For decades, betting that long-term bond rates would rise was known as the widow-maker trade: It was simultaneously the most sensible and the most consistently money-losing wager an investor could make. Could this be the month the trade finally pays off?

The logic remains sound. As rich countries grow older, they are spending like crazy, and they have no earthly way of paying for all their debt. So it stands to reason that rates will go up eventually. And yet for most of the last 20 years, rates didn’t go up — they went down. This so defied the basic laws of economics that some economists said they no longer applied — and then policy makers believed them, and spent even more.

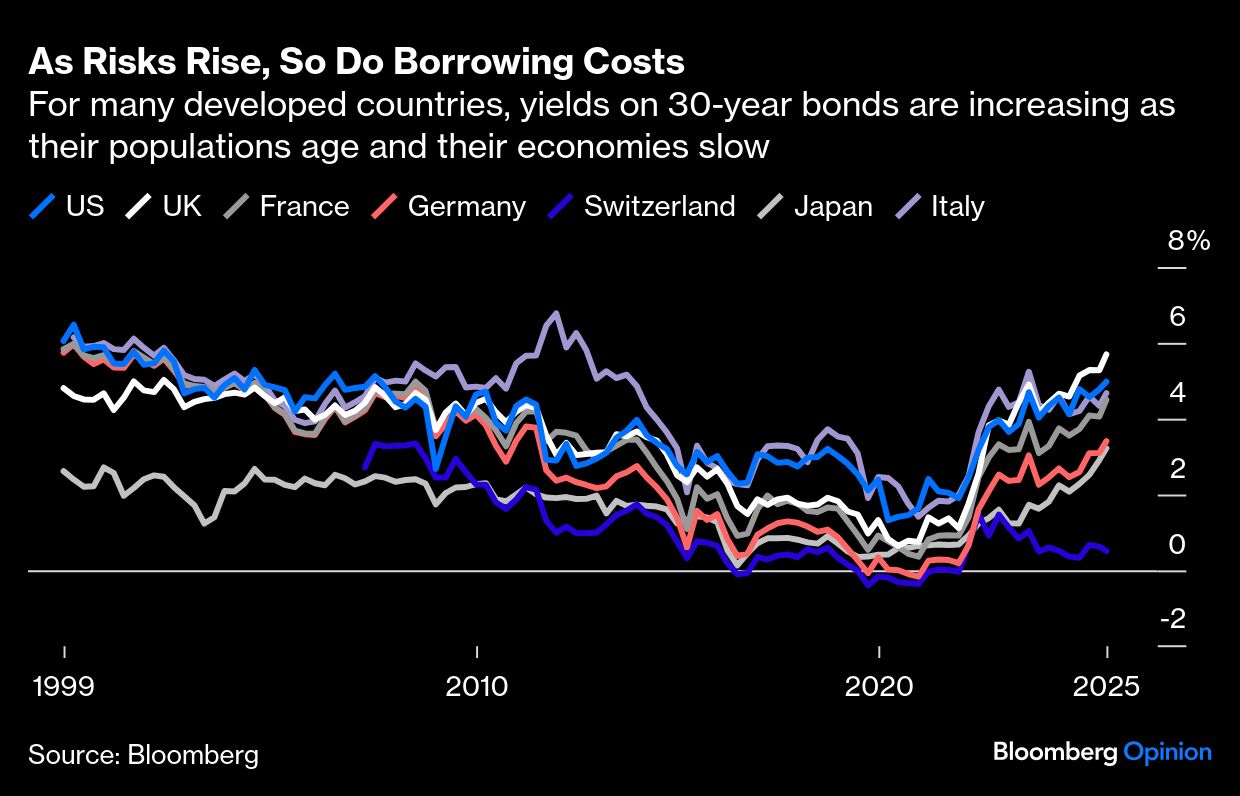

Rates have finally gone up in the last few years. Now the 30-year bond yield is rising in almost every rich country, except for those relatively prudent Swiss.

Most of the action is on the 30-year bond, which some see as a reassuring sign that a crisis is not imminent. After all, most credit is based on shorter-duration bonds. And while rates of about 5% may seem high, from a historical perspective they are not; the 30-year US yield is about one-third of what it was in the 1980s. Finally, rates have generally been higher since the pandemic, and nothing important has broken. Bond investors have had some good returns in the last year in the US as rates have remained steady, while rising rates in Europe may be less about macro panic and more about pension funds buying shorter-term bonds.

But ignore the market for 30-year bonds at your peril. Pension funds may be playing an important role by reducing demand now, but they are also awaking markets from a decades-long cognitive dissonance. There are reasons to worry, not only that rates aren’t going back down, but that they may rise even higher. There may not be a debt crisis with defaults and IMF bailouts, but global growth will probably be lower, with higher interest rates, inflation and the end of free money in developed markets.

This could be a rerun of the 1980s. Back then, yields were high because of chronic inflation and markets were still adjusting to the new global financial world brought on by the end of the Bretton Woods system of exchange rates.

Today, the dollar’s future as the reserve currency is looking a little iffy, and globalization seems to be on the wane. It is also concerning that long-term rates are rising as the European Central Bank is cutting — and the US Federal Reserve is expected to cut rates, too. Longer-term rates are a function of what markets expect future short-term rates to be. That they are rising despite rate cuts from central banks means that the risk outlook is worse.

And it is not like things are going to get better. The US, Japan the UK and many countries in Europe all are carrying lots of debt, with no serious plan to cut back. None of these countries has a viable plan to increase growth — unless you count “AI will increase productivity across the entire economy” as a growth plan. Maybe AI will do that, but policy makers aren’t helping by increasing regulation, as higher interest rates increase the cost of capital.

The last few decades of low rates lulled investors, companies and governments into believing that they could keep borrowing and not face any costs — that they could essentially live in a world without economic trade-offs. Higher rates mark the end of this era of magical thinking.

That’s not to say investors who bet against bonds will be redeemed — as always in markets, timing matters more than being right. But at the very least, this week’s bond market is redeeming the arguments for economic growth and fiscal prudence.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.