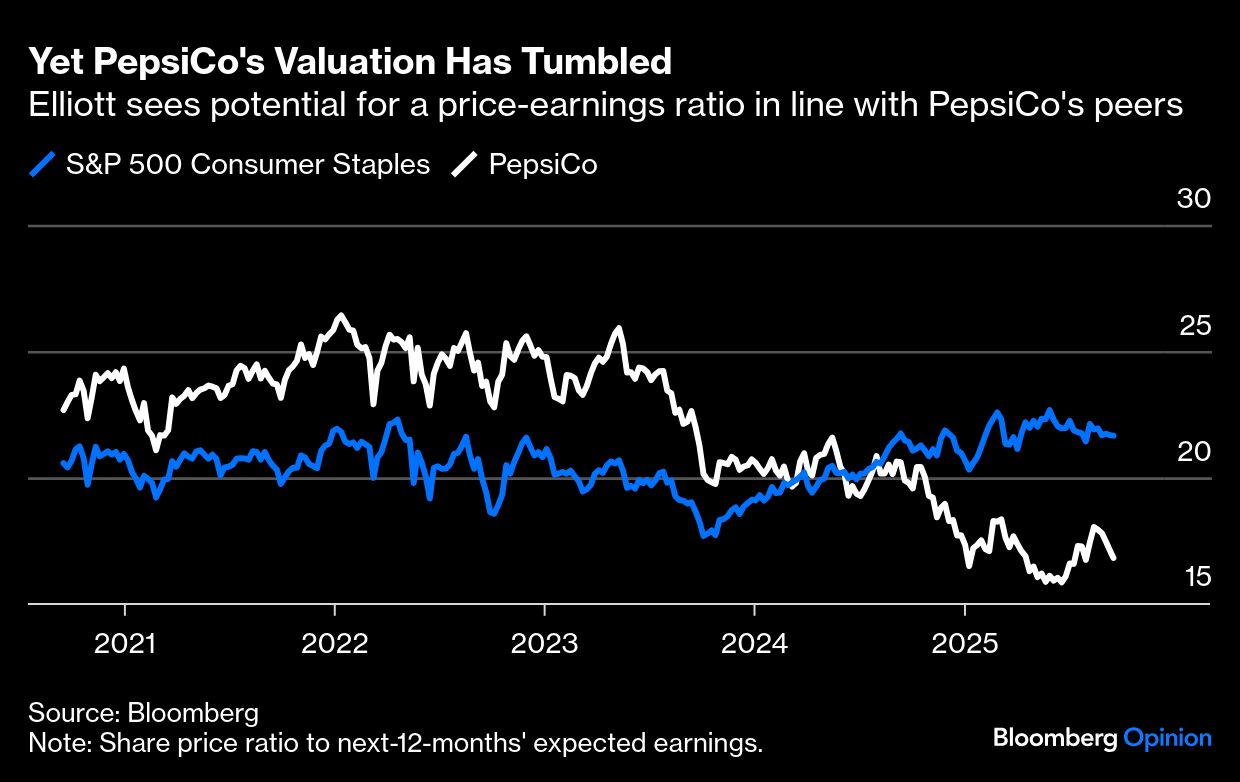

Something unusual is happening in shareholder activism. The grandmaster of the craft, Elliott Investment Management, has set out a strategy to push shares in US consumer icon PepsiCo Inc. up 50%. And yet, for all the hedge fund’s past wins, the stock has fallen. It may be no coincidence that Elliott has on this occasion kept its inner rottweiler on a leash and is seeking change (relatively) politely.

