Risk parity — the investing style popularized by Ray Dalio — is quietly bouncing back.

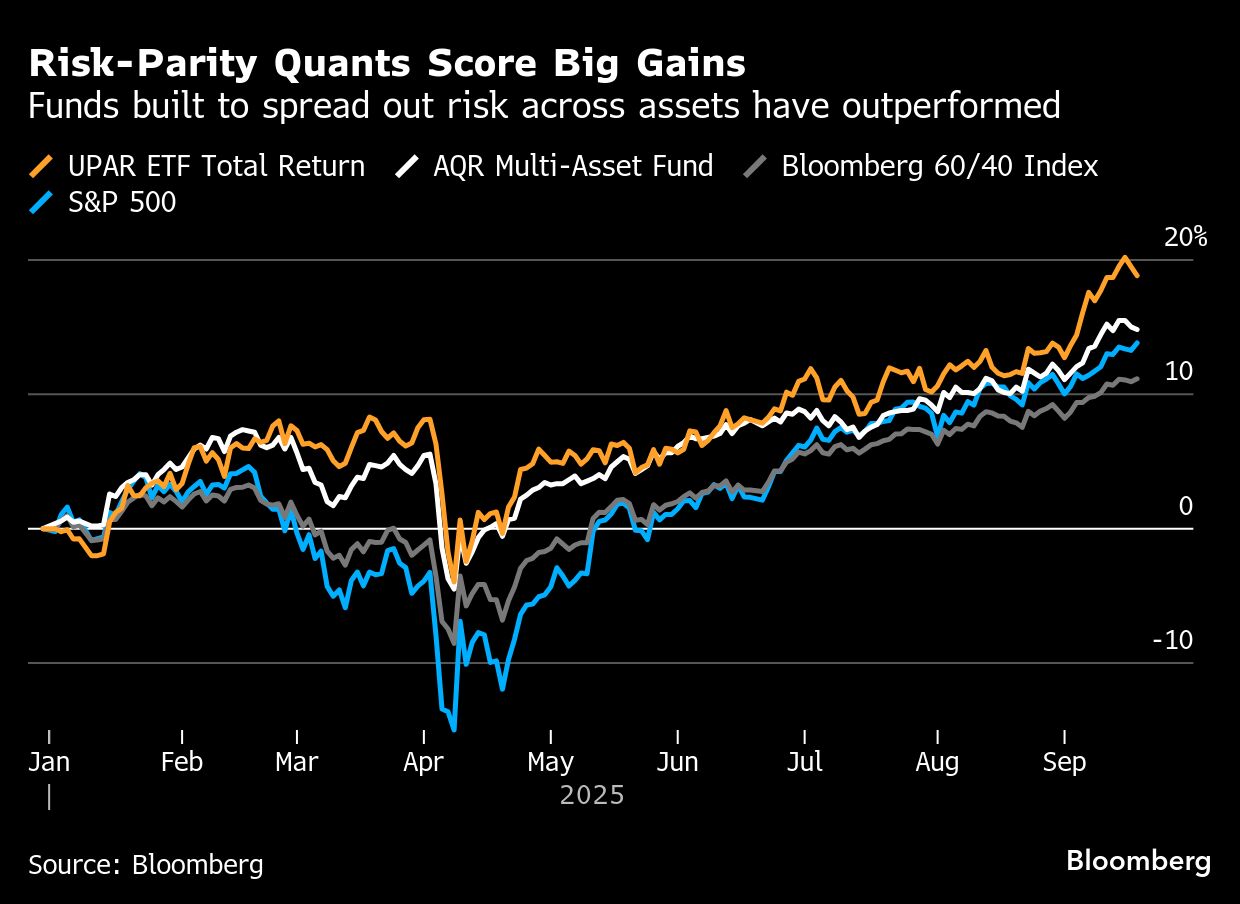

AQR Capital Management’s multi-asset fund is up 15% this year. Columbia Threadneedle’s version has returned about 12%. Even simple ETFs tracking the strategy have gained as much as 19%. For a category long seen as lagging, that’s a notable shift.

Much of the recent strength stems from fixed income. Because bonds tend to be less volatile than equities, risk parity gives them a larger role, often using leverage to balance risks in a portfolio, amplifying returns along the way. With bond prices rebounding as the Federal Reserve kicks back into easing mode that tilt has become a powerful tailwind. More broadly, the strategy’s multi-asset mix — spanning global stocks, inflation-linked bonds and gold — is delivering results, while helping investors ride out the turbulence shaking US markets under Donald Trump’s presidency.

It marks a rare moment in which diversification isn’t just defensive — it’s delivering.

That’s a sharp turn from recent years. A tech-fueled bull market rewarded concentration, not caution. Then came 2022, when stocks and bonds sold off in tandem, breaking the diversification link the strategy depends on. Risk parity faltered just when it was meant to protect. And as Big Tech powered equities to fresh highs, the approach looked increasingly out of step — more drag than hedge.

“We are finally starting to see some nice payoffs for other asset classes,” said Josh Kutin, head of multi-asset solutions for North America at Columbia Threadneedle. “Equities was really the only show in town. Diversification or even adding fixed income to a portfolio hasn’t been rewarded.”

These rules-based funds, which allocate across asset classes based on volatility, are showing signs of life after years of underperformance and investor redemptions. There are many variations on the strategy, but the basic idea is to balance the portfolio so that stocks, bonds and commodities contribute roughly equally to its risk, even if that means holding more bonds or using leverage.

ETFs like RPAR Risk Parity ETF and UPAR Ultra Risk Parity ETF are up 14% and 19% respectively. Overall, an S&P risk-parity index targeting 12% volatility is up 15% this year, outpacing both the S&P 500 and the Bloomberg 60/40 index of balanced funds. More conservatively positioned versions of the strategy have posted gains roughly in line with 60/40 portfolios. For an approach long seen as trailing, this marks a clear turnaround.

