A lot of people are watching this meteoric US stock market with amazement as it shakes off one worry after another – slowing labor market, sagging consumer sentiment, continuing trade uncertainty, geopolitical tensions and now a US government shutdown – on its way to new record highs. Some see a replay of the late 1990s internet bubble, this time fueled by artificial intelligence. Investors seem to be asking, in various ways, if this rally is overdone, and by implication, if the market is due a pullback.

One answer is that stocks only care about one thing — earnings growth. From that limited perspective, the future looks bright. Wall Street analysts expect that 95% of companies in the S&P 500 Index will grow earnings next year, by an average of 16%, according to estimates compiled by Bloomberg.

Most impactfully, the eight biggest companies in the index by market value — the Magnificent Seven and Broadcom Inc., which collectively account for 37% of the S&P 500 — are expected to grow profits by an average of 21%. So long as that growth isn’t in jeopardy, nothing else really matters.

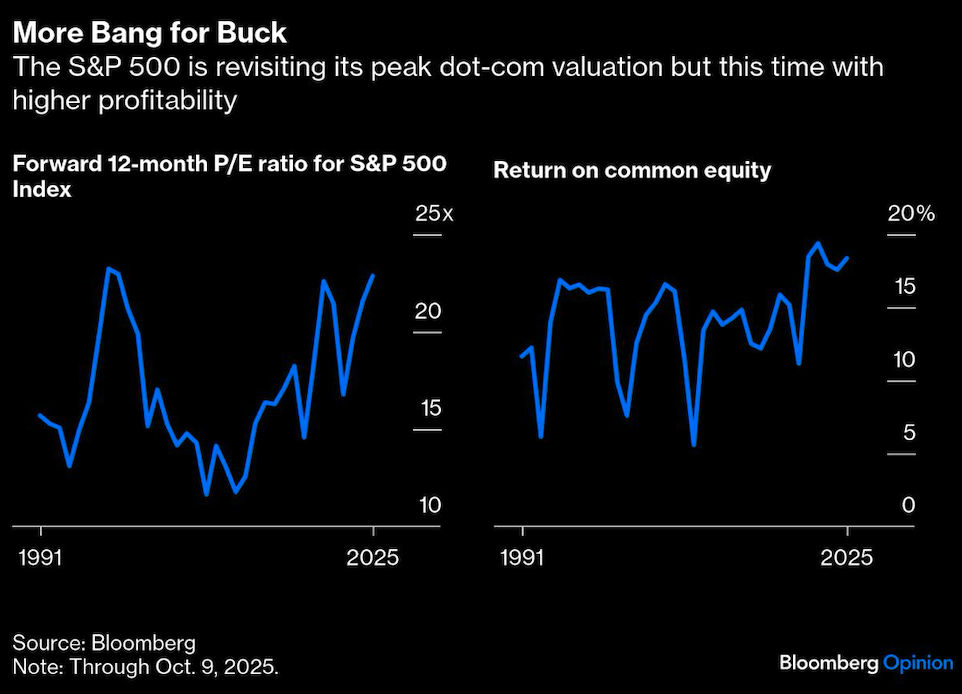

Investors are also getting more for their money than they did in the dot-com days.

Annual profitability for the S&P 500, as measured by return on equity, has been higher the last four years, at around 18%, than at any time since at least 1991. And with less leverage: The index’s debt-to-equity ratio is near 100% from more than double that in the late 1990s.

Much of that improvement is attributable to the Magnificent Seven and Broadcom, which posted a weighted-average return on equity of 68% last year — more than double that of the biggest eight companies at the peak of the dot-com bubble in March 2000. As a group, today’s market leaders also carry nearly half as much financial leverage as the dot-com cohort.

Profitability fuels earnings growth, which is what ultimately pushes stock prices higher. It’s why investors usually pay a premium for more profitable or faster growing companies.

The forward price-earnings ratio of the S&P 500 Growth Index, for example, has almost always been higher than that of the S&P 500 Value Index since 2001, with an average premium of 5 points over that time. Today’s market is not as screamingly expensive as the dot-com one once you’ve accounted for the higher profitability — and expected growth by extension.

Still, on an absolute basis, the market’s valuation is near the dot-com peak. If companies want to hang on to these lofty multiples, they’ll have to deliver. The likelihood depends largely on how much growth the market expects. Growth expectations can’t be observed directly, but there are clues.

Wall Street analysts expect S&P 500 earnings to grow by 10% a year over the next three to five years, based on individual company estimates compiled by Bloomberg and weighted by companies’ market value. That’s probably too optimistic and certainly well higher than the index’s long-term earnings growth of closer to 7% since the 1950s. Growth estimates for the market leaders are even rosier, in the mid-teens for most of the Magnificent Seven and closer to 40% a year for Nvidia Corp. and Broadcom.

The market has its own, more sober forecast. Another approximation of companies’ expected earnings growth is the difference between their cost of equity – essentially, the return investors demand to own shares – and their earnings yield. As things stand, the S&P 500’s weighted-average cost of equity is 10%, and its forward earnings yield is 4.4%, implying medium-term earnings growth of 5.6% a year. For the Magnificent Seven and Broadcom as a group, the implied growth rate jumps to 8.6%.

The market’s more modest expectations are very achievable but not necessarily bullish for medium-term returns. If companies deliver what’s expected, and the market rewards them by maintaining their elevated valuations, investors should collect their 5.6% earnings growth in addition to the S&P 500’s dividend yield of 1.2%, for a total return of about 6.8% a year. That’s less than half the S&P 500’s total return over the past decade.

But regardless of what happens in the next several years, AI is likely to pay off big for long-term investors. That’s an often-forgotten lesson of the dot-com era.

If you had bought the S&P 500 at the peak of the bubble in March 2000 and hung on all this time, your investment would have grown sevenfold, including dividends. And if you had bought the index as the internet emerged in 1995 and ignored the hype and doomcasts along the way, your money would have ballooned 26-fold.

Despite the endless arguments about the future of AI — the same squabbles I heard about the internet three decades ago — I have no doubt AI will be at least as transformative and valuable, and that much of the value will end up in investors’ pockets. Those scared off by elevated valuations in recent years have already given up a good chunk of it. The S&P 500 has delivered 16% a year over the past five years and 15% a year over 10 years, much of it driven by Big Tech and easily beating the index’s long-term average return of closer to 9% a year.

Don’t be surprised if this market refuses to be derailed by politics or the broader economy. There’s no reason the market has to fall apart, particularly if companies continue to feed it the growth it wants.

A message from Advisor Perspectives and VettaFi: Thinking about starting your own RIA, making a move to a different firm, or specializing in a new area? Read our latest articles on financial advisor transitions.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Nir Kaissar