A $15 trillion rally in US stocks from April lows took a breather at the start of a week that will bring a handful of Federal Reserve speakers and a key inflation measure.

After notching 27 records this year, the S&P 500 barely budged on speculation that its surge has already priced in a range of positive developments such as the restart of the Fed’s rate cuts.

“Of course, there are reasons to be mindful, given the current high valuations compared to long-term averages,” said Mark Haefele at UBS Global Wealth Management. “After such a strong recent run, a period of consolidation should not come as a surprise, in our view.”

In another sign of subdued appetite for risk, the crypto world got hit as traders saw more than $1.5 billion in bullish wagers liquidated on Monday. Gold powered to a record. Silver also rose, with year-to-date gains topping 50%.

Action was relatively muted in the bond market. That’s ahead of a trio of Treasury auctions this week, including $69 billion 2-year notes Tuesday, $70 billion 5-year notes Wednesday and $44 billion 7-year notes Thursday. The dollar edged lower.

There was no sign of seasonal weakness in the first three weeks of September, but with the Fed’s rate cut in the rearview mirror, the market will be searching for fresh sources of momentum, according to Chris Larkin at E*Trade from Morgan Stanley.

“In the short term, if economic data comes in soft, it may need to be in a “Goldilocks” zone — soft enough for the Fed to continue cutting, but not weak enough to fuel recession concerns — for the market to avoid excessive volatility bumps,” he said.

Investor focus is likely to shift to the Fed’s tolerance of sticky inflation in 2026, and away from worries about a weaker labor market, according to Morgan Stanley strategists.

“Should the administration’s intention to ‘run it hot’ play out next year while the Fed cuts rates, revenue and earnings growth could come in much stronger than expected,” the team led by Michael Wilson wrote.

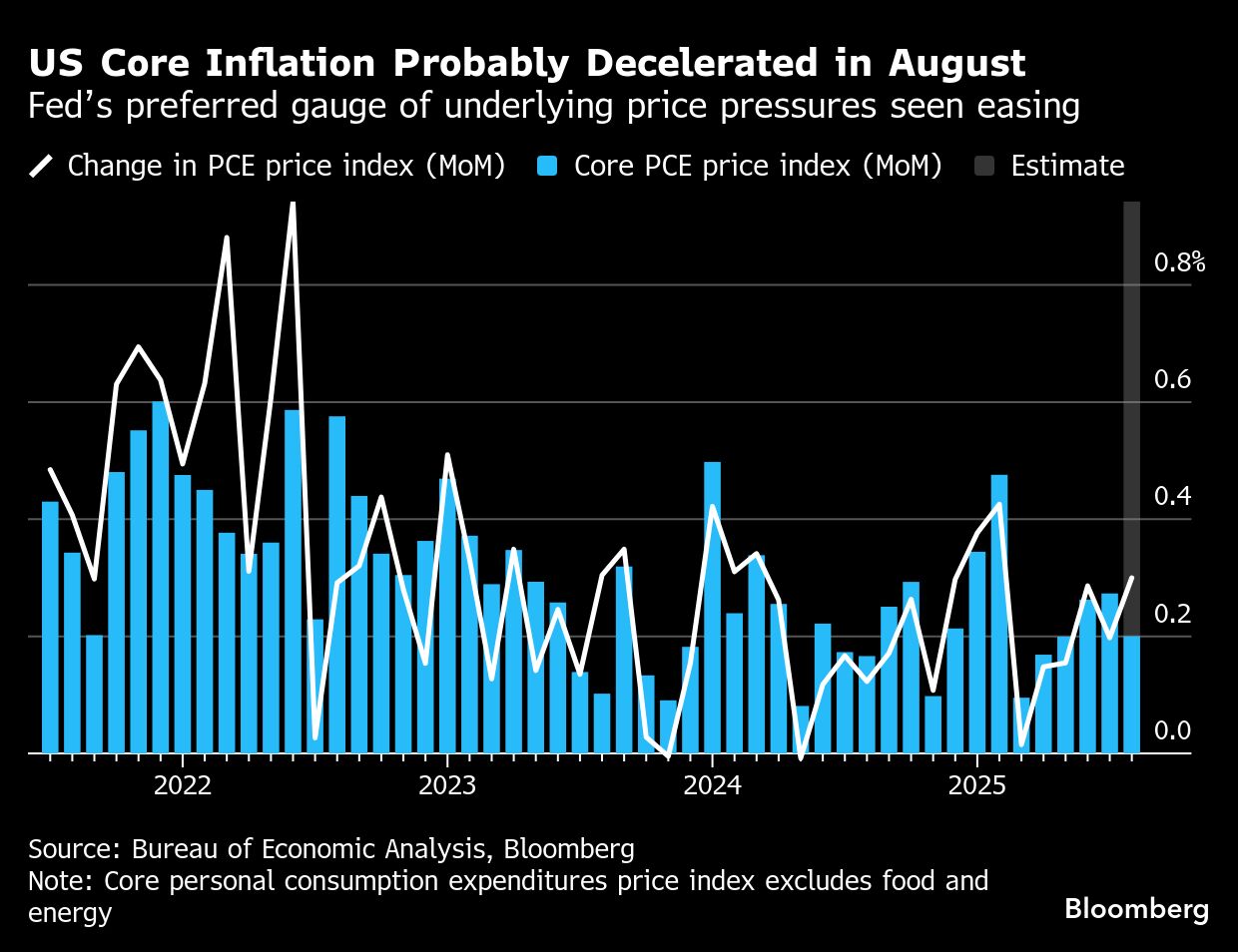

The Fed’s preferred gauge of underlying inflation likely grew at a slower pace last month, offering policymakers some breathing room to address weakness in the US labor market.

A report on Friday is forecast to show the personal consumption expenditures price index excluding food and energy rose 0.2% in August, compared with 0.3% in July. On an annual basis, the so-called core measure is seen holding at a still-elevated 2.9%.

Several Fed officials are set to speak at public events in the coming week, including Chair Jerome Powell on Tuesday. New Fed Governor Stephen Miran — on a temporary leave from his role as chair of the White House Council of Economic Advisers — as well as Michelle Bowman, Mary Daly and Alberto Musalem are scheduled to offer their thoughts on the economy.

“Fedspeak this week will highlight the wide dispersion of views on the Committee,” said Oscar Munoz at TD Securities. “We do not expect Powell to change his tone from his FOMC press conference.”

Munoz also said August PCE is likely to show gradual tariff passthrough into goods prices and moderating services inflation.

Despite the importance of PCE playing into the calculation of the Fed’s next rate decision, Rick Gardner at RGA Investments says that in the near-term, labor-market data carries more weight for the Fed than the inflation data.

“The focus for the remainder of 2025 will be more about what will drive markets in 2026, which includes earnings, the prospects of additional rate cuts in 2026, and the eventual uncertainty over the midterm elections,” he said.

Gardner also noted that the stock market’s strength is making it tougher to put new money to work, as valuations are rising, which makes it all the more important for investors to be selective and bottoms up.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Rita Nazareth