All’s fair in love and politics — and international bank capital rules. US financial watchdogs are making mischief with European standards that give lenders relief by treating the euro zone as a single domestic market. The Americans have a point: The bloc is not a single market for banking and that’s been a problem when things go wrong. But they doubtless have an ulterior motive born of the political obstacles to reforming some of their own rules to help big US banks compete harder with their European peers.

The heart of this brewing battle, first reported by Bloomberg News, is the extra capital charges placed on globally systemically important banks – or GSIBs — that amount to of billions of dollars and euros in equity supporting the financial system. These massive lenders pose greater risks to economies around the world because of their sheer size, their importance to payments and money flows, and how their multitude of interconnections across markets means they can spread instability like a virus.

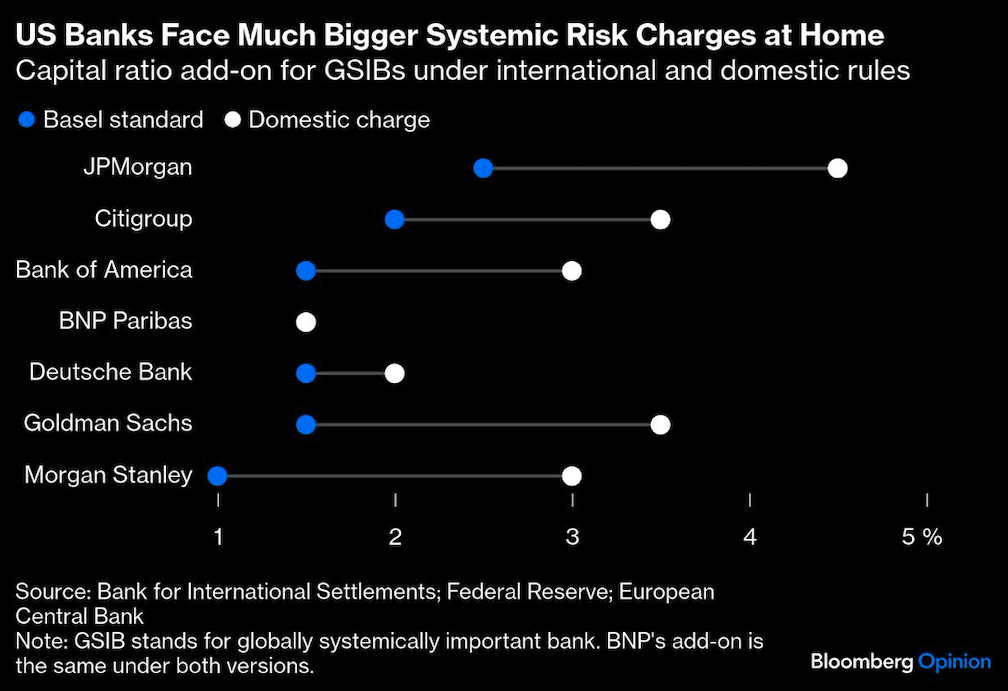

The biggest banks have had to clear higher equity hurdles since regulations were strengthened following the 2008 crisis. Europe calculates this so-called GSIB buffer using the method set by the Basel committee on international banking standards. The US uses its own method, which was badly designed in a way that means the charge increases as the economy grows almost no matter what banks do. American banks hate it, but a proper rethink looks like far too big a giveaway even under the Trump administration.

In the international method, GSIB banks are assessed for their riskiness – and the extra capital they need – using five scores, including one based on cross-border fundraising and lending. Treating the eurozone as a single jurisdiction automatically cuts that risk.

BNP Paribas SA of France was definitely helped when Basel standard setters recognized Europe’s Banking Union in 2022. When GSIB scores were calculated that year using financial reports from 2021, BNP and several others saw a drop in their cross-jurisdictional exposure rating. For the French lender that was enough for supervisors to lower its overall classification, according to the Banque de France, and reduce its minimum capital ratio requirement by half a percentage point – a significant boost for such a big bank. Reversing that today would cost BNP about €4 billion ($4.7 billion) in extra capital.

Other big Europeans, such as UniCredit SpA of Italy, have seen some benefit too, but lenders like Deutsche Bank AG and Banco Santander SA with more important links outside of Europe have not.

Federal Reserve officials are seeking to get this border-free treatment of the euro zone reversed – and to be fair it is a bit of a joke. European banks complain regularly that the banking union is still more a fantasy than a reality. There is no Europe-wide deposit insurance; cross-border lending within Europe remains limited, and both capital and liquidity get trapped within national subsidiaries of the biggest European banks, according to a recent report by the Association for Financial Markets in Europe, a lobby group. This fragmentation arguably increases costs and risks. Cross-border bank deals are also all but impossible.

