Traders are piling into one specific options wager that relies on a dovish Federal Reserve slashing interest rates by over a quarter-point next month.

The intensifying bet comes days ahead of the central bank’s annual gathering in Jackson Hole, Wyoming, where Fed Chair Jerome Powell is set to deliver pivotal remarks that could validate or nullify investors’ expectations for monetary easing. It also follows a hotter-than-expected read on inflation that caused some traders to dial back their rate-cut expectations.

Despite the brief pullback, traders so far appear to be sticking to the notion that rates will be lowered next month with Treasuries snapping a three-day selloff that pushed yields lower across tenors on Tuesday.

“As the market readies for Powell’s speech at Jackson Hole, we’ll argue that the biggest risk for Treasuries is if the Fed Chief chooses to throw cold water on the widely anticipated September rate cut,” Ian Lyngen, head of US rates strategy at BMO Capital Markets, said in a note.

The two-year yield was little changed on Wednesday at 3.75%. Longer tenors gained slightly, with the 10-year yield falling one basis point to 4.29%.

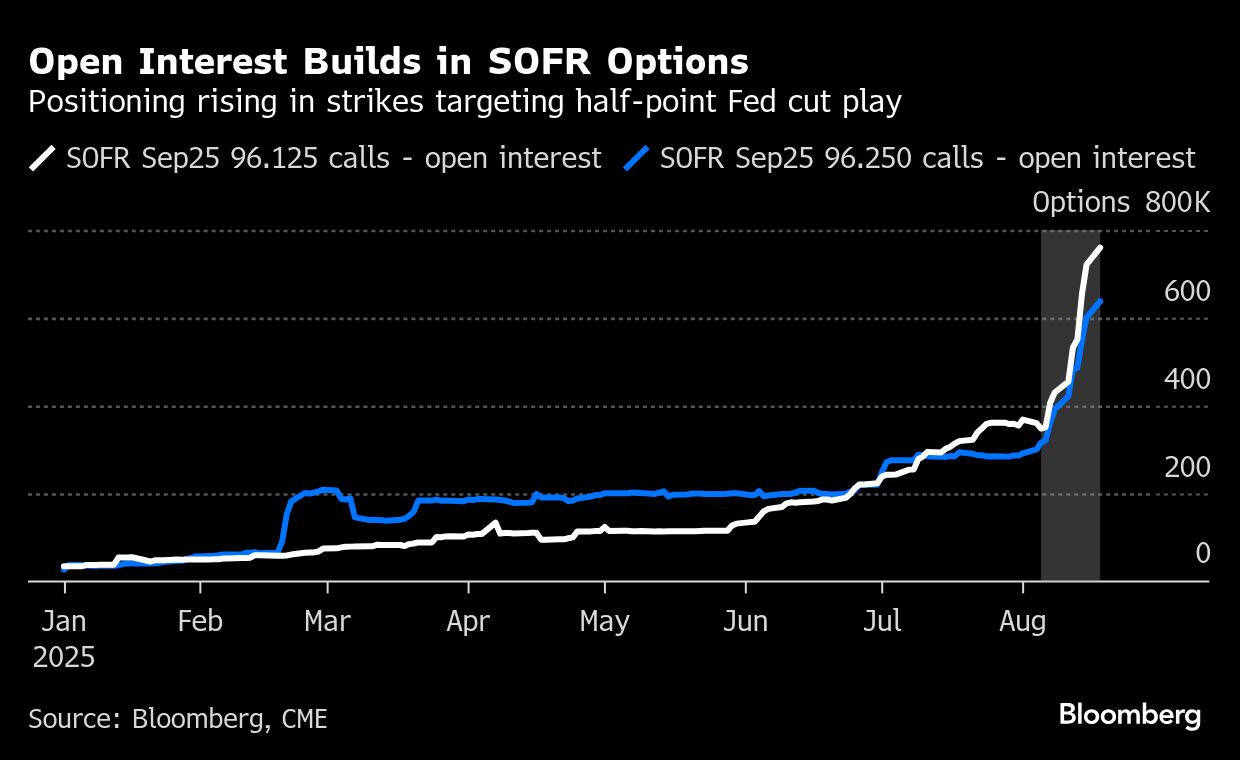

Demand for a position in the Secured Overnight Financing Rate (SOFR), which closely mirrors policy expectations, has been insatiable since the start of the month. This week, traders ramped up that wager again as open interest, or the amount of risk held by investors, surged in strikes targeting a half-point rate reduction.

