If ever there were conditions that cried out for stimulus, China appears to have met them. Recent gauges of growth and inflation were more than just disappointing.

After an encouraging start to the year, the expansion is in trouble. But authorities have given little sign they are prepared to jettison the caution that has characterized their actions. Fiscal policy has already done some work and, while economists predict interest-rate cuts later this year, the reductions are likely to be modest. The wait-and-see approach could be justified while activity was holding up reasonably well and the US was figuring out just how punitive tariffs would be. Beijing seems intent to just muddle through.

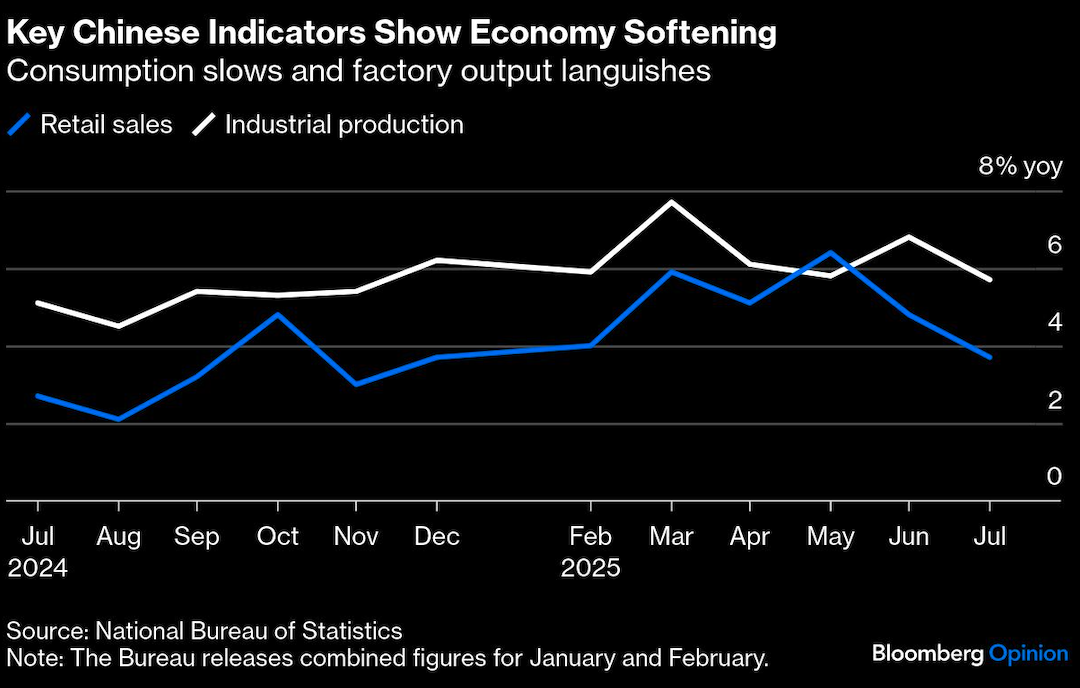

Figures released on Friday show a pronounced slackening. Production was more sluggish than anticipated and retail sales, which President Xi Jinping hoped would be a bright spot, were off the boil. Fixed-asset investment, a proxy for capital spending, languished. The jobless rate in urban areas edged up; at 5.2% it exceeds the US national measure by a fair margin. Deflationary pressures persist and the number of new loans plunged.

There's no good reason for the People’s Bank of China to hesitate. Incremental cuts of around 10 basis points, the size the bank prefers, will only go so far. It would be a pleasant surprise if it delivered a full-quarter point reduction, though this is often the bare minimum for central banks elsewhere. That's probably hoping for too much, but whatever the monetary authority had planned should be brought forward.

What — or who — might be staying Governor Pan Gongsheng’s hand? The bank isn't independent in the manner of the Federal Reserve or the European Central Bank. China's leadership is probably concerned about sending the wrong signal, one that has a whiff of panic or betrays a sense of vulnerability. That's understandable when trade talks with Washington are progressing. It's easy to see President Donald Trump milking stimulus on social media. He went as far as calling India's economy, which is projected to grow faster than China’s this year, a “dead” one. (The White House last week extended a pause on higher duties for China for another 90 days, a step that was matched by Xi.)

Also worrying is a crackdown on the price wars that the government is blaming for too-low inflation. The state has launched a campaign to curb the cutthroat competition that’s eroded profits and driven down wages. Addressing the specter of deflation is good, but this resembles a shoot-the-messenger approach. The consumer price index has been hovering around zero for a few years; the cost of living didn't take off after the pandemic as it did elsewhere. The chief problem is a lack of demand from households, which partly reflects the persistent fallout from a real-estate collapse.

Excess industrial capacity isn't helping. The Communist Party’s decision-making body listed the goal of addressing “disorderly competition” among companies as one of its top priorities. It's easy to see unemployment climb some more. If there is to be less production, there's less need for staff. And that will keep chipping away at household confidence. China's challenges are all linked.

Monetary policy isn't a balm for everything. Fiscal and regulatory levers also need to be pulled. And given the PBOC's subordination to the Communist Party, it's unfair to expect too much. That doesn't mean that rates and bank reserve requirements don't have their role. Moving quickly on those fronts can provide a signal that poor numbers have the attention of rulers. Xi was heading in the right direction, allowing increased spending to put a floor under the slowdown. There’s more to be done.

China no doubt wants to tough out its current difficulties. The long game has appeal, especially given Beijing prefers to see its models and governance as superior. Panic is rarely constructive, but responding in a firm way to swings in the economy has much to commend it.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.