Companies are moving some of the excess cash on their books into longer-term securities, betting that rate cuts from the Federal Reserve will make these holdings more lucrative.

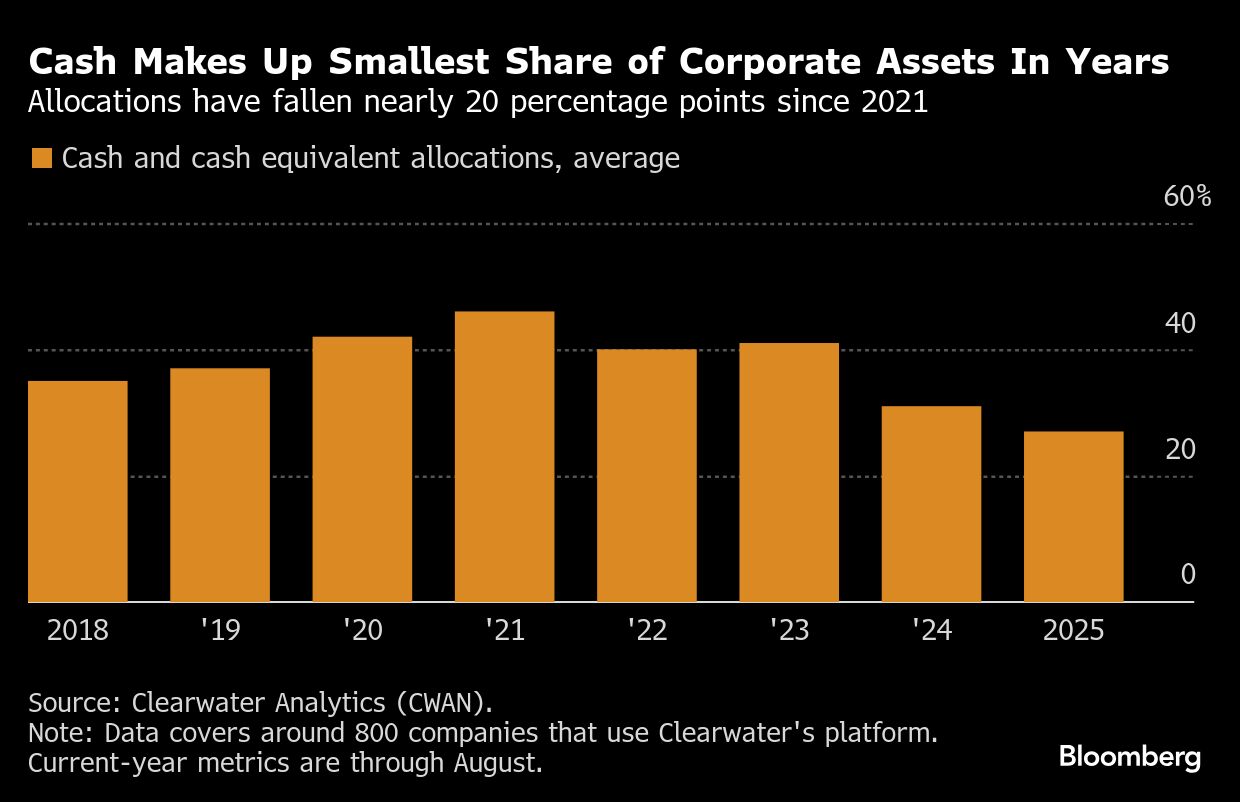

Firms this year have cut allocations to cash and other liquid investments, such as money market funds, to just 27% of holdings through the end of August, on average down about 13 percentage points compared with the end of 2022 after the Fed started hiking rates, according to investment software firm Clearwater Analytics.

