Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

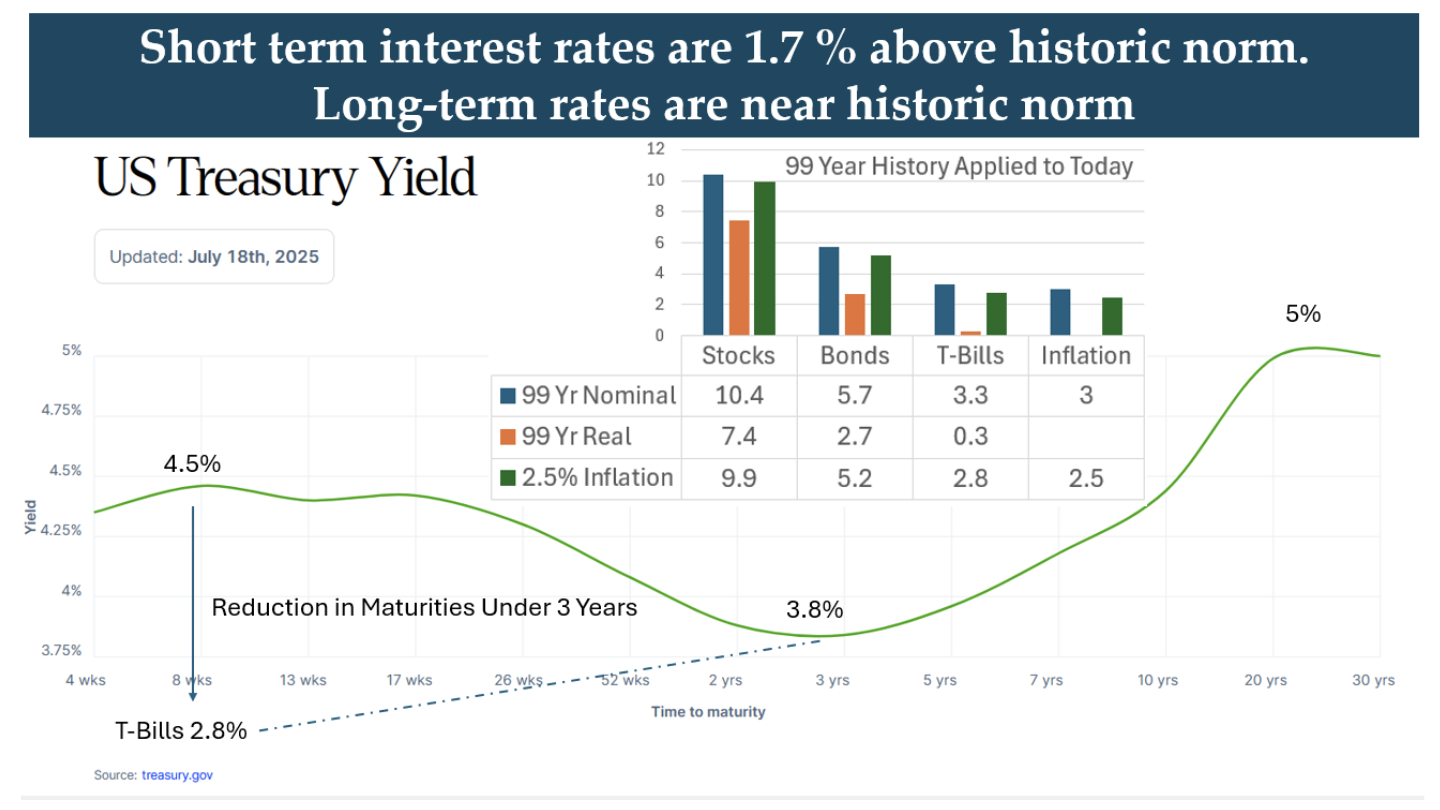

- Interest rates on Treasury Bills are currently 1.7% above their historic norm, supporting President Trump's call for rate cuts.

- Long-term Treasury Bond rates are in line with historical averages, suggesting no need for adjustment at the long end of the curve.

- The unusual U-shaped yield curve reflects investor concerns about tariffs, boosting demand for intermediate maturities.

- If inflation stays around 2.5%, short-term rates have room to decline, benefiting investors in short-term government securities if Trump's view prevails.

Is President Trump correct in his assertion that interest rates need to come down? He presumably wants to stimulate the economy, but doing so risks exacerbating inflation, especially if the economy doesn’t need stimulation at this time.

Let’s look at the 99-year history of capital market returns spanning 1926–2024 as our guide. Over this time period, Treasury Bills earned a mere 0.3% above inflation and Treasury Bonds earned 2.7% above inflation.

The following graphic shows how the current situation stacks up against history:

Applying the long-term Treasury Bill 0.3% premium to the current inflation rate of 2.5%, we say 2.8% is the “norm.” But T-Bills actually yield 4.5%, which is 1.7% above the historic norm. Treasury Bill rates are high by this standard. One point for the current administration.