Currently, a position of around 325,000 options, costing roughly $10 million, stands to profit by as much as $100 million should investors price in the Fed lowering rates by a half-point at the September policy meeting, a Bloomberg analysis shows.

Even after last week’s producer price index for July climbed the most in three years, signaling that tariffs are increasing companies’ costs, the mounting options position did not subside. The data, however, put a pause on a bond rally, sending yields on short-term Treasuries higher and prompting traders to scale back expectations for the Fed to ease rates over the remaining three policy meetings this year. Traders are now pricing in about an 80% chance of a quarter-point reduction at the Sept. 16-17 meeting.

“It’s worth acknowledging that the front-end of the curve is vulnerable to a bearish correction if Powell doesn’t deliver on the degree of dovishness that the market is currently anticipating,” said Lyngen.

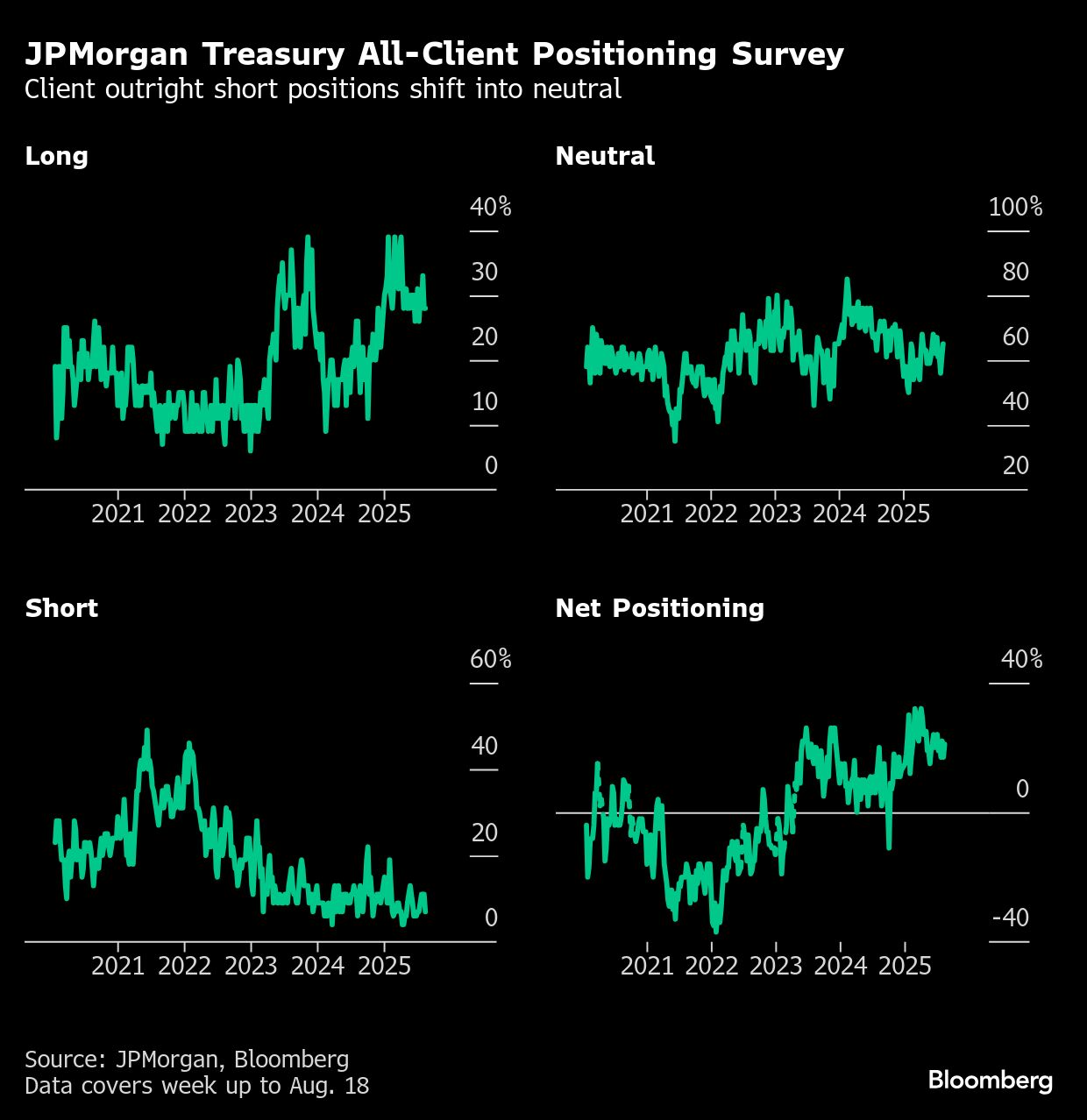

Meanwhile in the cash market, the latest read from JPMorgan’s survey of Treasury clients has shown investors switching out of short positions and into neutrals, which are now the most elevated in about a month.

Here’s a rundown of the latest positioning indicators across the rates market:

JPMorgan Treasury Client Survey

In the week ended Aug. 18, JPMorgan Treasury clients’ outright short positions dropped 4 percentage points, shifting into neutral, the survey showed. The outright short and neutral percentages now respectively sit at the lowest and highest levels since July 14.

