In the history of Wall Street, few have been as successful as Ken Griffin. Over the past three decades, he has built his Citadel hedge fund into a global financial behemoth, helping Griffin accumulate a personal net worth of about $48 billion. So when he makes a market call, it’s worth paying attention.

This time, Griffin is taking aim at gold, saying it’s sending a cautionary message. The shiny haven metal has appreciated by about 121% since the end of 2022, recently hitting the $4,000 an ounce milestone — historically, the type of market development you might associate with inflation risks, extreme geopolitical uncertainty or even a financial crisis. Call it a “yellow flag” at this stage.

Griffin also portrayed gold’s rise as the flipside of a US dollar that is losing influence in comments Monday at a Citadel Securities conference for institutional clients in Manhattan (emphasis mine).

Gold is at record highs. And the appreciation in other “dollar substitutes” – to use that word loosely – in items like crypto for example is unbelievable. So we’re seeing substantial asset inflation away from the dollar as people are looking for ways to effectively de-dollarize or de-risk their portfolios vis-à-vis US sovereign risk.

Griffin’s comments seemed to refer to the so-called debasement trade, the idea that perceived dollar vulnerability may be fanning gains for precious metals and even Bitcoin, assets that sometimes purport to compete with the buck in the safety trade. It may be a misreading to assume that strength in gold is directly related to the dollar, particularly over the past five months.

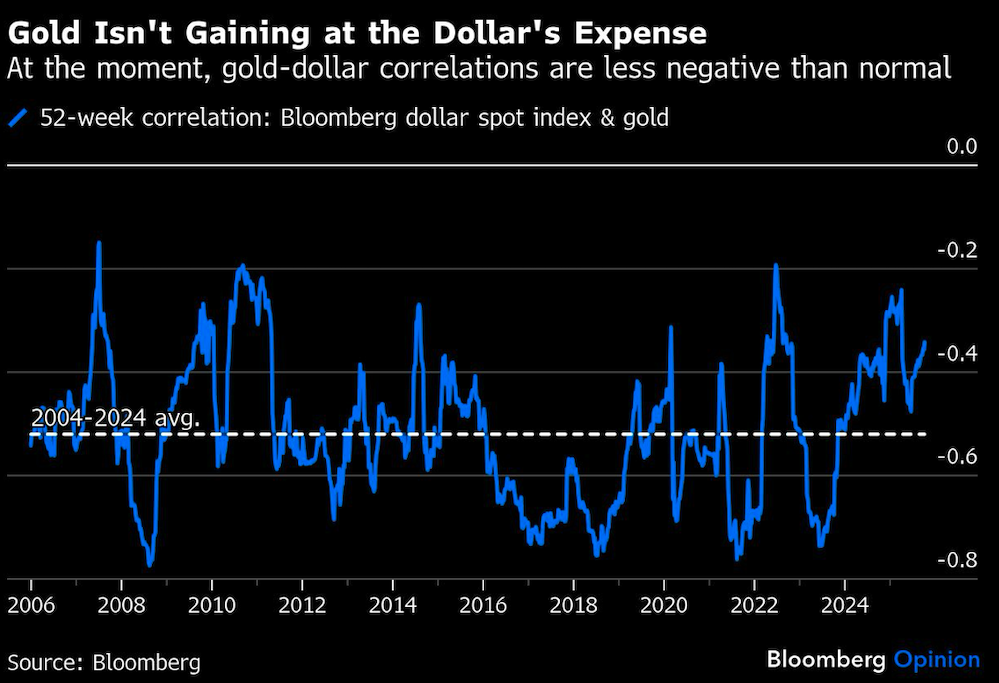

Let’s start with an overview of dollar-gold correlations, as well as some recent history. As a general matter, the buck and the metal tend to be negatively correlated, in part because, well, gold is priced in dollars. That technicality aside, there have been several periods of uniquely negative correlation in which gold seemed to make inroads as a dollar substitute. In recent times, those have included the financial crisis and 2023. Why 2023? As a response to Russia’s invasion of Ukraine the previous year, the US and its allies froze Russian central bank funds, prompting many developing-nation institutions to rethink their holdings in dollars.

Central banks still look like major buyers of gold today, but it’s no longer a new phenomenon — nor is the dollar-gold relationship uniquely negative at the moment.

What’s new is the investor enthusiasm for chasing the metal’s rally: Households and professional speculators have piled into gold exchange-traded funds lately, perhaps as a momentum trade and in some cases as a hedge against richly valued stock portfolios — a behavior that’s rather typical when massive bull markets start to feel a little long in the tooth. On a 52-week basis, gold and the dollar are actually a bit less negatively correlated now than they are on average.

