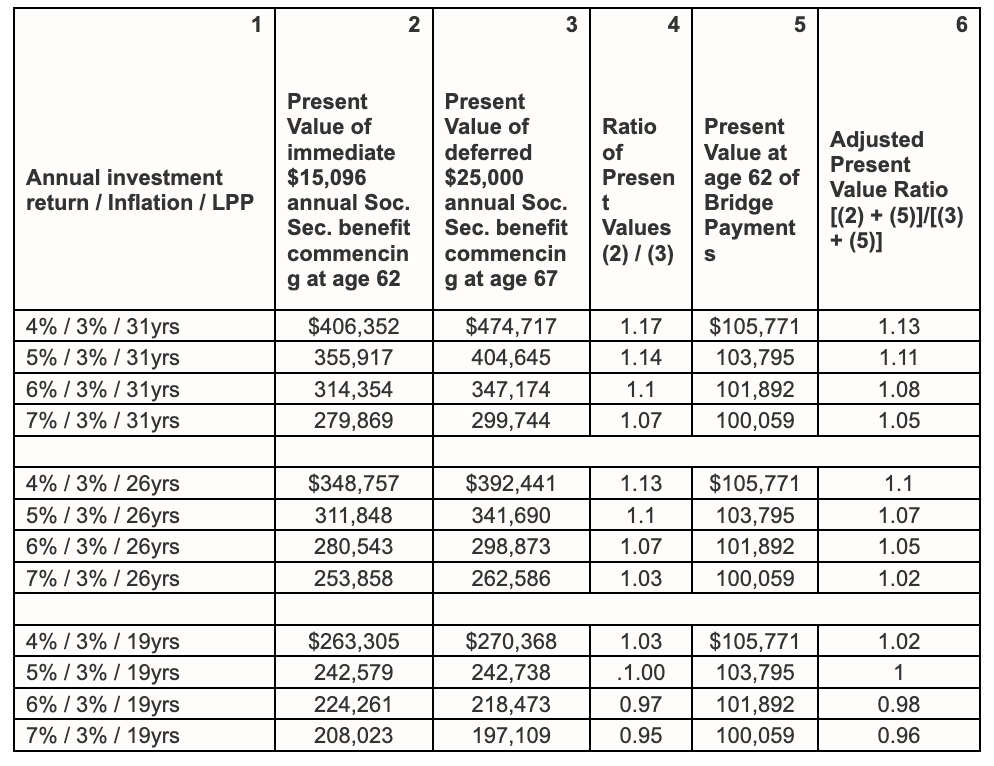

Table 3 shows the SSBS comparisons for commencement at age 62 vs. commencement at age 67. These results are a little bit less favorable than results for deferral all the way until age 70. Under the default assumptions, the ratio of expected real dollar payments is 1.11 vs. 1.13 for deferral until age 70.