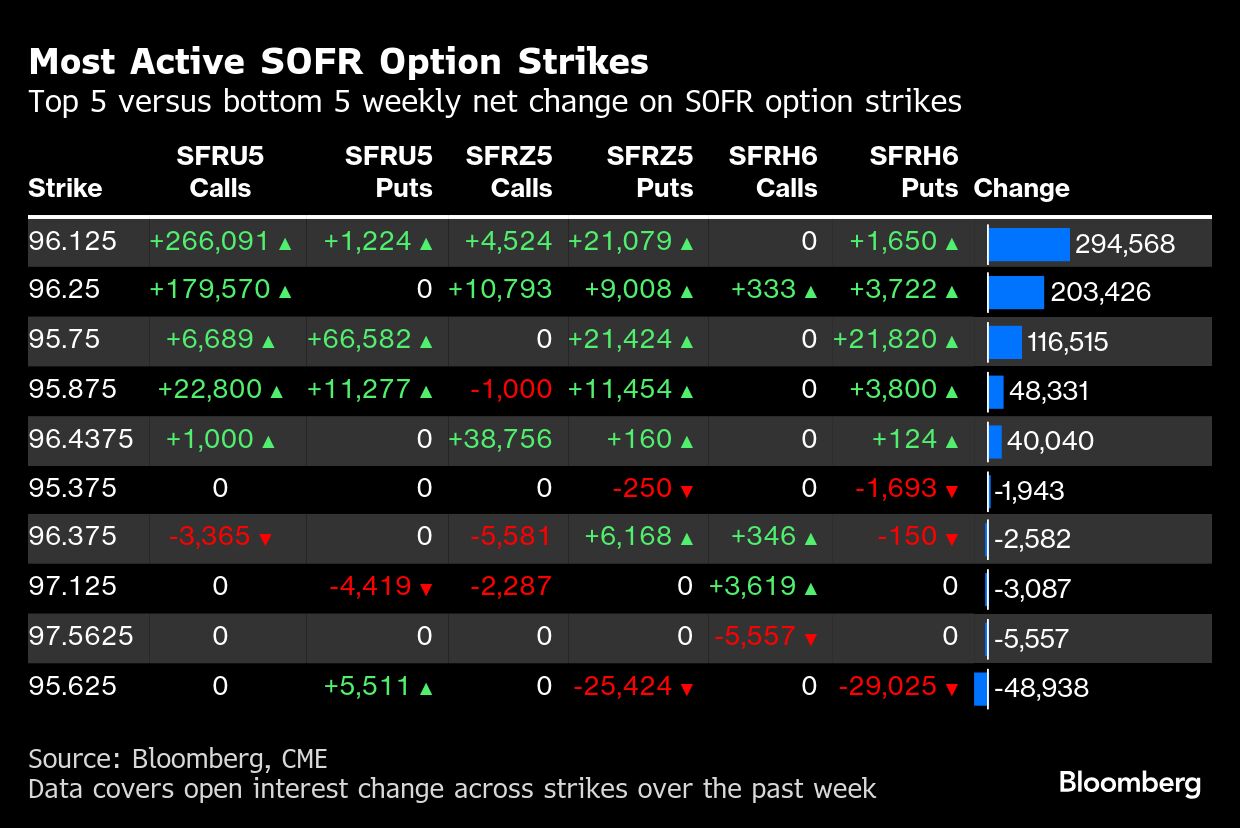

Most Active SOFR Options

In SOFR options across Sep25, Dec25 and Mar26 tenors over the past week there has been a jump in demand for the 96.125 and 96.25 strikes, which has shown new risk via a popular call spread position. Meanwhile, there has been a large amount of liquidation over the past week seen in the 95.625 strike via decent open interest reductions in the Dec25 puts and Mar26 puts.