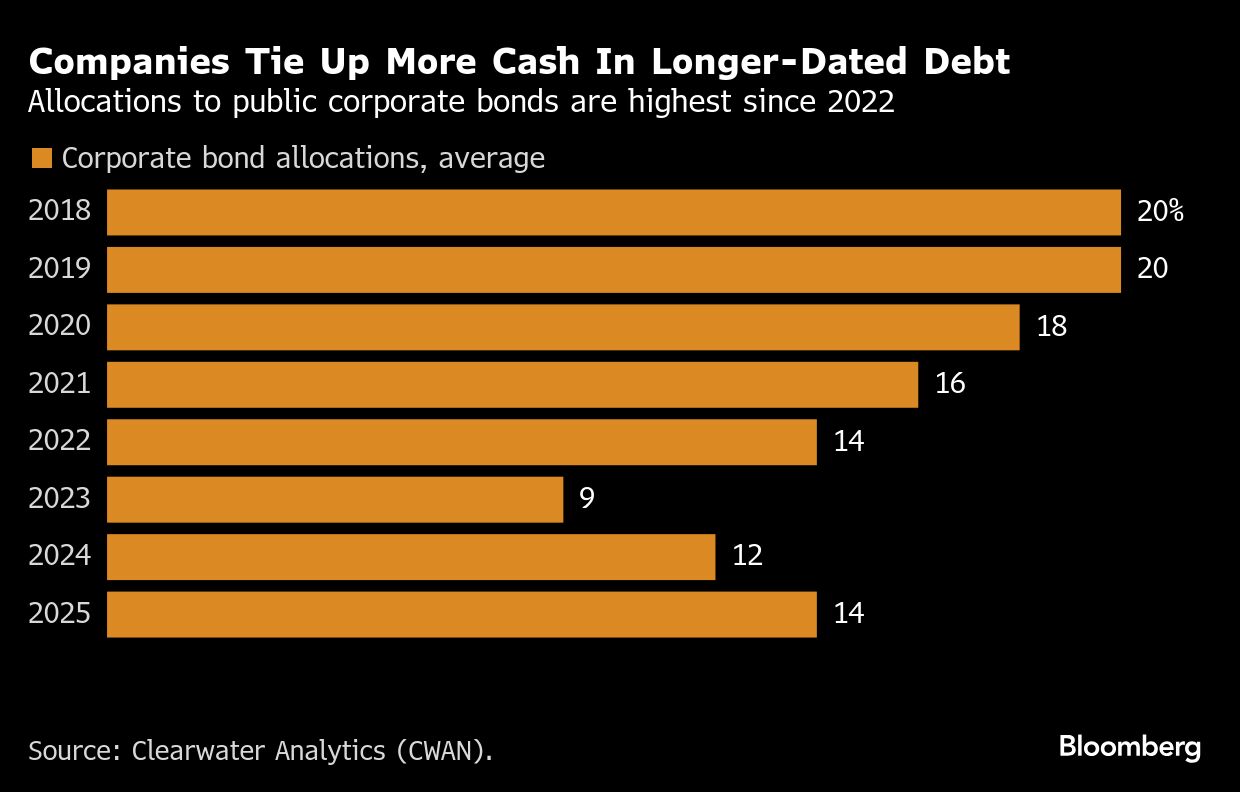

At the same time, corporate allocations to US Treasury debt maturing in more than 90 days are higher than at any point since 2018. Companies also boosted the share of corporate bond holdings in their portfolios to a three-year high, according to the Clearwater data, which covers $1.6 trillion in holdings from around 800 firms, most of them US-based.

Corporate holdings are still relatively short term, with durations averaging a little more than six months. But the shift into longer-term holdings underscores how even corporate treasurers — known for their aversion to investment risks — are gearing up for a round of rate cuts and exchanging liquidity for yield.

Market participants are currently pricing in more than two quarter-point cuts by the end of this year, including a quarter-point one at next week’s Fed meeting. Those reductions would lower the rate on short-term securities more quickly than on longer-dated ones.

“The firms that started locking in yield and duration six months or a year ago have been outperforming their peers,” said Matthew Vegari, head of research at Clearwater. “It might not be the most alluring form of revenue, but it is one of the easiest.”

Among the firms that recently made changes to their treasury holdings is Workday Inc., a California-based human resources firm. The company reduced its money market fund holdings by 19% to $802 million between January and July, while growing its allocations to corporate bonds by 12% to $4 billion over the period, according to filings.

Amazon.com Inc. in the first half of the year cut its money market fund holdings by more than $10 billion to $18.1 billion, but boosted its ownership of corporate debt by about $1.7 billion to $52.6 billion. Ridehailing firm Uber Technologies Inc. made an even bigger change, reducing its allocations to money markets by 77% to $434 million and boosting corporate debt holdings, all while keeping total assets at around the same.

Amazon and Workday declined to comment. Representatives for Uber didn’t return requests seeking comment.

“If we see a lowering of rates and a return to a normal, upward-sloping yield curve, that would probably prompt more companies to go back to this traditional approach of looking to extend duration and marginally take credit risk,” said Joseph Neu, chief executive officer of NeuGroup, a treasury advisory firm.

One asset class benefiting from companies’ willingness to take slightly more risk is private capital. This year, the companies in Clearwater’s dataset boosted their allocations to privately placed bonds from nothing to 1%, a small but indicative shift that’s emblematic of a broader embrace of alternatives to public bonds. The debt in most cases pays higher yields, but it is also less liquid and requires more oversight from investors, since there aren’t the same public indicators of risk, such as pricing indexes and frequent trading.

Rate cuts can be challenging for treasurers looking to grow their cash piles, since it means the money they have on hand will grow more slowly. Corporate cash returns have started coming down after peaking around 6% last year on a trailing 12-month basis, the Clearwater data shows. Returns were negative for part of 2022 before the Fed hiked interest rates. On the other hand, lower borrowing costs can be a boon for debt-laden firms seeking to refinance at lower costs.

To be sure, there may be other reasons why companies hold less cash now, for example if they anticipate needing their funds later than previously thought. And, most companies aren’t in the business of taking interest rate risk. Doing so is typically reserved for firms with sufficient excess cash that can afford to have some of it tied up.

And companies that add duration to their portfolios continue to invest in relatively short-dated products, just at the longer end of that spectrum. In the case of the Clearwater data, companies’ average portfolio duration of around eight months is the highest in three years.

One trend generally holds, according to the data: As market participants ramp up their rate cut bets, companies are moving away from cash. “Over the last year, investors just wanted to lock in yields, 4.5% to 5%, for as long as we could for them,” said Rich Mejzak, global head of investments for BlackRock’s cash management business.

“They weren’t caught up in market volatility, unrealized gains or losses, it was ‘Get us as much income as you can and lock it in for as long as you can,’” he said.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Ethan M Steinberg