As expected, the Federal Reserve cut its policy rate on Sept. 17 by a quarter of a percentage point. Officials had signaled the move in advance and Chair Jerome Powell explained the reasoning well enough. Unfortunately, where monetary policy goes from here is anything but clear — and there’s little the central bank can do about it.

The Fed is grappling with incipient stagflation: above-target inflation combined with a stalling labor market. It has just one tool, the policy rate, and can’t achieve its dual mandate of stable prices and maximum employment if those goals pull in opposite directions. At the moment, they’re doing so thanks to White House policy: Its immigration crackdown has created a labor market shock while its tariffs have worsened the outlook for inflation.

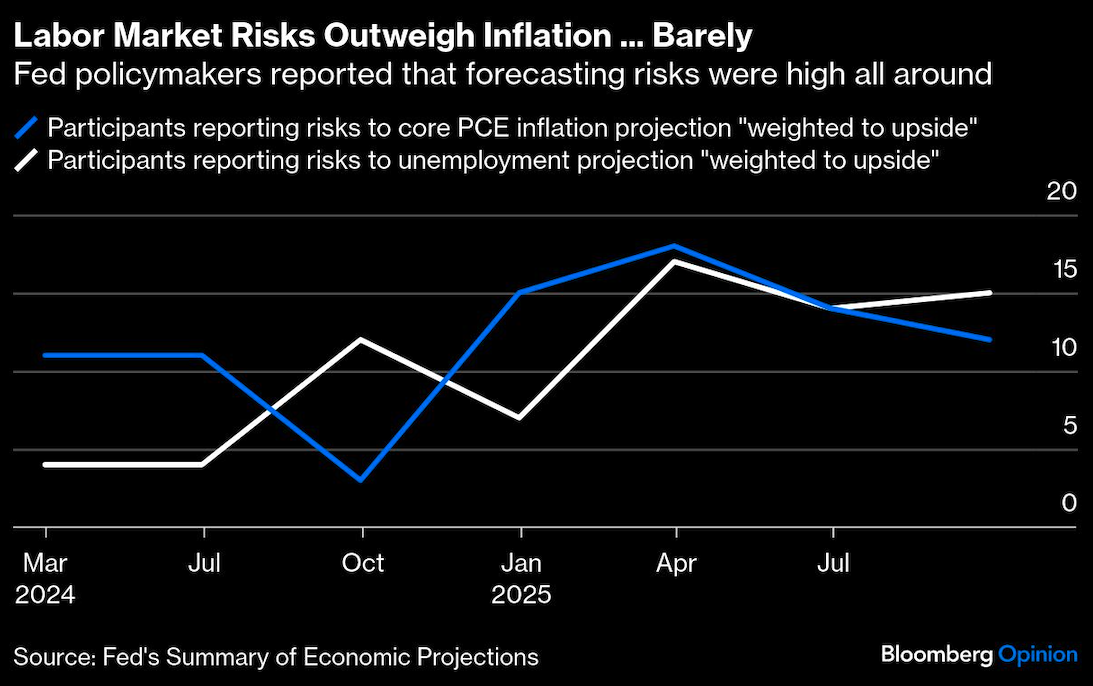

As Powell explained, the balance of risks has shifted. Hiring has slumped, so far with little effect on unemployment because the supply of labor has fallen, too. Cooling demand for labor makes a small cut in rates prudent. Yet as Powell also noted, it’s impossible to know whether further cuts will be needed. The central bank’s summary of economic projections, the so-called dot plot, indicates two more cuts of 25 basis points this year, but the spread of estimates is wide and Powell emphasized that the Fed has no fixed plan.

That’s good: Amid the current uncertainty, any such schedule would be worse than useless.

It’s also encouraging that the Fed is being criticized by inflation hawks and doves alike. Hawks note that the policymakers now expect slightly higher inflation next year (2.6%, up from 2.4%) and slightly lower unemployment (4.4%, not 4.5%), then ask why any cut in rates was needed. Doves insist that longer-term inflation expectations remain well-anchored and that the pause in hiring, which will add to unemployment if left unaddressed, demands bolder action.