Long-term Treasury Bond rates at 5% are in line with historic norms. And Bond King Bill Gross expects these rates to remain at or above current levels.

Note also that intermediate term bonds are lower yielding, creating an unusual U-shaped term structure that is likely due to investor concerns about the effects of tariffs in the near future that have increased demand for these maturities.

Shape Shifting

Based on history, short-term interest rates have plenty of room to decline if inflation remains around 2.5%. Intermediate and long-term bonds are currently near historic norms, so there’s no need for adjustment. The Fed controls the short end of the yield curve by setting the Federal Funds Rate, and it has stepped in on the long end by buying these bonds to control interest rates there. The good news is that the Fed won’t need to step in on the long end again. Assuming the Fed cuts rates, reductions in short-term government T-bill yields will put the yield curve near historic norms.

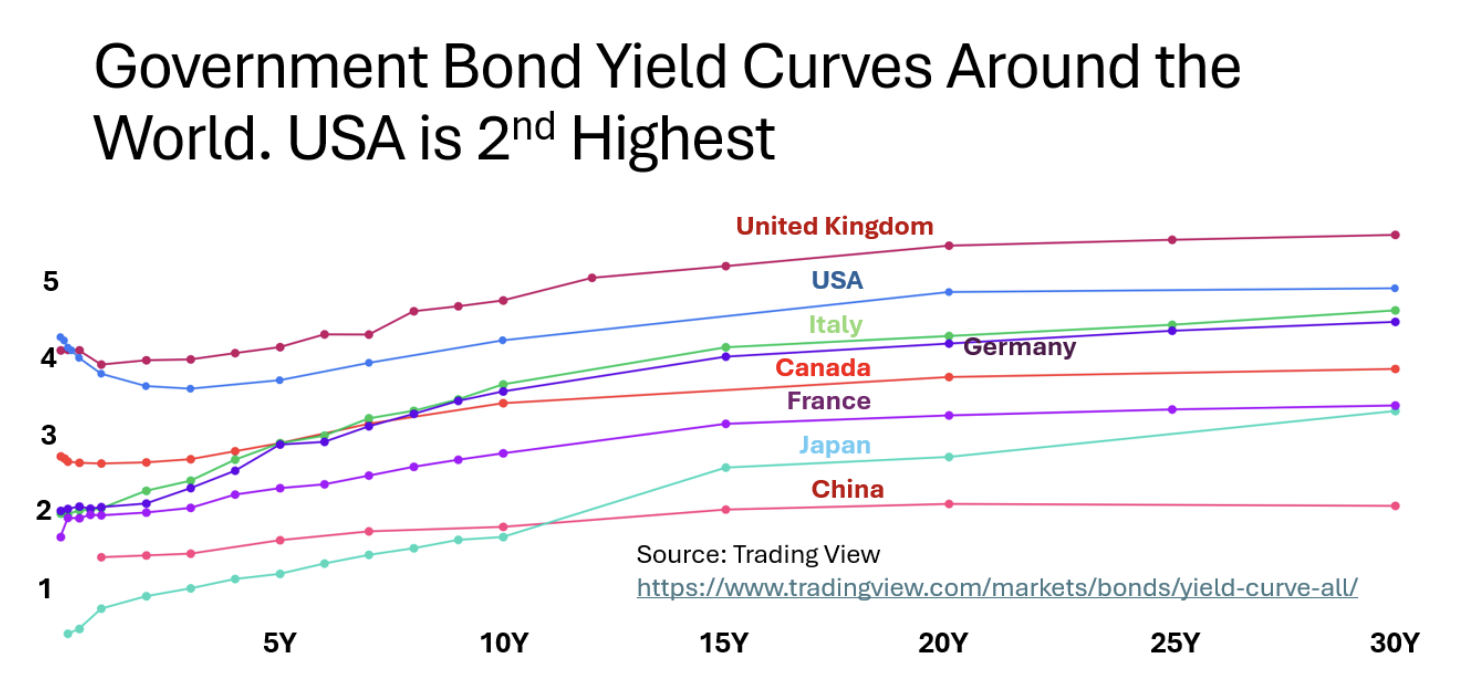

Government Bond Yield Curves Around the World

Lowering interest rates could drive investors to seek higher returns in the safe government bonds of other countries, so let’s take a look at current yield curves around the world.

As you can see, the government bonds of the United Kingdom are the only ones priced to yield more than U.S. government bonds, so they are the only bonds that currently compete on yield with the U.S. Although several countries have higher credit ratings than the U.S., Japan and China are not among them. As a result, it appears that there is room on a global basis to lower the interest paid on U.S. government bonds while still maintaining a competitive edge.

Conclusion

Investors counting on the Trump administration to prevail should expect short-term interest rates to decline, creating capital gains on these maturities. The rest of the yield curve might not be affected at all.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

For anyone who relies on TDFs — or advises those who do — Surz’s new book is a must-read guide to understanding the risks, solutions, and future of a secure retirement.

A message from Advisor Perspectives and VettaFi: Ready for your next career move? Explore our articles on financial advisor transitions.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.