Wall Street traders gearing up for the Federal Reserve decision refrained from making big bets as they awaited clues on the path of rates that will shape the outlook for markets over the next few months.

A solid reading on retail sales did little to move markets in early US trading, with equities holding gains and bonds yields edging mildly higher.

The value of retail purchases, not adjusted for inflation, increased 0.6% after a similar gain in July. The control-group sales — which feed into the calculation of goods spending for gross domestic product — climbed 0.7%, indicating a healthy quarter.

“The American consumer appears to be in good spirits,” said Ellen Zentner at Morgan Stanley Wealth Management. “That’s good news for the economy, but it may heighten debate over how aggressively the Fed needs to cut rates.”

While Fed officials are still focused on bringing inflation to their target, they’re widely expected to cut rates in an effort to shield the labor market from further deterioration.

“Even if the job market is weak, it’s not hurting the consumer yet,” said David Russell at TradeStation. “While these numbers won’t prevent the Fed from cutting rates tomorrow, they reduce some of the longer-term dovish hopes.”

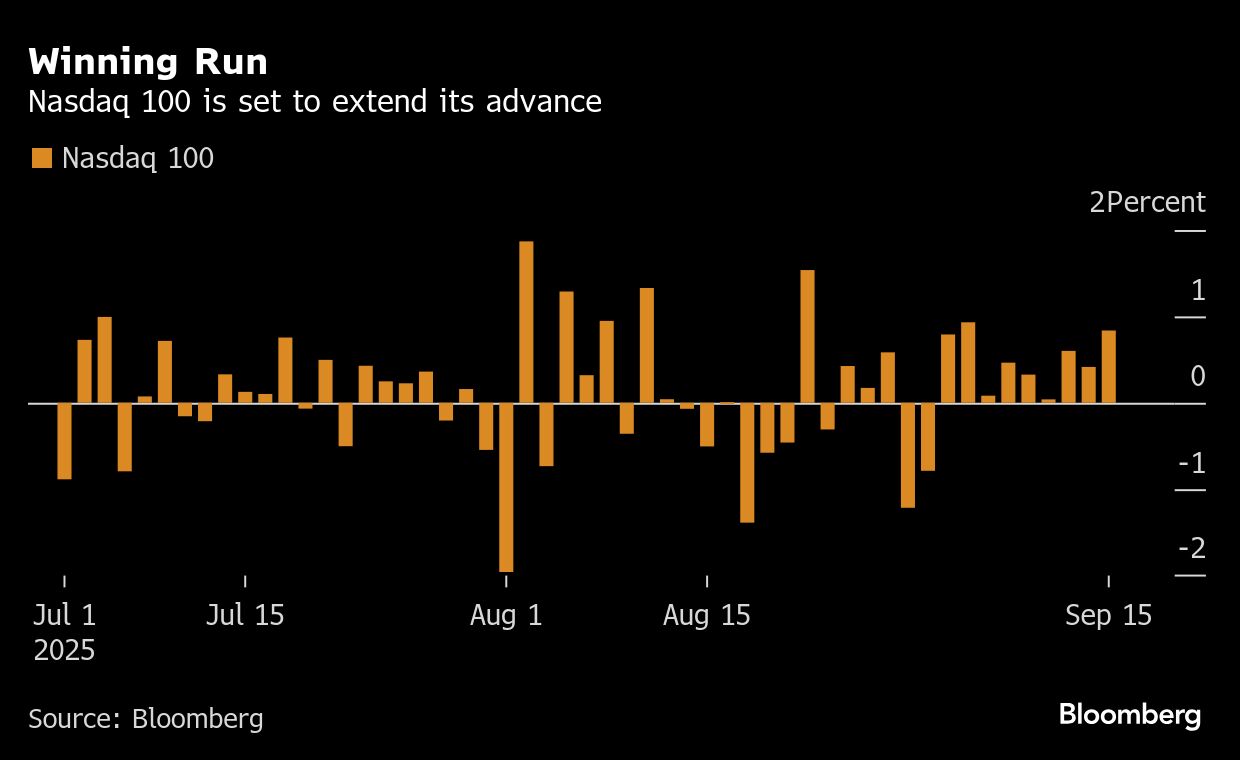

S&P 500 contracts signaled the US equity benchmark will open at a fresh record, with the Nasdaq 100 poised to rise for a 10th consecutive session. The yield on two-year Treasuries was little changed at 3.53%. The dollar fell.

To Bret Kenwell eToro, given the recent labor market data, retail sales were a big question coming into this week.

“In other words, would the recent job weakness impact consumer spending? The short answer appears to be no,” he said.

Kenwell noted that earnings estimates continue to move higher and consumer spending remains solid. Provided these tailwinds remain in place, equities can continue to perform well , even if the market takes a breather after a powerful rally, he said.

Following the latest retail sales data, Jeff Roach at LPL Financial now expects third-quarter GDP to hold above 1%, quarter over quarter.

“Further, it’s important to note that historically, risk assets perform well when the Fed starts cutting rates in non-recessionary environments,” Roach noted.

For markets, this retail sales report is another piece of good news in a string of positive data, according to Florian Ielpo at Lombard Odier Investment Managers.

“However, it’s worth remembering that much of the recent equity rally has been driven by expectations of six rate cuts over the next 12 months,” he noted. “These six cuts can only come if the job market deterioration is material and the equity performance that came with it is dependent over it.”

Bank of America Corp.’s latest survey showed a net 28% of global fund managers are overweight equities. Opinions about growth showed the sharpest improvement in almost a year.

There are “bulls galore” as the risk of a “recessionary trade war” has ebbed, strategist Michael Hartnett. wrote in a note. He added that equity exposure isn’t at extreme levels yet, which bodes well for the rally to continue for now.

Worries have been mounting that the S&P 500’s surge becoming a bubble. While critics point to the tech sector’s outsize influence on this year’s gain, it’s the rest of the market that is starting to look a bit overpriced, according to Seaport Research Partners.

An index of S&P 500 companies that excludes the technology sector has risen a solid 13% over the last year, but has seen profits grow by just 6.4%, according to data compiled by Bloomberg Intelligence. The S&P 500 Information Technology index has surged 27%, a rate that looks more restrained when put up against the sector’s earnings growth of 26.9%.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Rita Nazareth