US manufacturing may now be at its most vulnerable after decades of ceding crucial mining and production activities to China in the pursuit of low costs and higher company profits, and robust government support will be needed to narrow the time for securing the manufacturing supply chain.

China’s threat to curb the supply of rare-earth elements, which are crucial for making goods from autos and aircraft to headphones and vacuum cleaners, is a symptom of riding for too long the peace dividend after the Soviet Union’s collapse in the 1990s. The single-minded pursuit of global efficiency, supercharged by China’s entrance in the World Trade Organization in 2001, has backfired. With the clarity of hindsight, it’s easier to recognize the long game that sucked much of the life out of the US manufacturing base. As China geared up methodically to exert itself around the globe, the US was content to import low inflation and enjoy an extraordinary period of interest rates near zero.

It took a pandemic to wake up the country from its complacency and recognize the threat of a hollowed-out manufacturing sector. The recovery of US industry will take a concerted effort. Jamie Dimon, the chief executive officer of JP Morgan Chase, recognized that “we no longer have the luxury of time” in a Wall Street Journal op-ed on Monday in which he announced that his bank has created the Security and Resiliency Initiative to invest $1.5 trillion over 10 years for critical mining, energy and manufacturing, including military equipment and pharmaceuticals.

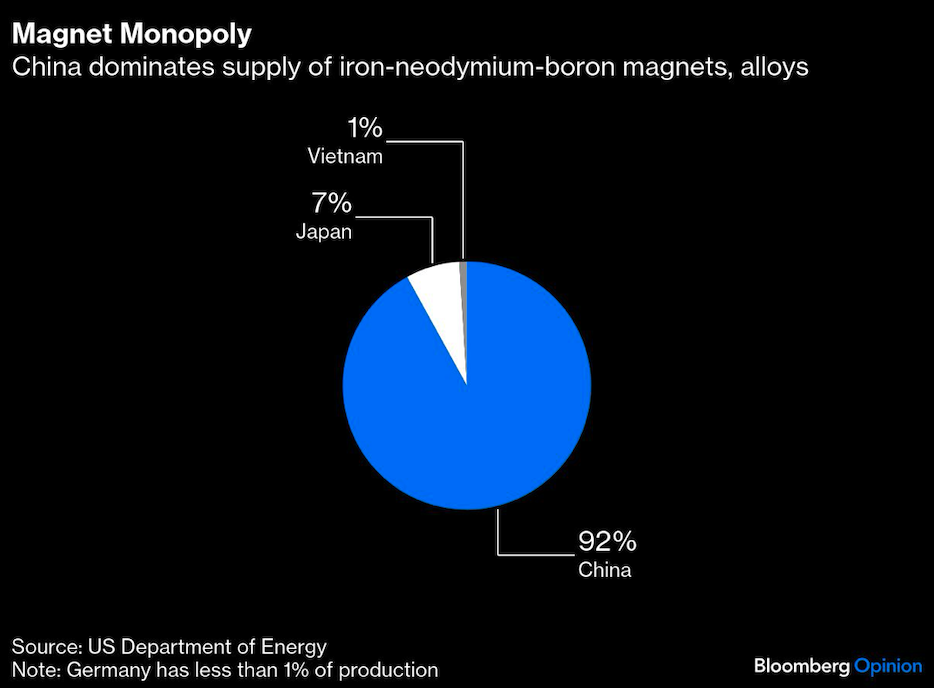

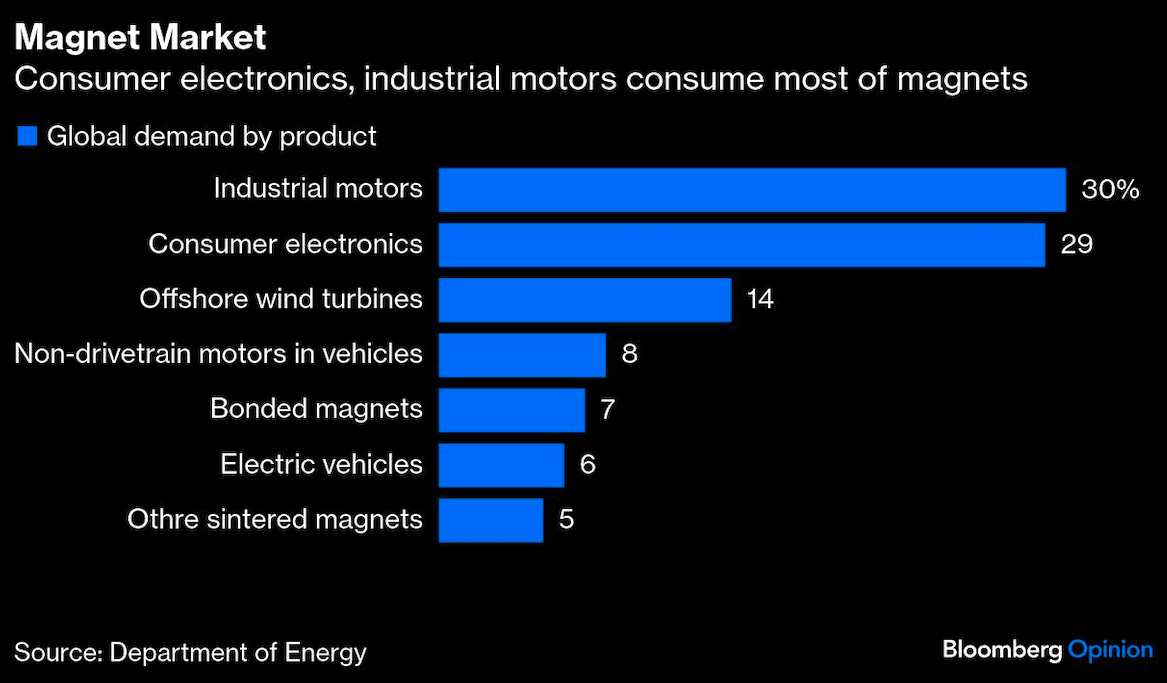

The clearest example of this threat is the supply chain for rare-earth elements. These metals aren’t truly scarce. Instead, they’re thinly dispersed in the Earth’s crust, which makes them difficult to mine. The process of filtering tons of earth to concentrate and refine these metals also involves chemicals that aren’t environmentally friendly. More manufacturing is required to turn some of these metals, such as neodymium, into permanent magnets used in many products.

The world was mostly nonchalant as China slowly gained control of the rare-earth supply chain. This wouldn’t be so alarming if China didn’t support Russian President Vladimir Putin’s savage attack on Ukraine and ally itself with Iran. Subsidies and lax labor and environmental oversight helped China undercut prices and put domestic producers out of business. Few defended domestic mining and production at the time because they were part of the old economy — the dull, dirty, dangerous jobs that a few decades ago were deemed undesirable for the new economy. And the threat doesn’t stop with mining. Even now, some are pushing for the quick demise of oil and gas as energy sources in favor of renewables that China dominates.

It turns out that the hollowing out of the manufacturing and mining sectors both hurt middle-class workers and undercut national security. Perhaps some Americans have forgotten, but Chinese leaders, including President Xi Jinping, are well aware that World War II was won on the back of US manufacturing prowess.