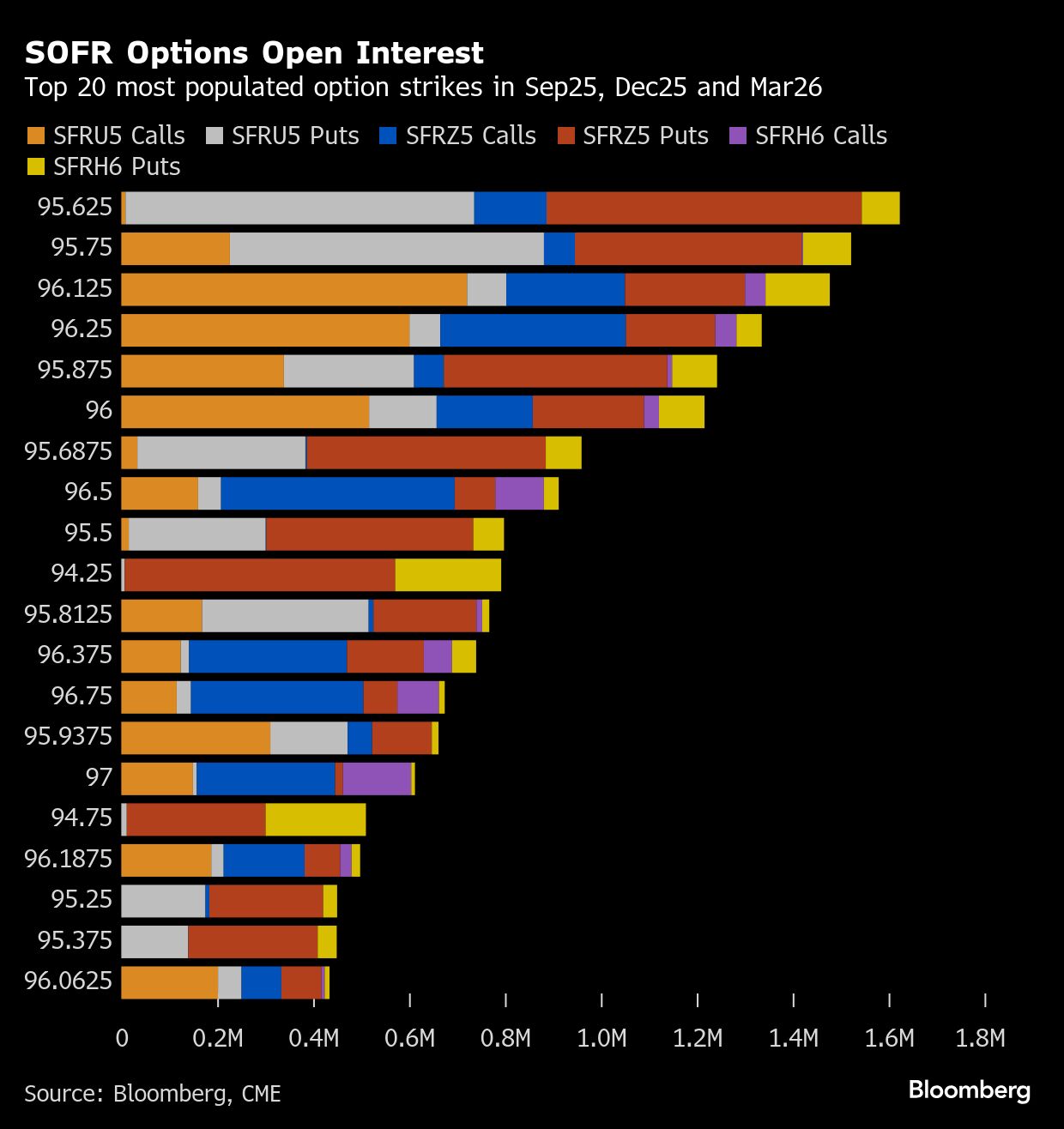

SOFR Options Heatmap

In SOFR options across Sep25, Dec25 and Mar26 tenors, the 96.125 and 96.25 strikes have moved up to the third and fourth most populated strikes due to heavy demand over the past week for the SOFR Sep25 96.125/96.25 call spread, while the SOFR Sep25 96.00/96.125/96.25 call fly has also been a popular play and traded again on Monday. The aggressive positioning and elevated open interest around these call strikes in the September SOFR options looks to target pricing of additional Fed rate cut premium into the September FOMC beyond a standard 25 basis-point move.