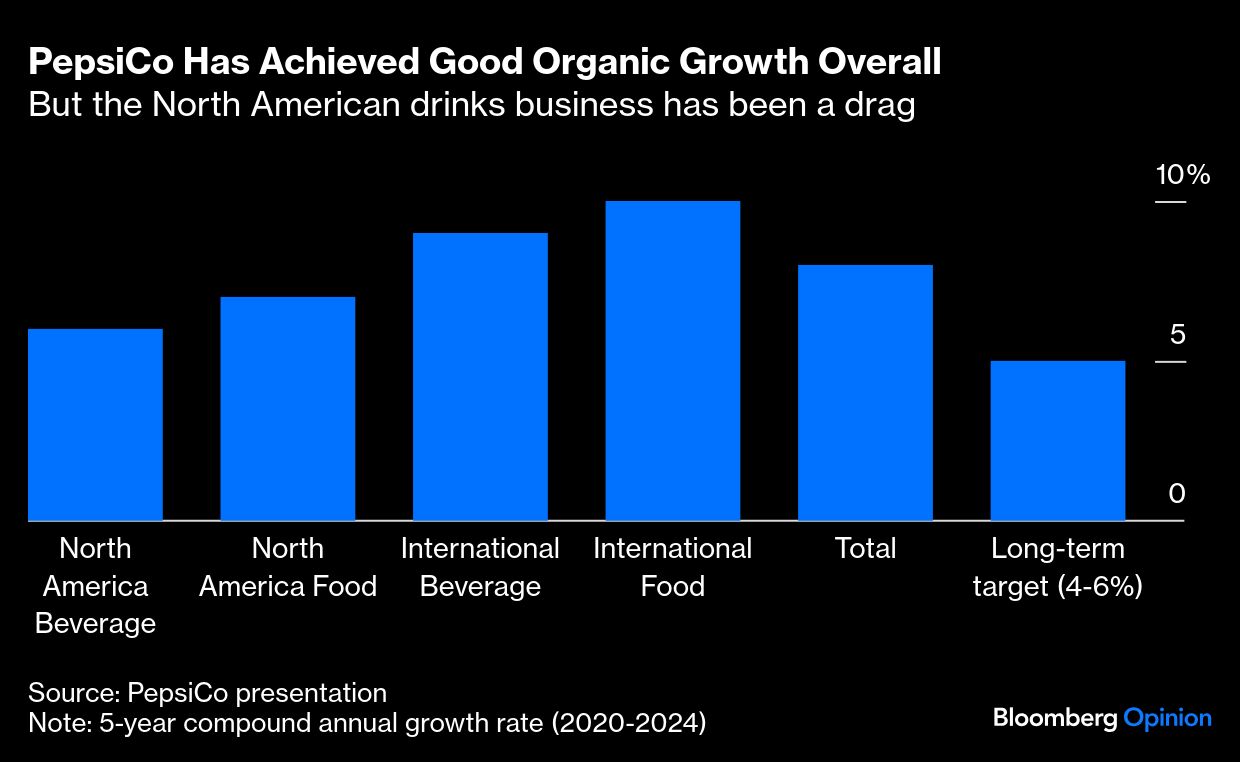

PepsiCo has seen off a powerful activist before when Nelson Peltz called for a breakup more than a decade ago. Its business outside North America is growing nicely. But recent poor performance at home has hit the stock price, reopening the opportunity to push for measures that would catalyze the kind of quick share-price revival that activists seek.

There’s one fundamental question facing the near-$200 billion company, and it’s the same one Peltz raised: Why not separate the drinks arm behind Pepsi and 7UP from the snacks business that owns Doritos and Lay’s? And yet, Elliott hasn’t called for this strategic pivot. The main demand is that PepsiCo exit bottling in North America to focus on marketing and innovation. Beyond that, it wants boilerplate cost-cutting and disposals plus simpler ranges and more investment.

Sharper management focus should fix the domestic drag on sales, supporting PepsiCo’s ambition to lift organic growth to mid- from low-single-digit percentages. Combine with lower costs and you get a powerful boost to earnings per share. Better still, the market would likely value those higher earnings on a higher multiple.

The thesis is hard to challenge for one obvious reason. The scale benefits of owning a national bottling operation just aren’t showing up in the numbers. Since PepsiCo took bottling in-house around 15 years ago, its beverage business has underperformed peers. There’s been ample time to make the model work. Coca-Cola Co. once owned bottling but switched to a franchised model — with success.

As for the rest, Coca-Cola, again, is doing great with a simpler drinks portfolio, and analysts concur there’s a sizeable cost-cutting opportunity paring back a snacks business that over-expanded.

Don’t tell, show, goes the saying. But markets are forward-looking and respond to promises. Elliott wants PepsiCo to announce a new strategy buttressed by targets, with management held accountable for meeting them. Doubtless, the idea is that the stock could begin to price in success long before improvement actually arrives.

All in all, Elliott has thrown down the gauntlet in seeing stronger margin potential and earnings-per-share growth than what’s embodied in PepsiCo’s current guidance. The consumer giant should surely seek to match the activist’s targets – even if it thinks its current strategy is the right means.

So why the market skepticism? One possible explanation is that this campaign doesn’t get to the heart of the matter. Elliott says PepsiCo has failed to respond to changing consumer trends and pursued “undisciplined growth,” in part through overpriced acquisitions. Will offloading bottling and simplifying what remains prevent such mistakes happening again?

The deterioration in the domestic drinks business was masked for many years by the success of snacks and impressive international growth. That’s a common problem with conglomerates and a strong argument for a full breakup. The benefits of focus likely count for more than the synergies in distributing soda and snacks on the same trucks. If PepsiCo’s beverages unit had its own share price providing a running commentary, its performance could not have been overlooked.

Of course, you can only successfully break up a business when the constituent parts can thrive on their own. PepsiCo is therefore not ready to do the splits just now. But the idea remains the elephant in the room.

Then there is governance. The board is unusually big, with 15 members, five of whom have served more than a decade, and three near that milestone. Coca Cola has 11 and even JPMorgan Chase & Co. has only 12. PepsiCo could well have been more nimble with a smaller, fresher board. That also needs addressing.

Is Elliott applying enough pressure? A 75-page presentation on room for improvement is embarrassing rather than painful. Elliott’s criticism is diluted by the sheer weight of analysis and its statement of “deep respect” for the company’s leadership.

It would be naive to think Elliott has suddenly gone soft. The activist has likely scored past victories by combining overt diplomacy with fierce engagement behind the scenes. The less public pressure, the more private pressure will be required. In the end, it is pain that we obey.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Chris Hughes