Fortunately, an effort has been underway in the US to build out the rare-earth supply chain from mining to magnets. At the current rate, it could take a couple of years. This pace needs to accelerate, which will require additional government support.

The Department of Defense already cut a milestone deal with mining company MP Materials Corp. to provide cash through a loan and an equity stake. More important, the deal set a price floor for the materials to prevent China from using price as a market weapon. This isn’t how a free-market economy should work, but there’s no other recourse to break China’s grip on rare-earth minerals.

This is a global problem, and countries including Canada, Australia and Mexico should be encouraged to speed up development of projects. This may require loans, equity stakes and price support, similar to the MP Materials deal.

For example, the Trump administration will build a 211-mile road in Alaska to open the remote Ambler Mining District and took a stake in Canada’s Trilogy Metals, which seeks to mine for copper, cobalt, gallium, germanium and other industrial metals. The department also provided a loan and took a stake in Canada’s Lithium Americas Corp. to jump-start the Thacker Pass lithium mining project in Nevada.

This last project bumps against the fine line of what constitutes a national security issue. Certainly lines were crossed by President Donald Trump’s badgering of Intel Corp. to hand over a 10% stake and the arm-twisting of US Steel Corp. to give the government a golden share. Trump seems to believe he’s getting a good deal for taxpayers by bullying companies into ceding ownership. It’s an unhealthy precedent that should be opposed by everybody, especially those who decried the US auto-industry bailout after the 2008 global financial crisis.

The need to develop rare-earth mining and refining projects is distinct. China can shut down US auto plants and other manufacturers by withholding minerals and industrial magnets. Still, the government stakes in these projects and price supports should be temporary and unwind once China’s stranglehold is broken.

The current predicament of China’s rare-earth dominance is worth noting for those urging a speedy demise of oil and gas that’s plentiful in the US in favor of wind turbines, solar panels and lithium batteries for energy storage — all areas now dominated by China. Handing over US energy security to China would create an even bigger national security threat.

The uncomfortable position of depending on an adversary for rare-earth elements has a solution, and it’s urgent to shorten this period. The government support should be robust but with a clear goal of unwinding equity positions once the crisis has subsided. This period of vulnerability should also be a lesson not to become beholden to China for other key aspects of the economy.

A message from Advisor Perspectives and VettaFi: Gain exposure to the evolving digital asset landscape. Learn about CoinShares ETFs.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.