US officials picked the perfect time to start this fight. It’s the first anniversary of a major report by Mario Draghi, former head of the European Central Bank, which warned the lack of euro zone integration in finance, industry and security left it vulnerable to being pushed around by the US and China.

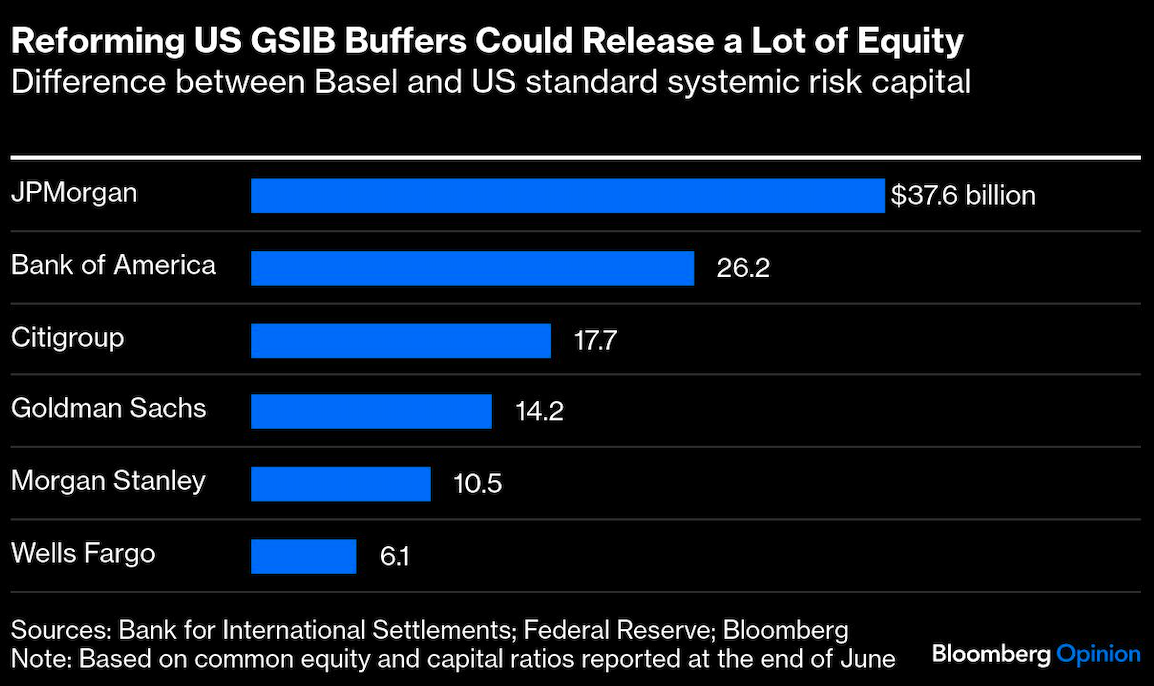

American banks want the GSIB charges evened up between themselves and big European peers. The biggest difference would be to get wholesale reform of their domestic rules, which are significantly more punitive than international standards. The problem with that is the simplest, most logical change – moving to the same method as everyone else – would release so much equity capital in one go that it looks politically impossible — especially as other relief giving reforms are happening at the same time. The difference between the US GSIB buffer and the internal one is worth nearly $40 billion of equity for JPMorgan Chase & Co. alone, and another $26 billion for Bank of America Corp., based on second-quarter results.

What makes the US GSIB calculation so painful is that it’s mechanically linked to economic growth and so each bank’s supposed riskiness simply rises with gross domestic product. A real measure of changing risk would judge whether a bank is expanding faster than the economy, or compared with rivals, which is more like how the international method works.

When the US rules were written, officials pledged to rebase the economic aspect regularly to ensure banks weren’t hit with ever increasing GSIB buffers. But that never happened and the charge kept escalating. Bank executives are hopeful that Trump’s deregulatory bent will bring some relief, but probably not enough to match those big Europeans.

This is a fluid moment for capital rules globally: We’ve entered an era of simplification and the likely dismantling of some safeguards. If allowed to run too far, that risks disaster down the road. Still, I have sympathy with US banks’ GSIB complaints and the obstacles to getting it changed. If they can’t get help at home, it makes sense to try and scuttle their rivals abroad instead.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.