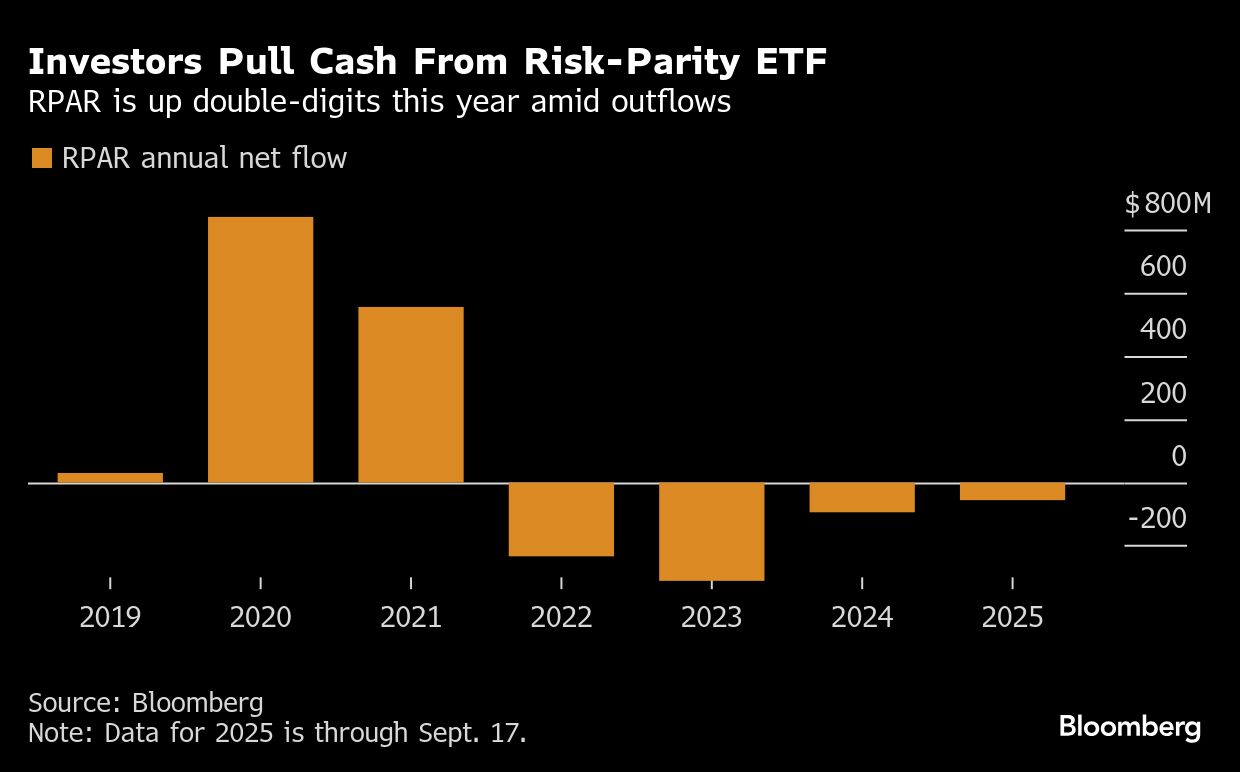

Despite the improved showing, risk parity hasn’t yet won back investor confidence. Assets remain well below peak levels. Wealthfront Inc. shuttered its fund entirely after a string of weak years.

In the ETF world, the SPDR Bridgewater All Weather ETF has reached $400 million in assets in about six months. RPAR and UPAR remain far below their asset peaks. RPAR’s assets, for instance, have shrunk to $540 million from a high of $1.6 billion.

Man Group’s portfolio manager Henry Neville argued in a recent paper that risk parity has delivered higher risk-adjusted returns than balanced portfolios of 60% equities and 40% bonds, which nevertheless have wider acceptance. In a sample that spanned the past 225 years, the Man study found that risk parity would have outperformed 75% of the time on a trailing five-year risk-adjusted basis.

The strategy grew in popularity in the aftermath of the 2008 financial crisis, attracting big inflows as investors sought a way to protect themselves from crushing selloffs. But rallying US stocks in the past decade undermined the appeal of diversified strategies.

While its core is a mechanical, rules-based approach, many funds have evolved, blending systematic risk-weighting with active security selection to navigate shifting markets. The strategy’s revival hinges less on raw returns in the short term, and more on its ability to provide a ballast to portfolios across investing regimes over the long haul.

Mixed Signals

For the past three years, Philippe Ferreira and his team at Kepler Cheuvreux have overridden their own models, bypassing signals that would have added exposure to low-volatility bonds and trimmed equity risk.

This year, he’s been more willing to follow the signals. Even so, he remains cautious. Risk-parity’s bias toward bonds “means long term it might continue to underperform a 60/40 portfolio,” Ferreira said.

In 2018, AQR rebranded one of its risk parity strategies as the Multi-Asset Fund, adding more active management after suffering outflows. The changes gave the team more flexibility on security selection and asset allocation. The fund has received about $800 million in inflows so far this year.

“We could hold an equity portfolio that has the desired equity market exposure but have it tilted towards the stocks we think are attractive,” said Jordan Brooks, a principal at AQR Capital Management. “That’s been a positive contributor.”

That global rotation is now offering fresh support to diversification-minded strategies like risk parity, according to Alex Shahidi, co-CIO at Evoke Advisors, the architect of both UPAR and RPAR.

“When you look across all those assets, this year is almost the opposite of the previous decade — where US stocks did well and everything else didn’t,” he said. “You could see that being sustained for an extended period of time.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Denitsa Tsekova