Big banks are flying. Traders and dealmakers at Citigroup Inc., Goldman Sachs Group Inc., JPMorgan Chase & Co. and Wells Fargo & Co. enjoyed a roaring third quarter while lending grew, too. Stock markets are riding high and corporate borrowing costs are aggressively close to risk-free rates. And yet, the Federal Reserve is set to cut interest rates in coming months and potentially slash capital demands for banks by billions of dollars.

The biggest banks are increasingly in the business of financing non-bank lenders and asset managers — and those firms, in turn, are right now more focused on churning assets in markets than funding fresh activity in the real economy. With worries building about an AI-driven market bubble, the central bank needs to be extremely careful not to throw unnecessary fuel onto a high financial fire.

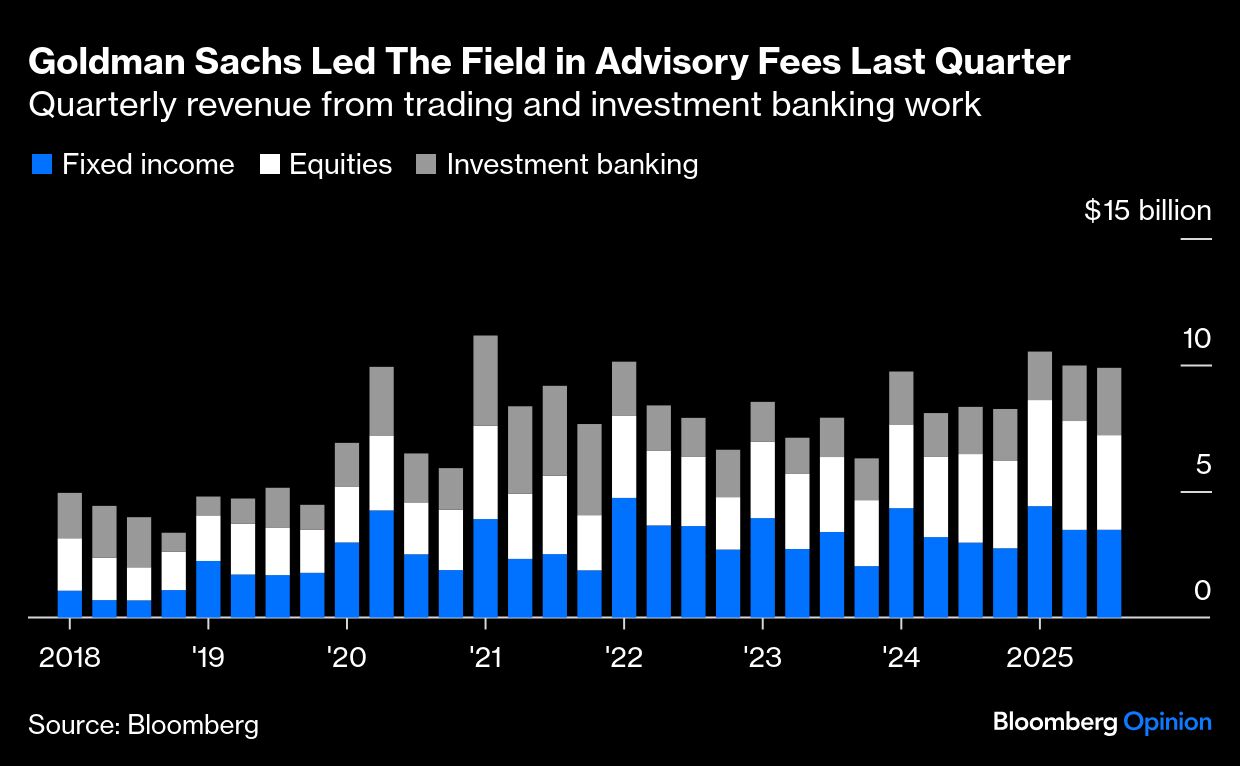

A recent data revision from the Fed showed that lending to non-banks accounted for all of the loan growth across US banks this year. These borrowers now make up 13% of loans outstanding. While most of the big banks don’t break out revenue from lending to hedge funds and other asset managers, Goldman’s results give some clues to the demand. Revenue at Goldman’s prime brokerage unit, which lends against equities, climbed by about one-third compared with the same period last year — a quarterly record for that unit.