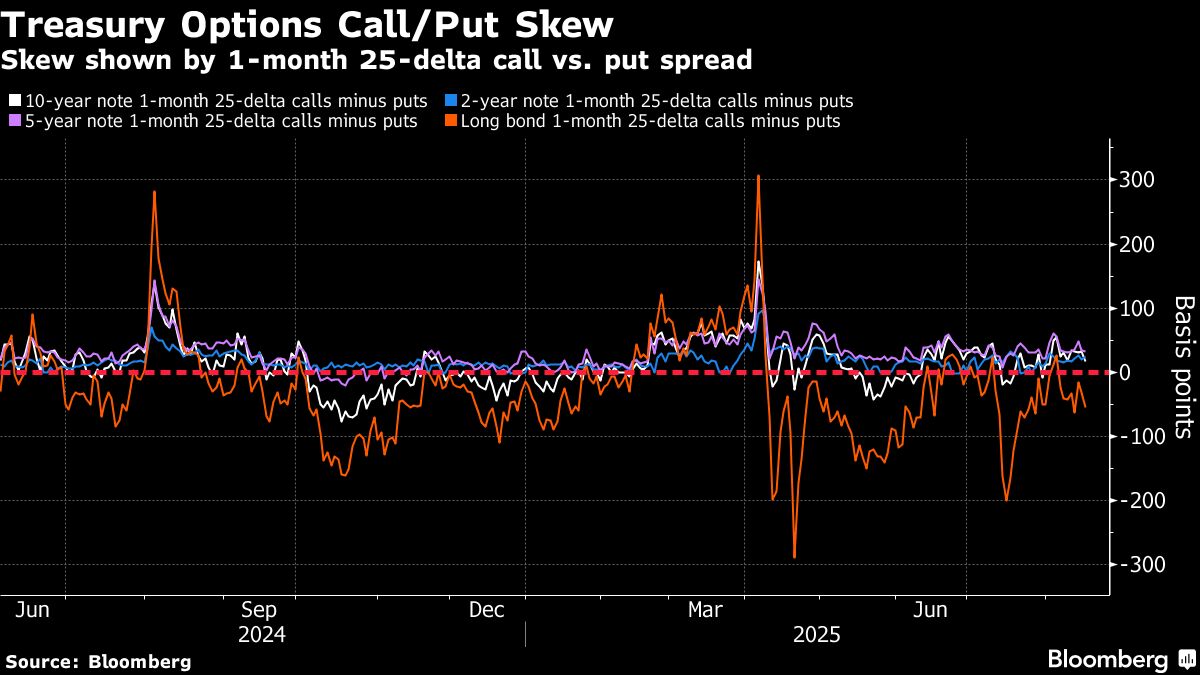

Treasury Options Skew

Treasury options skew in the long-end of the curve has drifted toward favoring puts over the past week, indicating traders paying a higher premium to hedge a selloff in long-bond futures. Options skew in the front-end out to the intermediates, however, slightly favors call premium, indicating traders paying up to hedge a rally in this part of the curve. The options skew signals demand for steepener positioning via the options market.