Table 3. Commencement at age 62 vs. commencement at age 67

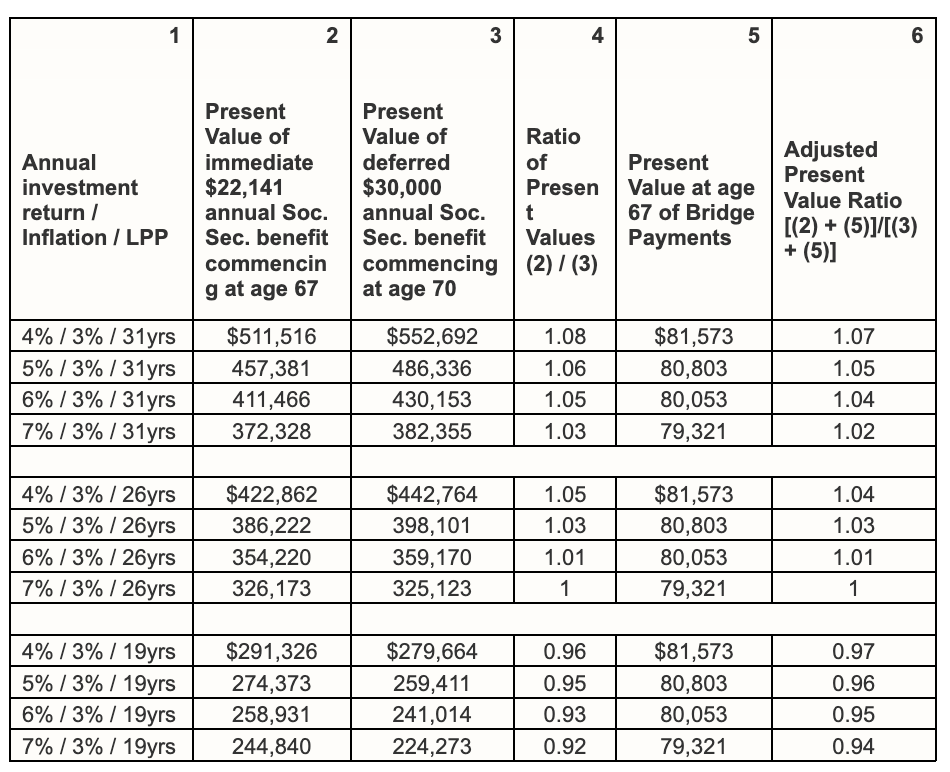

Table 4 shows SSBS results for commencement at age 67 vs commencement at age 70. These results show that the financial benefit of deferring the last three years is not as beneficial as deferring prior to Social Security normal retirement age, but is still favorable for most sets of reasonable planning assumptions. Under the default assumptions, the ratio of expected real dollar payments is 1.05.

Table 4. Commencement at 67 vs. commencement at age 70

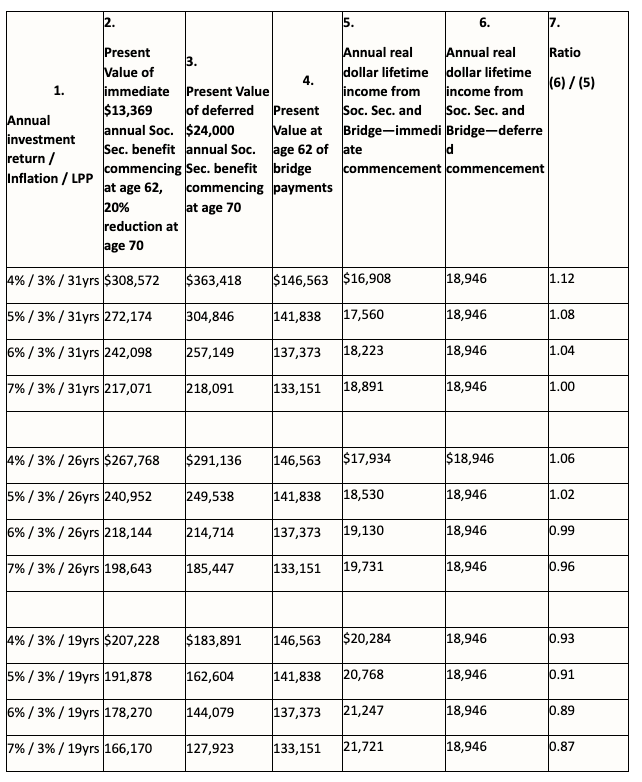

Table 5 attempts to address the question of whether an SSBS will still work if we assume Social Security benefits are cut by 20% across the board eight years from now, just when our hypothetical “62–70” average retiree would commence his deferred benefits. The present value of Social Security bridge payments would be less because, in this case, the annual real dollar target at age 70 would be reduced by 20%.

The table shows that there still may be value in deferring under certain planning assumptions, but the value is reduced somewhat. Under the default assumptions, the 1.13 ratio is now 1.08, or about the same ratio anticipated to be produced by purchase of a lifetime annuity based on current annuity purchase rates.

Table 5. Commencement at age 62 vs. commencement at age 70, average benefit with 20% across-the-board decrease at age 70

Summary

In Table 1, I showed that under our “default” assumptions, a 62-year-old man who is eligible to receive immediate annual Social Security payments of $13,369 must commit to withdrawing a present value of $177,303 from his accumulated savings over the next eight years to implement a Social Security Bridge strategy deferring commencement until age 70 that will provide level real dollar income. If that is his entire accumulated savings, he can expect to receive annual payments from his savings plus his Social Security benefits totaling $23,682 in real dollars each year under the SSBS. If he decides, instead, to commence benefits immediately, he will take withdrawals gradually, and he expects his total annual income under the non-deferral approach will be $20,889 in real dollars each year. Thus, the ratio of expected incomes under the two approaches is 1.13 in favor of the SSBS if the retiree spends his entire accumulated savings on bridging his Social Security. If he has greater accumulated savings, the expected increase in his annual real dollar lifetime income from the SSBA is expected to be less than 13%, but will still be positive.

If the client wants to plan on a 20% across-the-board decrease in Social Security benefits eight years from now, the SSBS would provide him level annual lifetime income of $18,946 (20% less than under the no-decrease scenario). This would still be about 8% greater than the lifetime annual benefit generated from commencing his benefit at age 62 and anticipating a 20% reduction of that benefit at age 70.

A Social Security bridge strategy is a good idea for individuals who have sufficient assets to easily fund their bridge payments, who need to beef up their floor portfolios and who have other accumulated savings invested in more risky assets. We agree with Mr. Sprick that it is probably a good idea to consult with a financial advisor before implementing an SSBS, especially one that can be expected to consume a large portion of household accumulated savings.

Ken Steiner is a retired actuary with a website titled, "How Much Can I Afford to Spend in Retirement?"

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All