Banks’ capacity for this kind of lending has been promised a further lift from the Fed’s plan to change how so-called supplementary leverage ratios are calculated. This will allow banks to further grow their prime broking and bond financing arms at home and overseas — and funnel more money into potentially frothy markets.

Beyond that, executives hope that the Fed and other regulators will soon make rule changes that could free up even more capital and either allow banks to add more risk or make huge payouts to shareholders, who will need to look for assets to plow this money into. Consultants at Alvarez & Marsal forecast this week that US deregulation could release nearly $140 billion in equity requirements from American banks — equivalent to almost half the capital backing JPMorgan today. This is a punchy, optimistic estimate to be sure, but it gives a sense of how far things could go.

At the same time, President Donald Trump’s efforts to influence the Fed have raised expectations that interest rates will be cut by a full percentage point by next summer. There are concerns that US economic growth will slow next year and that the labor market is starting to soften. But these cuts look more likely to feed higher asset prices than resolve the uncertainty about trade and tariffs that’s preventing business leaders from committing to fresh investments.

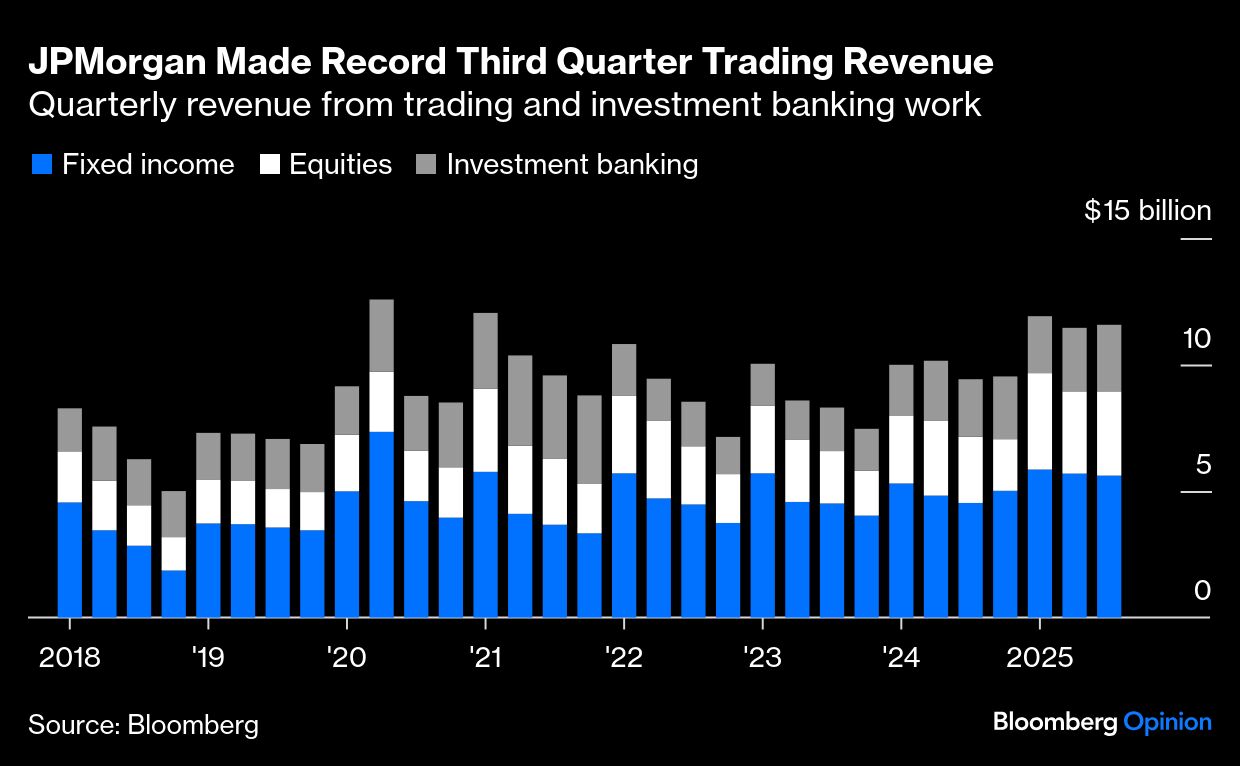

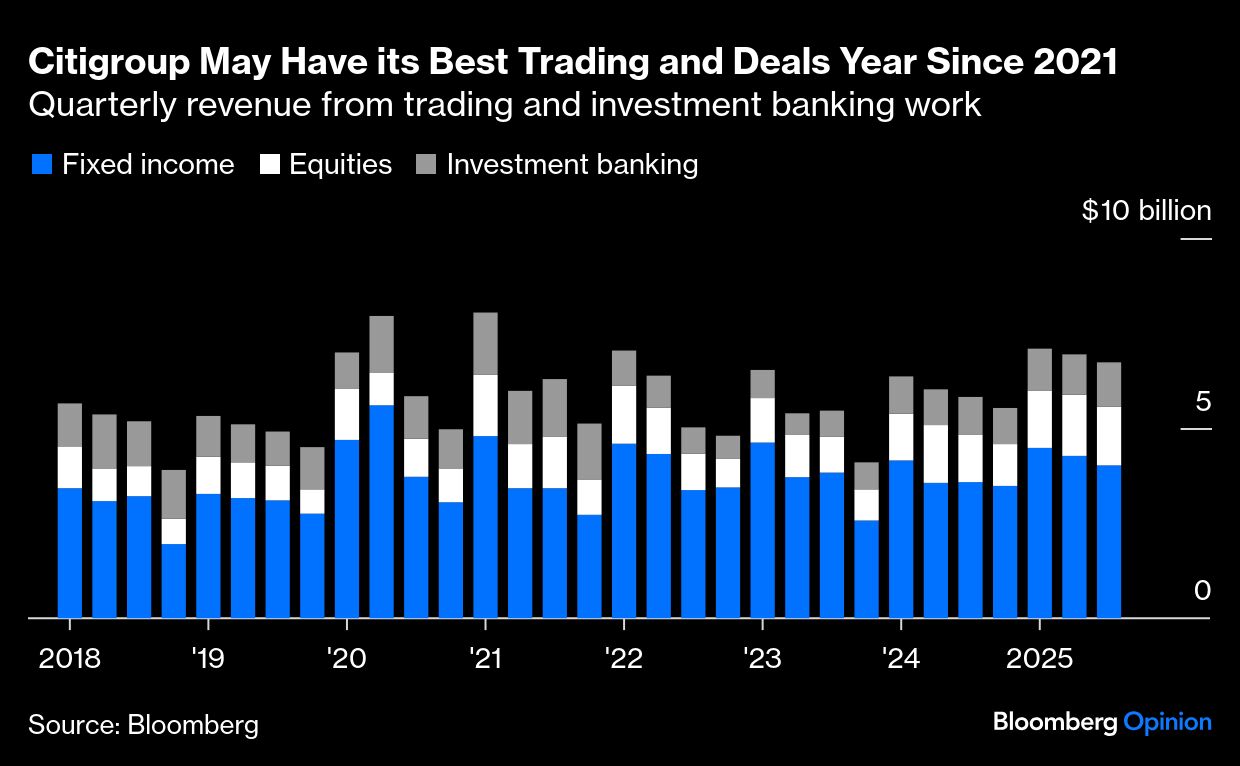

On Tuesday, JPMorgan reported its best ever third-quarter revenue for equities and fixed-income trading combined, while Goldman and Citigroup also reported their best third period for many, many years.