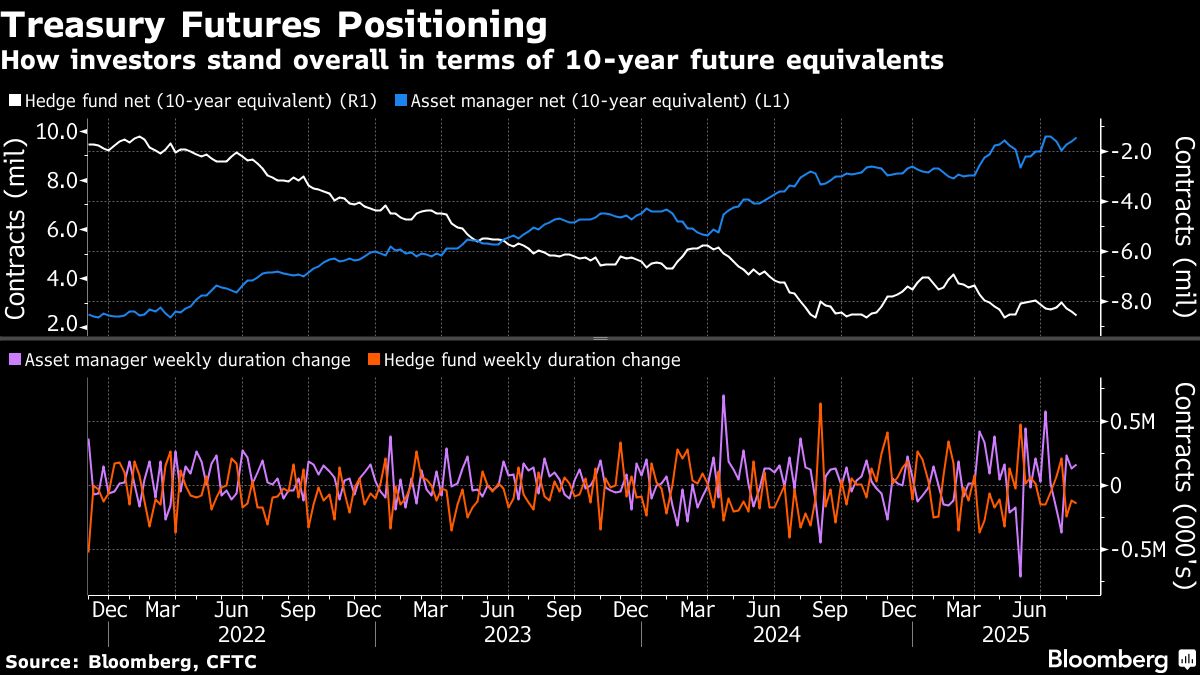

CFTC Futures Positioning

In the week ended Aug. 12, CFTC data shows asset managers added to net long positions across most of the bond futures strip. Notable net long extension was seen in the long-end via long-bond and ultra-long bond futures. For hedge funds, they added to net short positions in 10-year note futures, while covering short positions in the long-bond contract.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Edward Bolingbroke