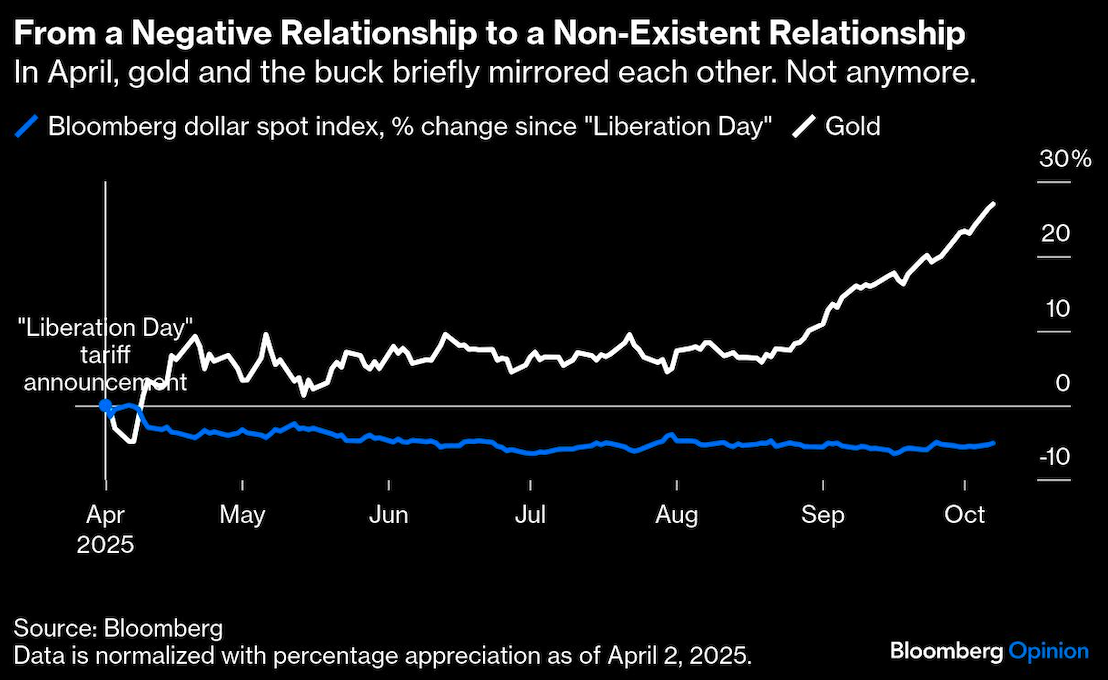

The dollar and gold now seem to be on separate journeys. The one big exception this year came after President Donald Trump’s haphazard “Liberation Day” tariff announcement — a moment that led investors around the world to at least briefly reassess America’s reliability as a global trading partner and investment destination. For around two weeks in April, gold surged as the dollar tumbled, and extreme “dollar demise” narratives briefly took hold. I too was quite concerned at the time.

But almost everything that’s happened since shows that the buck is still the undisputed champion of global currencies.

According to a new Bank for International Settlements survey, the dollar is still on one side of 89% of currency trades. International Monetary Fund data for the second quarter show that the dollar constituted well over a majority of global reserves. Even with all the April 2 chaos, its share barely budged if you hold exchange rates constant. Foreign participation in Treasury auctions has remained strong. Inflows into the US equity market have continued (albeit, with more foreigners opting to hedge currency exposure). And the dollar itself has more or less stabilized (additional wiggles in the exchange rate seem to simply reflect expectations about interest rate differentials, a totally normal state of affairs for the buck.)

Is the current setup for gold ominous? Maybe a bit. We certainly have reason to associate sustained gold rallies with terrible events in our economic history: Gold rallied in the stagflationary 1970s; the undoing of the dot-com bubble; and around the financial crisis. But large parts of those infamous rallies occurred during the economic disasters in question.

As a predictive indictor or market timing tool, gold’s track record is extremely spotty. For instance, it tripled between 2001 and 2007. Did it predict the financial crisis? Doubtful. And even if it did, what was the right moment to take signal from gold’s strength? 2005? 2006? 2007? Now, gold is up around 121% since 2022, but it isn’t clear that such information provides actionable insight for the here and now.

None of this suggests that we should ignore the risks around us. In Griffin’s case, his big concern seems to be a resurgence of inflation that markets aren’t prepared for. “There’s a sense of almost inevitability that the inflation genie is going to go back in the bottle,” he said Monday. “But I think that’s a very premature conclusion.” He added that immigration policy (read: tighter labor supply), fiscal policy (consistently sky-high peacetime deficits) and monetary policy (a recent interest rate cut to guard against labor market weakening) seem to be fostering a “very pro-inflationary environment.”

It’s wise to move carefully to ensure that we have fully slain the inflationary dragon. But, I believe that the Federal Reserve will ultimately do just that, provided it’s allowed to continue operating independent from executive branch influence. The “move cautiously” mindset has been borne out by a series of Fed speeches since the September rate cut.

Likewise, White House officials can’t forget that the sterling reputation of America’s currency and markets was earned over many decades, and they should be careful not to put it at risk with overly aggressive trade tactics, which offer little upside, and attacks on the independent central bank.

For now, the last few months have shown that the dollar continues to be as indispensable as ever. So while gold’s rally is noteworthy in its own right, there’s very little risk that the metal somehow portends a fading of the dollar’s dominance in the world.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin